France is on its fourth prime minister since a snap election in June 2024 resulted in a hung parliament. The economic uncertainty that accompanies parliamentary gridlock manifests in the form of higher yields, indicating that political instability has costs.

Additional interest borne by the French taxpayer over the lifecycle of issued debt attributable to the political turmoil beginning in June 2024 is estimated to be €6-7.5bn. This instability penalty is thus far roughly equivalent to France’s annual expenditure on its Personalised Housing Assistance (APL) programme for low- and middle-income households – a cornerstone of the French welfare state. Each day of continued turmoil compounds the cost.

While the second premiership of Sébastien Lecornu has stabilised markets, the yield on 10-year French government debt, a benchmark indicator of the market’s perception of fiscal risk, remains far above its long-term average. Extreme short-term political risk may have abated, but long-term fiscal concerns persist. The one-notch downgrade by S&P’s on 17 October will reinforce, rather than settle, market unease.

The market’s perspective

From the perspective of a bond investor, France is becoming an increasingly problematic credit risk. At the end of Q1 2025, France’s debt-to-gross domestic product ratio stood at 114.1%, the third highest in the euro area, beaten only by Greece (152.5%) and Italy (137.9%). In European debt markets, the key indicator of fiscal risk is the spread between the yield on a country’s 10-year bonds and the yield on the equivalent German Bund. Bunds are the safe reference asset of the euro area – the yardstick against which all other assets may be compared. An increase in the spread between the yield on French 10-year bonds (OATs) and German 10-year Bunds, all else equal, implies deteriorating conditions in the French economy. In France, this spread is driven by political risk.

