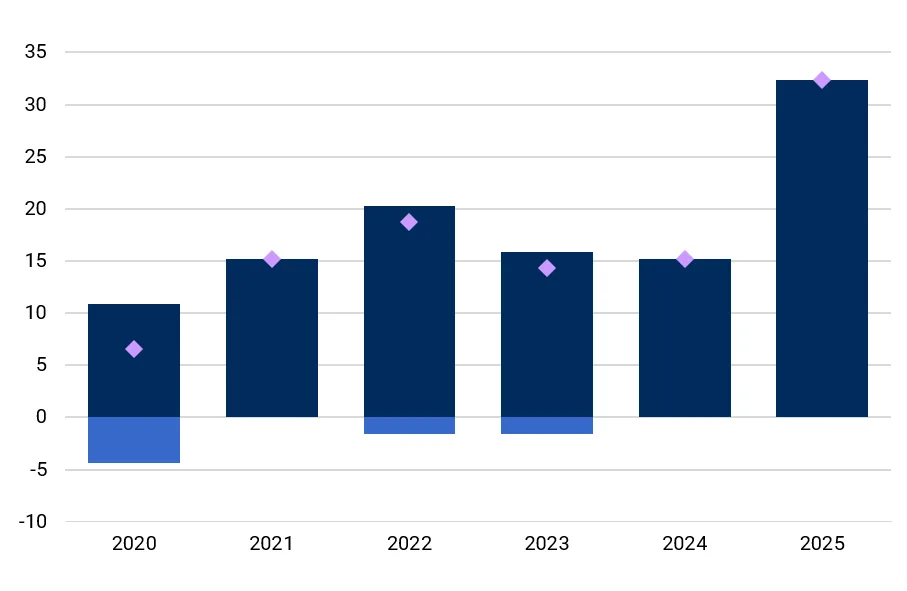

Last year, public investors were reassessing the role of gold not simply as a symbolic reserve asset, but as a more active portfolio hedge in an increasingly fragmented geopolitical environment. That shift was reflected in OMFIF’s Global Public Investor 2025, which showed central banks are continuing to increase gold allocations amid concerns over sanctions risk, reserve diversification and long-term strategic resilience (Figure 1).

Figure 1. Central banks are going for gold

Over the next 12-24 months, do you expect to increase, decrease or maintain your allocations to gold? Share of respondents, %

Source: OMFIF Global Public Investor 2025

In May, OMFIF hosted its annual seminar in London, in partnership with State Street Investment Management. This year’s discussions, shaped by escalating tensions in the Middle East, concerns around US fiscal policy and renewed questions over traditional safe havens, suggested that the conversation has broadened beyond gold itself.

The discussions at the OMFIF-SSIM seminar revealed a growing recognition that diversification is entering a new phase. The traditional framework, built around balancing equities and bonds across regions and sectors, is proving less reliable in a world shaped by persistent inflation uncertainty, geopolitical fragmentation and repeated market shocks. Public investors are increasingly being forced to think not only about what they own, but what specific risks they are trying to hedge.

While gold remained part of the conversation, particularly given continued central bank demand and concerns around reserve diversification, the emphasis shifted towards broader questions around liquidity, implementation and governance under stress.

Liquidity becomes part of diversification

One recurring theme throughout the discussions was that liquidity itself has become a more important component of diversification. This reflects not only the lessons from recent market shocks, but also the reality that investors may need to rebalance portfolios quickly during periods of stress. In practice, the ability to act during volatility can matter as much as the underlying allocation itself. ‘We’ve become a bit lazy sometimes as portfolio constructors and asset allocators. We’ve relied on old maxims, like bonds and equities always diversify each other’, said one participant during the discussion.

The Middle East war emphasised this point and, unlike previous geopolitical episodes where gold served as the dominant hedge, recent market behaviour has demonstrated that energy and commodity exposures can become equally important during supply-driven inflation shocks. Public investors are therefore increasingly questioning not only which assets belong in a portfolio, but also which risks portfolios are designed to hedge against. As one participant said, ‘We really need to think about what diversification means, and especially what risks we are trying to diversify against’.

