Decentralised finance is transforming the financial system by replacing traditional intermediaries with blockchain networks, smart contracts and permissionless protocols. Services such as lending, savings, payments and insurance are now available to anyone with a smartphone and internet connection.

By 2023, DeFi adoption surpassed 6.5m wallets worldwide, reflecting its borderless reach. For developing economies, this is particularly significant. The World Bank once estimated that 1.4bn adults remain unbanked, most in low-income regions. With remittance costs averaging 6.3% through traditional channels, compared to under 3% for blockchain transfers, DeFi promises cost efficiency and expanded access.

Yet the risks are profound. In 2022 alone, $3.8bn was lost in DeFi hacks and exploits. The pseudonymous nature of wallets opens loopholes for fraud, terrorist financing and money laundering, echoing the Financial Action Task Force’s warnings.

National security concerns

DeFi’s open architecture has direct implications for national and international security. First, illicit financial flows, where pseudonymous wallets enable discreet transfers, decentralisation may weaken traditional accountability, reconcentrating risks in less visible parts of the value chain.

Second, systemic vulnerabilities such as the 2022 Terra/Luna collapse, which erased $40bn in market value, revealed how fragile DeFi ecosystems can destabilise wider financial markets.

National security concerns also include regulatory gaps and sanctions evasion. Specifically, in 2022, the US Treasury reported that North Korea’s Lazarus Group laundered over $600m via DeFi to finance weapons programs. Similarly, the European Union flagged DeFi as a tool for sanctions evasion by Russian entities following the Ukraine invasion.

Using survey data and ARDL analysis in my research, fintech adoption appears to correlate with increased money laundering risk, though this risk is significantly moderated by strong regulation and financial literacy. This underscores the imperative: without adaptive oversight, DeFi can amplify vulnerabilities in fragile economies.

Financial inclusion

Despite security concerns, DeFi’s potential for financial inclusion is undeniable. In sub-Saharan Africa, the World Bank reported that 57% of adults remain unbanked. DeFi’s mobile-first approach offers savings, microloans and remittances without reliance on physical banking infrastructure.

Global remittance inflows reached $626bn in 2022. With traditional channels charging high fees, DeFi provides faster, cheaper alternatives. Decentralised credit and investment pools are already empowering small businesses in Kenya and Nigeria, where conventional credit scoring excludes many entrepreneurs.

But access alone is insufficient. Digital financial literacy is critical. Weak literacy undermines AML efforts and allows criminals to exploit new systems. True inclusion requires not only access but also digital intelligence, awareness and protections for users.

Adaptive policy and regulation

The convergence of DeFi, central bank digital currencies and financial crime demands adaptive, risk-based regulation. A one-size-fits-all approach risks stifling innovation or enabling abuse. Instead, policy-makers should adopt risk-based oversight and distinguish between high-risk tools and lower-risk payment solutions. Regulatory and supervisory tech should also be leveraged alongside the deployment of artificial intelligence, blockchain analytics and machine learning for real-time monitoring.

Policy should also focus on strengthening cross-border co-operation and prioritising consumer protection and literary. Harmonised rules are vital to prevent regulatory arbitrage and liability frameworks, compensation mechanisms and education campaigns should accompany technical safeguards. Policy-makers should also encourage innovation sandboxes. Controlled environments, like those pioneered by the UK’s Financial Conduct Authority and Monetary Authority of Singapore, allow safe experimentation.

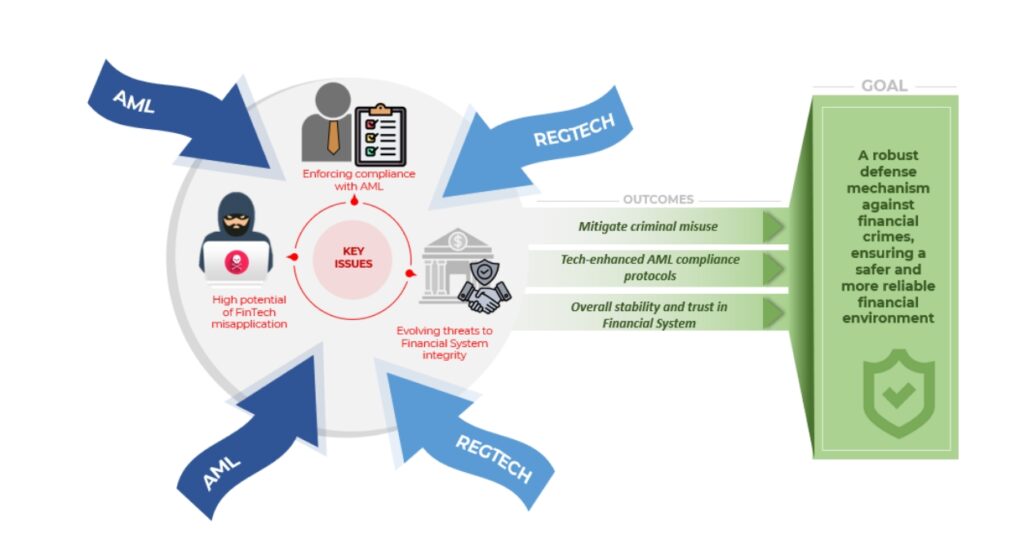

This approach of ‘embedded regulation’ where compliance tools are built directly into DeFi systems, ensuring resilience without compromising decentralisation. Figure 1 illustrates this policy imperative, demonstrating how AML frameworks and regtech solutions can co-operate to strengthen financial system integrity. By addressing risks such as fintech misapplication and evolving threats to compliance, regulators can create a robust defense mechanism against financial crimes mitigating misuse, enhancing AML protocols and ultimately fostering trust and stability in the financial system.

Figure 1. Enhancing resilience through AML and regtech solutions

Addressing key risks

Source: ‘Fintech and money laundering in Nigeria’

DeFi is not just a technological trend. It lies at the intersection of innovation, inclusion and security. For emerging economies, the stakes are especially high: poorly regulated DeFi accelerates illicit flows and systemic risks, while well-regulated DeFi expands access and strengthens resilience.

The tools for regulatory quality, digital literacy, regtech frameworks exist but their coordinated deployment is lacking. Adaptive, evidence-based and internationally harmonised policies are the only way forward if we want DeFi to contribute positively to global stability. The challenge is not whether to regulate, but how to regulate in a way that secures both financial integrity and inclusive innovation.

Nafisa Usman is Manager of Payments System Policy at Central Bank of Nigeria.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.