Bond yields have jumped in recent weeks. But is this just usual volatility – what President Donald Trump once called ‘yips’ – or might it be the return of bond vigilantes?

While the Iran war’s oil price surge has lifted inflation and central banks are poised to raise interest rates, a case can be made for the yips. Longer-term market inflation expectation measures in key advanced economies are anchored, major central banks are still viewed as credible, safe asset demand remains considerable and the world is awash in capital. Demographics trends may lower potential growth and push real yields down.

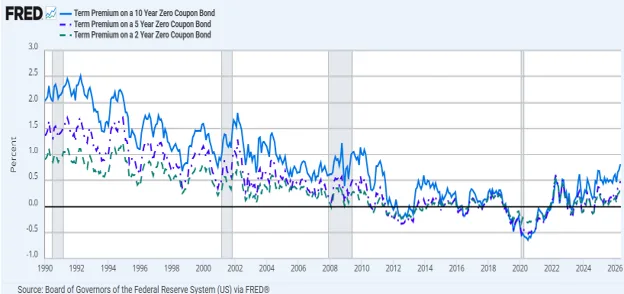

But serious consideration should be given to the proposition that change is afoot and the world should acclimatise itself to higher yields and term premia. Figure 1 shows why the jury is out. It highlights that the current level of the term premia is well below those of the past, but also the recent upward drift.

Figure 1. Current term premia is way down

Why might a fundamental upward break be occurring?

Inflation

The Federal Reserve has missed its 2% inflation target for five years. Forecasters and the dot plot typically assume mean reversion to 2%. But the latest oil price spike suggests that a return to the inflation target has once again been delayed.

In the words of the famous Saturday Night Live philosopher, Roseanne Roseannadanna, ‘It’s always something. If it’s not one thing, it’s another.’

Japan has finally managed to push inflation up and the Bank of England is struggling to keep a lid on prices. The European Central Bank is doing a better job, but it too faces challenges.

Simply put, inflation may well be on the rise. I have argued – along with Marco Annunziata – that the US may be closer to a 3% inflation regime, rather than its 2% target.

Central bank behaviour is shifting gear

The Great Moderation is over. The post-pandemic rate-hiking cycle and subsequent easing gyrated quickly. Quantitative easing in the wake of the 2008 financial crisis and pandemic is being unwound. Indeed, central banks are seeking to withdraw balance sheet support and incoming Fed Chair Kevin Warsh has signalled a desire to further shrink the Fed’s balance sheet.

Central banks, and their independence, are now often under political attack and increasingly facing the threat of fiscal dominance. Trump has declared: ‘This country should have the lowest interest rates in the world…We keep the world going.’ He has also said: ‘Every point is $600bn…If we went down two points, we don’t have a deficit anymore.’

Fiscal policy caught between a rock and a hard place

Almost a year ago, I noted that the fiscal chickens are coming home to roost. The point was to highlight looming unsustainable fiscal policies and outlooks in many large advanced economies.

In the no longer triple-A rated US, the outlook for the coming decade is more than 6% of gross domestic product annual deficits, aggravated by Trump’s so-called ‘Big Beautiful Bill’, followed by an even greater surge past the mid-2030s. Meanwhile, US political parties are incapable of acting responsibly – unwilling in effect to raise revenues or cut spending – and instead seemingly praying for a chimerical productivity artificial intelligence miracle or twiddling their thumbs in the face of a looming financial crisis that forces action.

America’s dubious fiscal dynamics raise obvious questions about whether Treasuries can still be seen as the world’s safe asset.

Japan’s gross debt is well over 200% of GDP, yet Prime Minister Sanae Takaichi is speaking about stimulus. In France and the UK, debt is already high, yet the populace wants to maintain or increase social spending while the prospects for revenue gains are limited given low growth and antipathy towards tax increases.

Rising debt burdens and higher interest bills will keep pressuring rates. Similarly, long-term purchasers of bonds – pension and insurance funds, primary dealers – are less willing to hold duration, such that greater issuance is in the hands of flighty hedge funds and asset managers.

Is there any wonder markets fret about fiscal dominance, higher inflation eroding debt – perhaps even leading to debt rescheduling – and the need to seek higher compensation? Who can forget the UK’s Liz Truss moment?

Geopolitics

Adding to these woes, the globe faces disorder, or what Eswar Prasad calls a doom loop. The US is no longer a trusted ally or partner. It is increasingly protectionist. US-China frictions are splintering the global trading system and the associated fragmentation adds to inflationary headwinds. Questions arise, even if overblown, about the dollar and currency market instability and whether America will retain supremacy over global payment rails. These factors may dampen cross-border capital flows.

The world may be witnessing an elevating term premium, more in line with past history. That elevation may be a structural feature, not a bug.

Mark Sobel is Chief Economist and Vice Chair of OMFIF. Thanks to Marco Annunziata for helpful comments.

Join OMFIF on 4 June for the chief economists briefing.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.