With geopolitics the second biggest driver – after inflation – of central bank reserves managers’ operations, financial markets may be underestimating the dark cloud looming. Rather than financial distrust, we may increasingly need to brace for political distrust. The threat of ‘beggar-thy-neighbour’ policies – from the US and China to anti-Russia sanctions and reserves confiscation – may be rising and, without renewed policy stimulus, stagflation will deepen.

Geopolitical factors were brewing before the invasion of Ukraine, evidenced by US tariffs under President Donald Trump, US/China frictions over trade and Taiwan, European populism and the UK’s exit from the European Union. Most acutely, the shocks to the energy market from the invasion will be pervasive, falling hardest initially on Europe, more directly dependent on Russian energy and heading into winter. But, given the linkages, high energy prices are elsewhere constraining growth, adding to consumer price index baskets and threatening a more inward-looking approach.

Should protectionism forces build, on top of any international ‘blame game’ following Covid-19, inflation in the first instance would intensify. But it would surely be more of the ‘wrong sort’ – cost-push led by tariffs, weaker currencies and goods shortages, rather than demand-pull. Central banks would have to turn a blind eye to aggressive tightening as economies stagflate. This portends more to the inflation rises of the early 1980s and 1990s recessions than the overheating of the late 1980s and mid-2000s. The inflationary flame from demand may snuff itself out without aggressive policy action.

Until the Russia/Ukraine war, the notion of slower international trade had appeared outside most official projections. And, even including it, world growth is generally expected to continue, albeit with the balance of risks ‘squarely to the downside’ (Figure 1)

While Joe Biden is a less confrontational US president, he has been loath to roll back his predecessor’s trade restrictions. For financial markets, trade frictions may (like Brexit in the UK) be a more long-term ‘crack-in-the-ice’ than an overnight ‘cliff-edge’ event. A disparity may occur, at least initially, between goods and service sectors, and broadening out to countries whose ‘cheaper’ imports can fill the gap. This potentially offers a reversal of the goods-over-services rotation under Covid-19.

Figure 1. Major economies are expected to carry on growing…

IMF’s real GDP growth projections (p): world, advanced and emerging market/developing economies (% yoy)

Source: IMF’s July 2022 updated world economic projections (post-2023 are indicative)

Source: IMF’s July 2022 updated world economic projections (post-2023 are indicative)

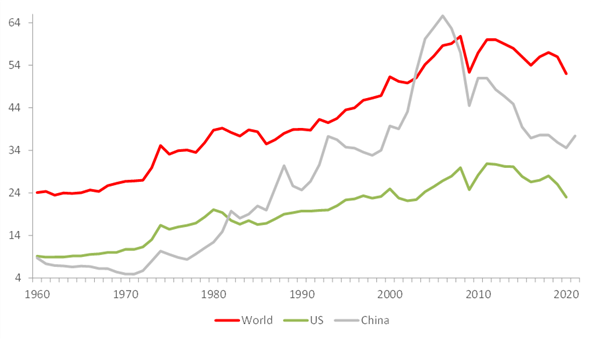

Figure 2. …On the assumption that world-trade growth is largely unabated

World, US and China’s trade (exports plus imports)* as a share of their respective GDP (all %)

Source: World Bank data (*goods and services)

Source: World Bank data (*goods and services)

The world’s appetite for international trade has, as a share of GDP, more than doubled in the past 50 years (Figure 2). Yet, without care, an unhelpful jigsaw piece from the 1930s – retaliatory protectionism – might come crashing into place. In 1930, it was triggered by the Smoot-Hawley Tariff Act that raised US tariffs to up to 20% on over 20,000 imported goods. This hit the US’ small number of trading partners (notably Canada and Europe) and prolonged the depression.

US Congress under Trump pushed back on a general approach. If needed though, the US president of the day has the facility to – without approval from Congress or the World Trade Organization – more fully invoke Section 301 of the 1974 Trade Act. This would impose tariffs on countries deemed by him or her to be engaging in ‘unfair’ trade practices against the US. It might be a last resort. But, for pre-emptive financial markets, the fear then would be of a scramble, triggered by a policy face-off between the US, China and an EU already taken up with fall-out from the war.

Trump’s tariffs in 2018 on steel and aluminium imports, and the administration’s investigations into alleged intellectual property rights violations in China and auto imports, (aimed at Europe and Mexico) looked potent first steps. They have not been repealed. If added to, they could spark retaliation unless there are more conclusive trade talks, which were never likely ahead of this autumn’s US midterms and China’s 20th National Congress. While not widely used since the WTO’s formation in 1995, US disaffection with the WTO and Biden’s need to gain favour after November could raise expectations of playing this card.

