Q1 2024

Mexico: no longer a tale of two elections

Politics no longer drives Mexican financial markets, but reforms are required to become a nearshoring nirvana, writes Nikhil Sanghani, managing director, Economic and Monetary Policy Institute, OMFIF.

The prospect of a left-leaning Mexican government and a Donald Trump presidency in the US frightened investors in Mexico almost a decade ago, but not now. The political situation is more stable and there is optimism over the potential economic gains from ‘nearshoring’. The next Mexican president will need to push through structural reforms for the country to take full advantage of this opportunity.

This year, general elections will be held in Mexico on 2 June. The latest polls put the governing Morena party well ahead of its rivals. So it seems likely that incumbent President Andrés Manuel Lopez Obrador – who is unable to run again – will be succeeded by Morena’s chosen presidential candidate Claudia Sheinbaum. The elections north of Mexico’s border will be a much closer call, but it is a distinct possibility that Trump will return to the White House.

These outcomes – a Morena government alongside a Trump presidency – were big concerns for investors in Mexico from 2016-18. Trump had threatened to rip up the existing North America Free Trade Agreement between the US, Mexico and Canada during his 2016 election campaign. Two years later, there were fears over excessive state intervention following the victory of AMLO in Mexico and subsequent cancelation of the $13bn Texcoco airport project (which was already partly built).

From 2016-18, the Mexican peso sank by 12% against the dollar, in part due to these political factors (Figure 1). This fall would have been more severe had it not been for the decisive actions of Mexico’s central bank, which raised its policy rate by 500 basis points over this period.

Figure 1. Mexican peso hit by political factors

Mexican peso per US dollar, inverted (2016-18)

Source: London Stock Exchange Group, OMFIF analysis

Investors’ fears were eventually quelled. NAFTA wasn’t scrapped but amended to become the United States–Mexico–Canada Agreement (T-MEC in Spanish). Meanwhile, on the domestic front, AMLO eased his interventionist rhetoric. He has generally kept a lid on public spending, which has helped to maintain Mexico’s sovereign investment-grade rating. However, the 2024 budget includes fiscal impulse worth 2.4% of gross domestic product, which will need to be reined in by the next administration to keep the public debt on a sustainable path.

Accordingly, political factors are not as concerning for investors now as they were eight years ago. If anything, (geo)politics is a tailwind to Mexico’s current economic prospects. Amid US-China tensions – which will probably persist regardless of who wins the US elections – there is optimism that Mexico will benefit from the relocation, or ‘nearshoring’, of supply chains. There are signs this is starting to materialise as Mexico has overtaken China as the US’s largest trading partner.

However, the next government’s policies will have a major bearing on whether Mexico’s economy will reap the full rewards from nearshoring.

The arguments made now could have applied to Mexico when NAFTA came into force in 1994. Companies are seeking to establish a low-cost manufacturing hub with close ties to the US, Mexico will benefit from higher foreign direct investment, export growth and productivity gains.

But, by and large, this failed to play out. While Mexico has built a strong manufacturing base in the north, the rest of the country has seen little economic gains. Instead of achieving catch-up growth, Mexico’s GDP per capita has fallen further behind the US since it joined NAFTA, based on market exchange rates and in purchasing power parity terms.

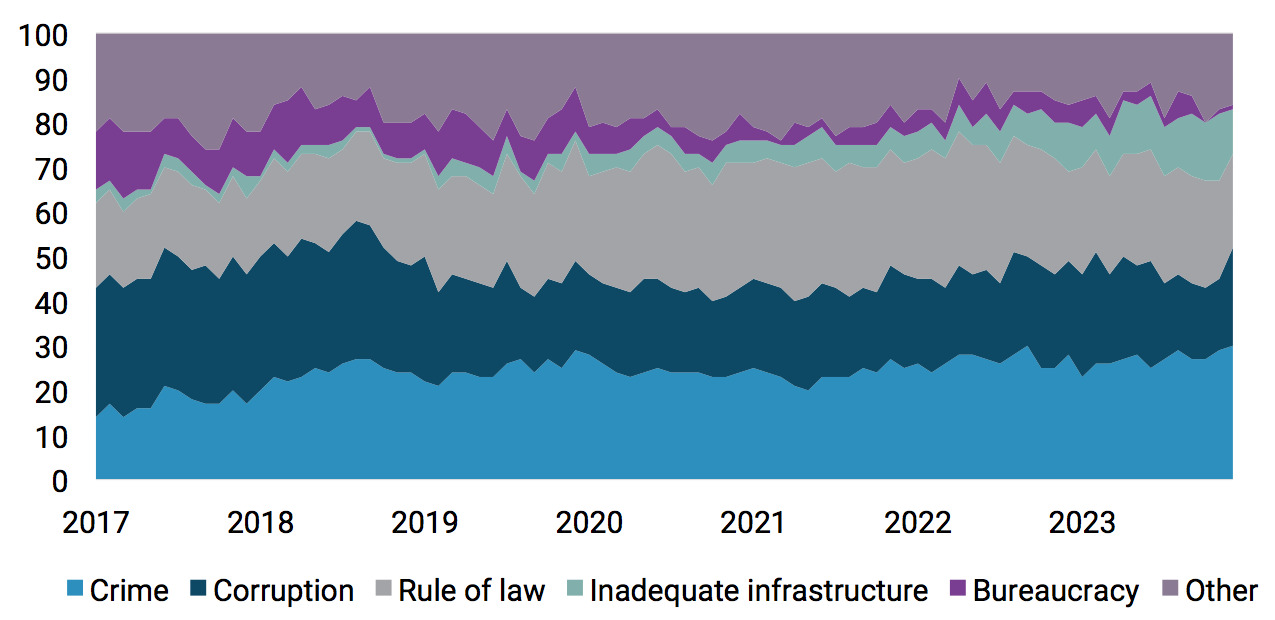

Key reasons for this underperformance include the poor business environment marred by crime, corruption and weak rule of law. The vast majority of private sector economists surveyed by Banco de México selected these three factors as the main obstacles to business in Mexico over the past five years (Figure 2).

Figure 2. Crime and corruption seen as persistent issues in Mexico

Obstacles to doing business in Mexico, share of responses, %

Source: Banco de México, OMFIF analysis

There is also a lack of competition in domestic industries, especially the energy sector. The current government has continued to prop up the ailing state-owned oil company Pemex and deter private sector involvement. That has contributed to a misallocation of government resources and an inefficient energy sector. The International Monetary Fund’s Article IV report for Mexico warns that ‘subsidising investments by Pemex risks creating costly stranded assets’.

Mexico has an opportunity to benefit from nearshoring but success is not guaranteed. It will require structural reforms to tackle corruption and crime while encouraging more competition in the domestic economy, particularly in the energy sector. It remains to be seen if Mexico’s next government will be willing or able to alter the picture.