Reducing public debt in Europe is feasible based on past fiscal adjustments. But some governments are struggling to agree and implement consistent medium-term fiscal plans. In these circumstances, debt sustainability hinges on boosting growth where the outlook is only partially encouraging. Growth will be a moderate 1.0% in 2024 and 1.8% in 2025.

The European Union responded well to the pandemic and energy crises. The economy recovered swiftly but raising the region’s long-term growth potential remains critical.

Accelerating the implementation of Next Generation EU reforms and investments is imperative, as is advancing the capital markets union, initiated in 2015, to facilitate cross-border savings and investments and optimise resource allocation. The digital transition, including artificial intelligence development, could bolster productivity provided the EU can match its pace in developing regulatory frameworks that allow innovation.

Figure 1. Euro area fiscal disparities widen after successive crises

Germany debt differential versus France, Italy and Spain, percentage points of GDP

Source: IMF, Scope Ratings forecasts.

Europe might also encourage more immigration to address labour shortages, though current political dynamics make it unlikely. Likewise, reforming Germany’s debt-brake rule to allow for an investment-driven fiscal stimulus also appears improbable before the 2025 federal elections.

Amid sluggish growth, Europe faces structurally higher public debt after the Covid-19 and energy crises and wider fiscal disparities across euro area sovereigns. The debt-ratio differential between Germany and France has widened from 38 percentage points in 2019 to nearly 50pps, contrasting sharply with the near zero differential between 1992, when the Maastricht Treaty was signed, and 2012, the height of the euro area crisis (Figure 1).

Capacity of euro area sovereigns to respond to shocks is diverging

This matters because different public debt levels imply varying capacities to respond to the next shock. Divergent fiscal positions may also complicate future discussions about solidarity and fiscal risk sharing, especially in the case of country-specific rather than regional shocks.

Finally, interest costs are set to remain higher than before the pandemic even as central banks ease rates later this year. Public debt issued before and during the pandemic will be refinanced at higher rates. Italy, Germany, France and Spain collectively will pay almost €170bn more in interest in 2028 than in 2020.

These three challenges – moderate growth, high public debt and rising interest payments – coincide with pressures for higher spending and investment, exacerbated by demographic shifts and declining working populations. These trends will strain budgets by around 1.5pps of gross domestic product, on average, in the coming years. Similarly, the investment to achieve carbon neutrality by 2050 is equivalent to about 0.5% to 1.0% of GDP a year for the public sector alone, based on European Commission data.

Europe will also have to invest more to meet Nato defence targets, in some cases of around 0.5% to 1.0% of GDP, in addition to funding support for Ukraine. Industrial policies to bolster domestic production for economic autonomy and national security will also squeeze budgets, through lower taxes and more generous subsidies. All told, Europe’s identified policy priorities imply higher spending and investment of about 3% to 5% of GDP.

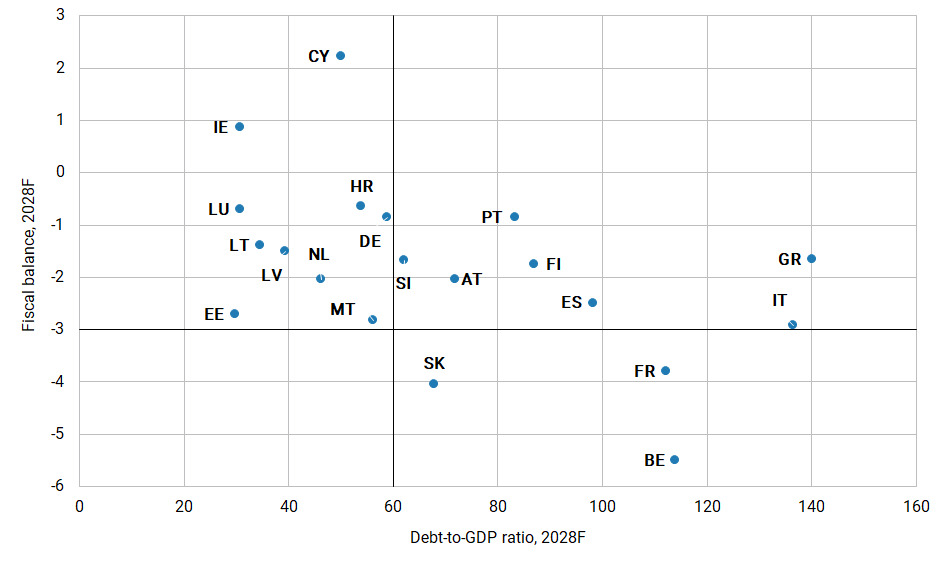

Important fiscal adjustments are required

How governments prioritise spending will depend on their specific circumstances and the degree of European solidarity.