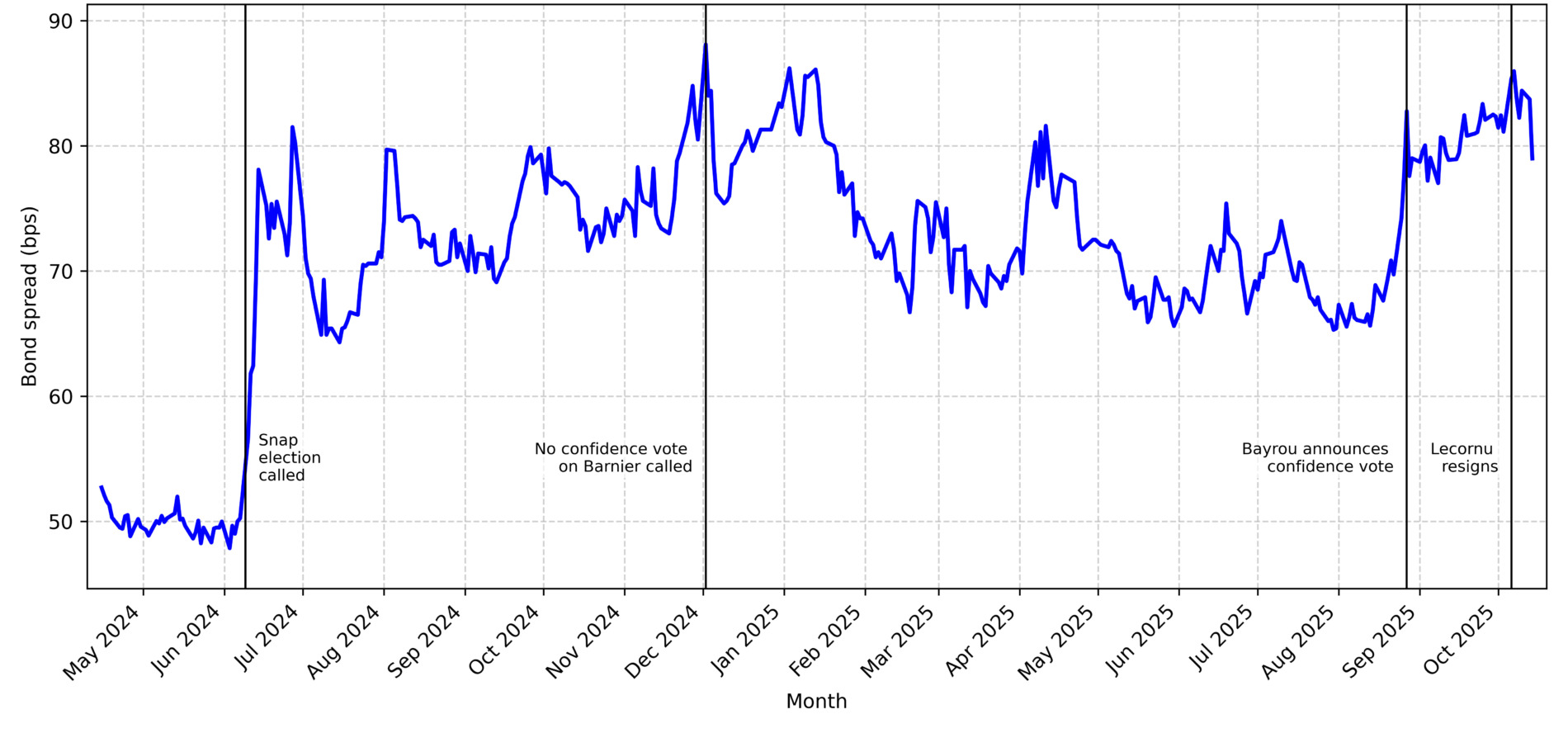

Figure 1. French 10-year OAT-Bund spread widens post-election

10-year OAT-Bund spread

Source: London Stock Exchange Group Eikon and OMFIF analysis

Between the beginning of the European Central Bank’s post-pandemic rate hiking cycle on 27 July 2022, and the date of France’s snap parliamentary election on 9 June 2024, the average spread between 10-year OATs and Bunds was 53 basis points – in line with the post-euro area crisis average. Between the election and 16 October 2025, this spread averaged 74 basis points. The 21-basis point difference is the extra yield demanded by bond investors as compensation for political instability.

The sensitivity of the OAT-Bund spread to French domestic politics is heightened by the make-up of the French sovereign bond market investor base (Figure 1). Research from UniCredit indicates that 55% of investors in French bonds are foreign banks, foreign non-bank financial institutions and foreign central banks – a much higher share than that of Italy or Spain, which have historically been prone to similar bouts of fiscal incontinence.

Approximately 25% of French bonds are held by foreign NBFIs – the investor subsection most sensitive to negative news and rising uncertainty. This investor base increases the elasticity of the French 10-year yield with respect to French political dysfunction, with foreign NBFIs driving the transmission mechanism through which domestic political gridlock translates into higher borrowing costs for the French state.