The impact this time of protectionism, whatever the source, would be more complicated than the 1930s.

First, economic and financial linkages suggest the knock-on would be more far reaching. Retaliation – whether tit-for-tat tariff rises, qualitative barriers and/or competitive currency depreciations – would activate second-round effects that would offset much of the growth impulse from 2020’s Covid-19 fiscal stimuli. In this case, the fiscal coffers would need to reopen if central banks are still normalising monetary conditions.

A strong dollar would reinforce this. In 1930, Canada ‘retaliated’ even before S-H became US law. The UK and France sought new partners, and Germany moved to autarky. Canada then forged closer links with the UK – an early precedent to the EU deal it signed in 2016.

The broader mix of countries affected would include the emerging markets whose ‘cheaper’ imports then fill the gap. Were the US the initial trigger, then Mexico (which relies on the US for 80% of its exports and the bulk of remittances) and Canada (despite new, post-North American Free Trade Agreement arrangements) would be especially heavy hit. China could react by devaluing its currency more aggressively, though this a double-edged sword given China’s external debt liabilities. This could spark competitive depreciations in Southeast Asia.

Second, despite the US being a relatively closed economy, the deflationary return could be much larger than anticipated. A renminbi devaluation that hurt China’s balance sheets would question its commitment to US Treasuries just as the US budget deficit widens. With US mortgage rates priced off long yields, this could come back to bite US households. And tariffs on importing countries would surely disrupt supply chains (already tested by transport strikes in the UK), and the ability and cost of home companies outsourcing their production. Setting up chains elsewhere may be more costly in a protectionist world.

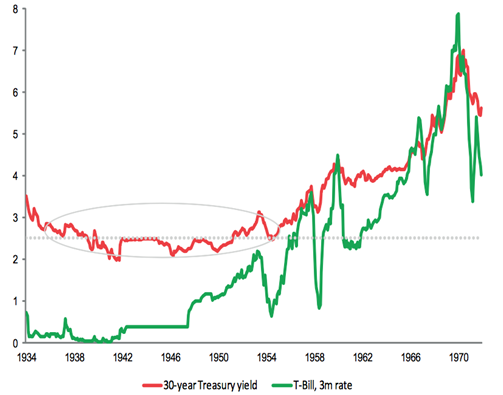

Figure 3. QE in the 1930s was – like now – not short-lived

US 30-year Treasury bond yield and US T-bill 3-month rate (both %)

Source: Refinitiv Datastream

Source: Refinitiv Datastream

Should it come to it, restricting immigrant workers would limit the labour pool, contribute to hiring difficulties and skill shortages and risk an element in short supply: potential growth. The National Bureau of Economic Research in 2018 estimated that the undocumented workers threatened by Trump contributed 3% of private sector GDP. Yet, by accounting for 9% of agriculture, construction and leisure sector value added, their relatively low-skilled, low-pay jobs did not offer widespread appeal.

Third, more direct vulnerability from protectionism probably lies not with the US (whose trade dependence is limited) and China (where dependence has been falling), but smaller, open economies. These include Southeast Asia (Malaysia and Thailand’s trade – exports plus imports – each exceeds 100% of GDP, Vietnam’s is 200%, Singapore’s over 300%); Australia and New Zealand (40% and 44%); United Arab Emirates (162%); and core Europe (Germany 89%, UK 55%, Netherlands 156%).

For other emerging markets, the outlook in a more protectionist, strong dollar scenario would be less rosy. Clear vulnerabilities exist, such as those non-commodity-exporting sovereigns with high exposure to short-term external debt and foreign saving needs, including Turkey, Argentina and Ukraine. For most others, external debt ratios are lower, with fewer currency pegs to have to protect. And if domestic debt-strains build, they too can run quantitative easing.

So, the question after 14 years of QE exceeding $25tn is how the big central banks normalise the monetary dials without unintended consequences. Their bloated balance sheets suggest they cannot take us off guard. If the 1930s is any guide, US QE ran unbroken from 1937 to effective Federal Reserve independence in 1951 (Figure 3). Today, by running passive quantitative tightening, the Fed is expected to normalise its balance sheet by 2025. But, if protectionism grows, this – and a return to historic policy norms globally – may be optimistic.

Neil Williams is Chief Economist, OMFIF.

This article will also be published in the forthcoming edition of the OMFIF Bulletin.