France’s inability to get its public finances in order has already drawn increasing concern. As one of the pillars of the European Union and the euro area, France faces a crisis that would make Greece’s troubles seem like a minor stumble.

Solutions will clearly need to address both expenditure and revenue in the short term. However, few realise that debt has a long-term dimension, and in the context of a demographic crisis, it can only be tackled by accelerating the growth of labour productivity – a solution that effectively rules out tax increases. This problem, however, is far from unique to France.

Labour output

Economists typically identify two primary factors of production: labour and capital. Labour typically accounts for between just over half to two-thirds of an economy’s output. Consider a typical advanced economy with debt levels around 100% of its gross domestic product. For such a heavily indebted country to grow at a reasonably robust pace – sufficient to finance its debt while allowing some wealth accumulation for its population – it should aim for at least 2.5% annual growth. This requires labour output, as a production factor, to increase by roughly 1.5% per year.

Achieving this is not overly difficult in an economy with a growing population, but that is not the situation in European countries. On the contrary, we are witnessing declining birth rates and associated trends of population decline. Moreover, as populations age – an inevitable consequence of these trends – the proportion of economically active individuals is also expected to decrease. For a country to grow sustainably and maintain manageable debt levels under such conditions, labour productivity growth must exceed the 1.5% threshold to compensate for this decline.

While demographic projections from different institutions may slightly vary, these differences are not considerable (Figure 1). Demographic trends are largely predetermined, with a degree of uncertainty dramatically lower than that of economic forecasts for similar periods.

Figure 1. Demographic outlook for major economies

| Country | Population 2024 (m) | Population 2050 (m) | Active share 2024 (%) | Active share 2050 (%) | Average growth of economically active 2024-50 (%) |

| Argentina | 46.7 | 53.2 | 60 | 55 | 0.2 |

| China | 1411.8 | 1312.5 | 67 | 60 | -0.7 |

| India | 1449.9 | 1670.0 | 55 | 58 | 0.8 |

| Japan | 123.2 | 104.8 | 60 | 50 | -1.3 |

| France | 64.9 | 63.5 | 51 | 45 | -0.6 |

| Germany | 84.4 | 80.9 | 58 | 50 | -0.7 |

| Italy | 59.0 | 54.4 | 50 | 45 | -0.6 |

| EU | 453.3 | 447.2 | 49 | 45 | -0.4 |

| UK | 68.6 | 73.5 | 58 | 52 | -0.2 |

| USA | 341.8 | 380.0 | 62 | 58 | 0.2 |

| Czechia | 10.8 | 10.3 | 78 | 76 | -0.2 |

| Poland | 37.6 | 31.9 | 73 | 71 | -0.7 |

| Romania | 19.0 | 15.8 | 68 | 67 | -0.7 |

Source: Organisation of Economic Co-operation and Development, Eurostat, International Monetary Fund, World Bank, author’s calculations

Note: Countries where the number of economically active individuals is expected to grow, such as Argentina, India or the US, their bar is set lower.

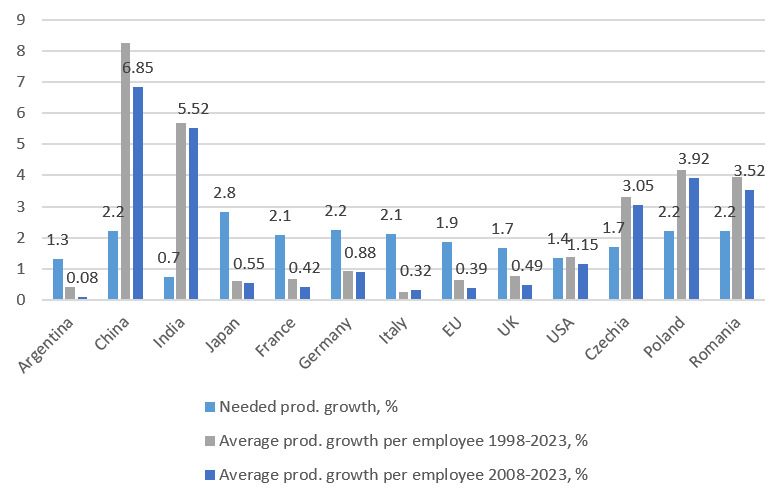

To gauge whether economies are equipped to meet this challenge, it may be more instructive to examine historical labour productivity growth over a longer period. Figure 2 compares the required productivity growth (1.5% plus the average expected decline in the economically active population by 2050) with historical labour productivity growth per employee from 1998-2023 in the discussed economies.

Figure 2. Past versus needed productivity growth

Source: World Bank, author’s calculations

Simply put, from this relatively straightforward perspective on growth, it does not appear that India, China or the newer EU member states face considerable challenges in achieving productivity growth sufficient to offset population declines. One could imagine that the new EU might mismanage its policies or be forced to undermine productivity growth, but the experience of the past 25 years does not suggest this. Similarly, one could speculate that China might fail to sustain its observed productivity growth rates over the next quarter-century, but its margin for error is clearly substantial.

The picture is far wore worrying for France, Germany, Italy and the EU overall. For these economies, the gap between the productivity growth required to stabilise debt and what has theoretically been achieved exceeds one percentage point. A similar, quantitatively even more alarming conclusion holds for Japan, and to a lesser extent, the UK.

A similarly alarming result applies to Argentina, whose current economic situation illustrates the kind of institutional and structural reform likely needed across the euro area if it is to remain financially sustainable in the long term. One might also hope that advancements in artificial intelligence could enable such progress with less drastic changes. However, it must be admitted that the EU is currently creating more regulatory obstacles to such developments than fostering them.

Finally, it is crucial to note that addressing debt sustainability amid a declining economically active population cannot be achieved by introducing new, creative taxes or through fiscal loosening. Such taxes effectively drive out the individuals and firms that push productivity forward. While they might generate some additional budgetary revenue, this comes at the cost of productivity stagnation – a situation that the already heavily taxed economies discussed here are closest to among all those mentioned. Similarly, Keynesian stimulus in an economy constrained by a labour shortage is unlikely to produce anything beyond higher inflation and a worsened trade balance.

It remains unclear how the euro area and the EU will address the issue of sustainable financing given current demographic trends. It is also uncertain whether their leaders even fully grasp the scale of the problem they are facing. In the particular case of Italy’s representative and the author of the EU competitiveness report, Mario Draghi, the answer to these questions is affirmative.

Given that he began his career managing Italy’s debt at the ministry of finance, his frequent emphasis on productivity in the report bearing his name, as well as his assertive push to channel more resources from the new EU and other economies with less dire long-term financial prospects into the EU budget, support this view. What is certain is that the communication from EU leaders and those of advanced economies grappling with this issue does not remotely suggest a commitment to the reforms needed to tackle it.

Miroslav Singer is Director of Institutional Affairs and Chief Economist at Generali Group and a former Governor of the Czech National Bank.

Over the past three years, OMFIF has collaborated with EY on a project that explores how to improve public finance management. This year’s project examines how governments can more effectively allocate public funds to support better fiscal, economic and societal outcomes. A series of roundtable discussions will result in a research report, publishing 2 December.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.