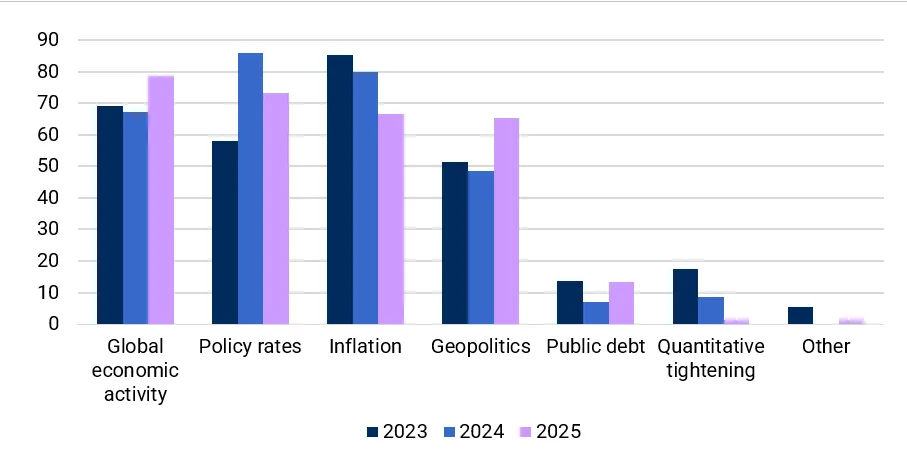

This evolving mindset aligns closely with findings from OMFIF’s GPI 2025 (Figure 1.2). The survey of central banks highlighted how public investors were reassessing portfolio construction frameworks in response to geopolitical fragmentation and higher-for-longer inflation risks. Gold purchases continued to rise, reserve managers remained focused on diversification away from concentrated currency exposures and institutional investors showed growing interest in alternative sources of protection.

Figure 2. Growing focus on geopolitics

What are the most important economic challenges affecting your investment approach over the next 12-24 months?

Source: OMFIF GPI 2025

Yet the discussions at this year’s OMFIF-SSIM seminar also suggested that diversification is becoming more operationally demanding. It is no longer sufficient to hold a wider mix of asset classes if institutions lack the governance structures, liquidity management frameworks or implementation flexibility required to navigate periods of market stress.

Several participants reflected on how recent crises exposed these constraints. During episodes such as the UK liability-driven investment crisis, Covid-19 market dislocations and more recent geopolitical shocks, the challenge was often not identifying the correct investment response but being able to act quickly enough within existing governance structures. In this sense, diversification increasingly depends as much on institutional agility as on strategic asset allocation.

Liquidity management emerged as another critical issue. Long-term asset owners continue to increase allocations to private markets in pursuit of diversification and illiquidity premia, while simultaneously facing growing demands for flexibility and liquidity. This tension is particularly acute for pension funds and other institutions facing daily liquidity requirements while maintaining substantial exposures to infrastructure, private equity and real estate. ‘People have realised that liquidity is the thing that makes funds fail’, said one participant.

Rethinking safety and reserve management

For reserve managers, the constraints are different but equally significant. Safety, liquidity and capital preservation remain central considerations. Several discussions highlighted the challenge of balancing reserve adequacy, diversification and market functionality at a time when reserve portfolios have become exceptionally large relative to domestic economies. Questions around concentration risk, the future composition of safe assets and the long-term role of reserve currencies continue to move higher up the agenda.

Public investors are also becoming increasingly aware that fiscal dynamics and geopolitical fragmentation are more directly influencing market outcomes. The result is a world in which macroeconomics and political volatility can no longer be analysed separately. At the same time, public investors are not retreating from risk entirely. Rather, the discussions reflected a more nuanced approach to diversification, one that prioritises flexibility while still positioning portfolios to benefit from long-term structural themes, including artificial intelligence, digital infrastructure and energy transition investment.

Against this backdrop, diversification is becoming more dynamic, more operational and arguably more difficult. The forthcoming GPI 2026, launching on 30 June, examines whether this shift is now translating into a more structural reassessment of how public investors define safety, liquidity and capital preservation. For many reserve managers, there are growing signs that diversification is no longer just about reducing concentration risk, but about preparing portfolios for a world in which shocks are harder to predict and harder to contain.

Yara Aziz is Senior Economist at OMFIF.

Join OMFIF on 30 June for the Global Public Investor 2026 report launch.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.