For example, the Baltic states, central and eastern European countries and Finland are unlikely to scale back on defence given their proximity to Russia whereas, for countries in southern Europe, defence is likely to take a back seat. High-tax countries like France and Belgium as well as Germany and Austria may consider rebalancing tax structures away from labour, which is becoming scarcer, towards capital, ownership and environmental factors.

Fiscal pressures may also accelerate discussions about which expenditure is best suited at the European rather than national level, particularly after healthcare, energy and defence emerged in recent years as important European as much as national public goods.

Reform-minded governments will make necessary trade-offs. The additional adjustment needed to ensure a steady decline of public debt, even among the most indebted European sovereigns, is around 1.5% to 2.0% of GDP, based on data from Bruegel. This is feasible based on historical fiscal adjustments, although past consolidation usually benefitted from higher nominal growth.

However, for several European sovereigns, complacency is the risk. Weak governments may postpone and delay important reforms, damaging investor confidence, which at some point may lead to forced ad hoc austerity curbing public investments and growth. The UK’s recent experience shows that even G7 countries are not exempt from these potential dynamics.

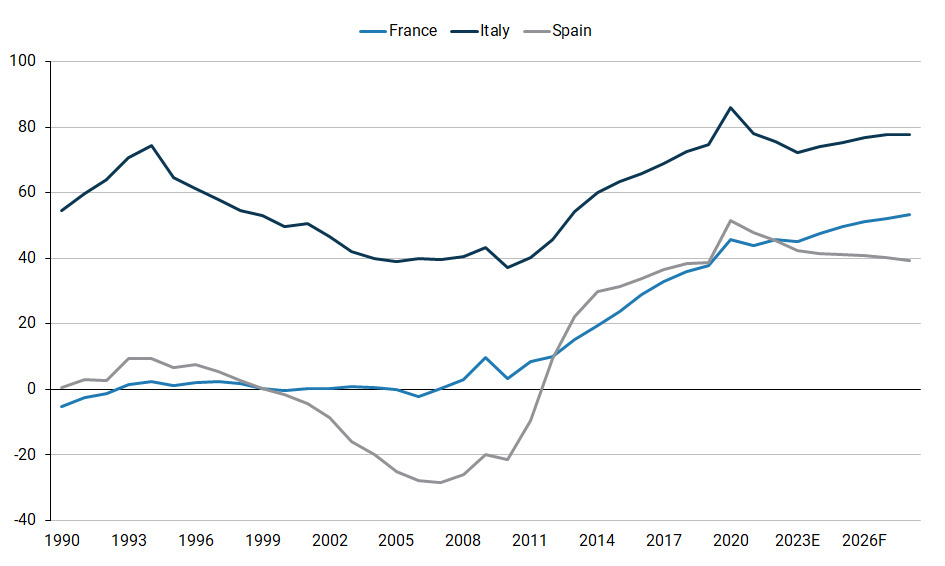

Previously crisis-hit countries such as Greece, Ireland, Portugal, Spain and Cyprus have implemented important reforms under EU financial assistance programmes, resulting in more favourable macro-economic trajectories (Figure 2).

Figure 2. Diverging public debt trajectories for select euro area sovereigns

% of GDP

Source: Scope Ratings forecasts

In contrast, France and Belgium, which we rate with a negative outlook, risk failing to fully acknowledge their financial constraints. Government plans that aim only to stabilise public debt at current elevated ratios imply that debt will rise come the next crisis.

France’s recent upward revision of its fiscal deficit to 5.5% of GDP for 2023 further challenges the government’s consolidation plan, which may now require additional savings of around €50bn, or 2% of GDP, in the years ahead of the 2027 elections.

Similarly, in the absence of policy changes in Belgium following the federal and regional elections in June, Belgium will record the largest fiscal deficit in Europe, exceeding 5% of GDP over the coming years. This would result in a steadily increasing debt trajectory and the third-highest level of public debt in Europe by 2028, after Greece and Italy.

Alvise Lennkh-Yunus is Head of Sovereign and Public Sector Ratings, Scope Ratings.