The long-term view

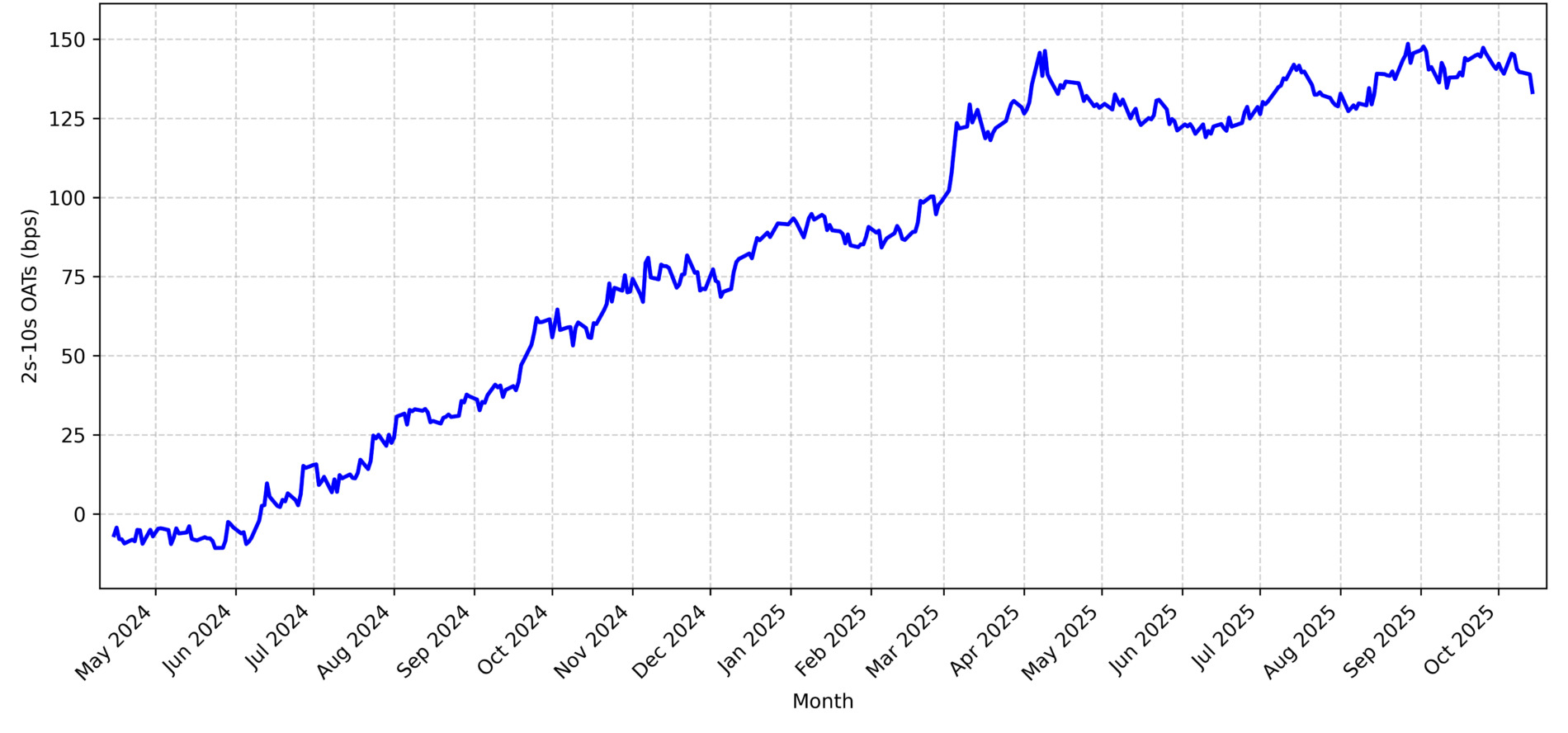

While changes in the 10-year OAT-Bund spread reflect shifts in the market’s perception of French relative to German fiscal risks, movements in the French yield curve itself provide an insight into investors’ perspectives on the balance of short- and long-term risks. A key barometer of economic and fiscal expectations in the short-term relative to the long-term is the 2s-10s curve. Steepening can reflect expectations of stronger growth, interest rate increases and higher inflation. It can also reflect a rising long-term risk premium.

Since the June 2024 snap election, long-term yields have risen much faster than shorter ones. Although this coincides with the beginning of the ECB’s easing cycle, which drags down shorter-term yields, the persistence of the increase in long-term yields implies the dominance of structural factors, in particular political and fiscal uncertainty, relative to cyclical ones, such as changing policy rates (Figure 2). Sharp steepening reflects the premium that investors now demand as compensation for a compounding budget deficit, reform paralysis and an increase in expected sovereign issuance.

Figure 2. Long-term risks dominate market outlook

A steepening 2s-10s curve

Source: LSEG Eikon

Mounting costs

While the increase in yields is most acute at the 10-year tenor, it is measurable across the curve. When the French government goes to market, the French taxpayer pays an average additional 14-17 basis points in interest annually over the life of the bond, attributable to political gridlock. Since the June 2024 snap election, the French government has issued €457bn in debt at a tenor longer than one year. The additional €6-7.5bn that will be shouldered by the French taxpayer over the coming decades is the cost of instability.

While the market will always reprice first, the three major ratings agencies, Fitch, Moody’s and S&P’s, have all downgraded French sovereign debt in the past 12 months. S&P is the most recent agency to update their assessment of French creditworthiness, with their downgrade seen as a response to Lecornu’s capitulation to the French Socialists over pension reform. Democratic compromise may be the hallmark of western governance, but compromise which risks the sustainability of the fiscal outlook comes with serious costs. With every new issue of government debt, the cost of instability grows.

ECB to the rescue?

In the euro area, governments have the implicit backstop of the ECB. A key argument against the existence of the euro area is the moral hazard that this creates for fiscal policy-makers. A key argument in its favour is the downward pressure this places on yields in the context of fiscal crises. The backing of the ECB allows investors to have confidence that sovereign default is a near impossibility.

If OAT spreads became so dislocated from fundamentals that they impacted the transmission of monetary policy, then the ECB can intervene with their Transmission Protection Instrument. The purpose of the TPI is to counter disorder in the bond market that disrupts the ECB’s capacity to manage interest rates. While according to the letter of the rulebook, the ECB is prohibited from using TPI in the French bond market, since France is currently subject to the Excessive Deficit Procedure due to its unsustainable fiscal position, in practice, the ECB has substantial discretion. This backstop forms a key component of the case for market stability despite mounting fiscal risks. With true fiscal reform increasingly unlikely, a bet on long-term French government debt has become a bet on the TPI containing any amplification of disorder in the French sovereign bond market.

When a member state’s best hope of fiscal relief is ECB intervention, they have made a wrong turn. While the postponement of pension reform is an acceptable compromise to avoid indefinite gridlock, France cannot continue to shun meaningful fiscal adjustment. A prayer for the deus ex machina of ECB intervention is not a fiscal framework. There is no substitute for true spending reform.

Conor Perry is an Economist at OMFIF.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.