The exact timing of Christine Lagarde’s departure from the European Central Bank presidency remains uncertain. But keenness to succeed her is not, although there are many reasons why the post will probably be demanding and unenviable.

Multiple sources have coalesced on four front-runners: Klaas Knot, former Dutch central bank governor, Isabel Schnabel, ECB board member, Joachim Nagel, Bundesbank president, and Pablo Hernández de Cos, formerly Banca de España governor and now general manager at the Bank for International Settlements. Officials have hinted to OMFIF of a less likely fifth possibility, François Villeroy de Galhau, the outgoing Banque de France governor.

OMFIF has polled its advisers network, a broad international group of commercial bankers, current and former policy officials and central bankers, asset managers, development finance officers and others. Using a five-point scale, 20 respondents, including 11 from the euro area, marked these candidates against nine categories covering experience, knowledge and leadership, as well as the scope for domestic and wider European support (Figure 1).

Figure 1. Competencies of ECB presidency candidates

Ranked by survey respondents

| Competency | First choice | Second choice | Third choice |

| Monetary economics training | Hernández de Cos | Schnabel | Knot |

| Central banking experience | Knot | Hernández de Cos | Villeroy de Galhau |

| Capital markets knowledge | Nagel | Hernández de Cos/Knot | Villeroy de Galhau |

| Political capital | Villeroy de Galhau | Knot | Hernández de Cos |

| Reputation for leadership | Nagel | Villeroy de Galhau | Knot |

| Reputation for consensus building | Hernández de Cos | Nagel | Villeroy de Galhau |

| Ability to attract endorsement from other member states | Hernández de Cos | Nagel | Villeroy de Galhau |

| European credentials | Hernández de Cos | Villeroy de Galhau | Nagel |

| Crisis management experience | Nagel | Knot | Villeroy de Galhau |

Source: OMFIF advisers network poll. See full details of the results here.

Hernández de Cos, who has also come out on top of similar surveys, has a narrow lead. Ranking Nagel, Knot and Villeroy de Galhau requires a second decimal point, with the Bundesbank head taking second place and Knot, a favourite elsewhere, third. Schnabel, whose candidacy would need to navigate the single-term restriction for ECB board members, is the marginal outlier overall, though ranked second for monetary economics knowledge. Her departure would mean the ECB board also runs the risk of an arid period for gender balance.

The skillset nuances in the survey are diversely ranked and worth mapping to the incoming headaches. ‘Given the incomplete nature of the Union, Europe’s deeply entrenched, sticky problems, and the energy shock Europe is experiencing, I would not be surprised if the ECB’s role and mandate were recalibrated,’ a sovereign wealth specialist and former official from a multilateral development institution told OMFIF.

Another, who now advises a major asset manager, suggested that, ‘at the minimum, I think the ECB may need to slow down the pace of its passive quantitative easing if yields continue to rise, or rise at some later period’. Although several observers have suggested the traditional requirement to calibrate hawks and doves at the ECB council is outmoded, it could return with a vengeance if stagflation emerges, hammering central bank credibility and reawakening a north-south split on the merits of painful sound money remedies.

Nagel, Knot and Hernández de Cos equally qualified for the role

Lurking in the background are worries about the bond market’s tolerance of the permanent French budget deficit. While the ECB is structurally protected from fiscal dominance by the lack of a European finance ministry, it is equipped, with persistent objections from Germany, to intervene in disorderly euro area sovereign bond markets for the ‘protection of monetary policy transmission’. One of the candidates has suggested to OMFIF this topic will be a mainstay of the presidency job interview.

Nagel is an intriguing candidate in the poll on that basis, ranking first for both crisis management and capital markets knowledge. Nagel, who also wins the leadership category, unflappably helped run the complex vehicle to remove single-name credit risk from bank borrowing after the 2008 crisis. He has introduced a tentative open-mindedness on European joint borrowing, unthinkable of his predecessors, and could be in the best position to reconcile German objections with European utility. An economist poll respondent who helped design monetary union described Nagel as ‘the most obvious choice’. He is also a relatable communicator, a factor we haven’t directly measured but sits at the heart of most categories in the poll.

Knot, who leads the field in the central banking experience category, is a close runner-up in crisis management and capital markets knowledge, having helped devise, despite his instinctive hawkishness, unorthodox remedial ECB tools such as the pandemic emergency planning programme and transition protection instrument, and presided over important work on non-bank finance risks at the Financial Stability Board. Knot is one of the most polished central banking communicators of the last two decades in view of his 14 years as head of De Nederlandsche Bank and his Dutch proclivity for plain speaking.

Overall poll winner, Hernández de Cos, who was at the ECB’s governing council between 2018 and 2024, ‘combines poise, intellectual depth and hard-earned experience from managing Spain’s crisis and navigating a highly fractious political environment’, according to a former multilateral development institution official, who spotted him as a notable talent early in his Banco de Espaňa career.

Hernández de Cos won four of the poll categories (monetary and economics training, consensus building, non-domestic endorsement scope and European credentials), came second in two (capital markets knowledge and central banking experience) and third for the heavily contingent factor of native political backing for the nomination. Some observers have suggested Pedro Sánchez, Spain’s socialist prime minister, may be reluctant to sponsor a candidate who was appointed Banco de Espaňa governor by the conservative Partido Popular.

A German duality?

An important part of the debate over the choice of the next ECB president surrounds the issue of whether Germany would be infringing European Union norms if it held the presidency of the ECB and of the European Commission at the same time.

If a German took over as president of ECB early next year, on the assumption that Lagarde steps down early, and European Commission President Ursula von der Leyen remains until the end of her term, this would mean that Germany would hold two senior positions for almost three years. If, however, she stayed on until the end of her term, that would lower the overlap with Lagarde, and possibly aid Nagel’s position.

The chances that von der Leyen could leave Brussels early – possibly to take over as German federal president next year – seems somewhat low in view of the considerable political complications that would cause in Germany and across Europe.

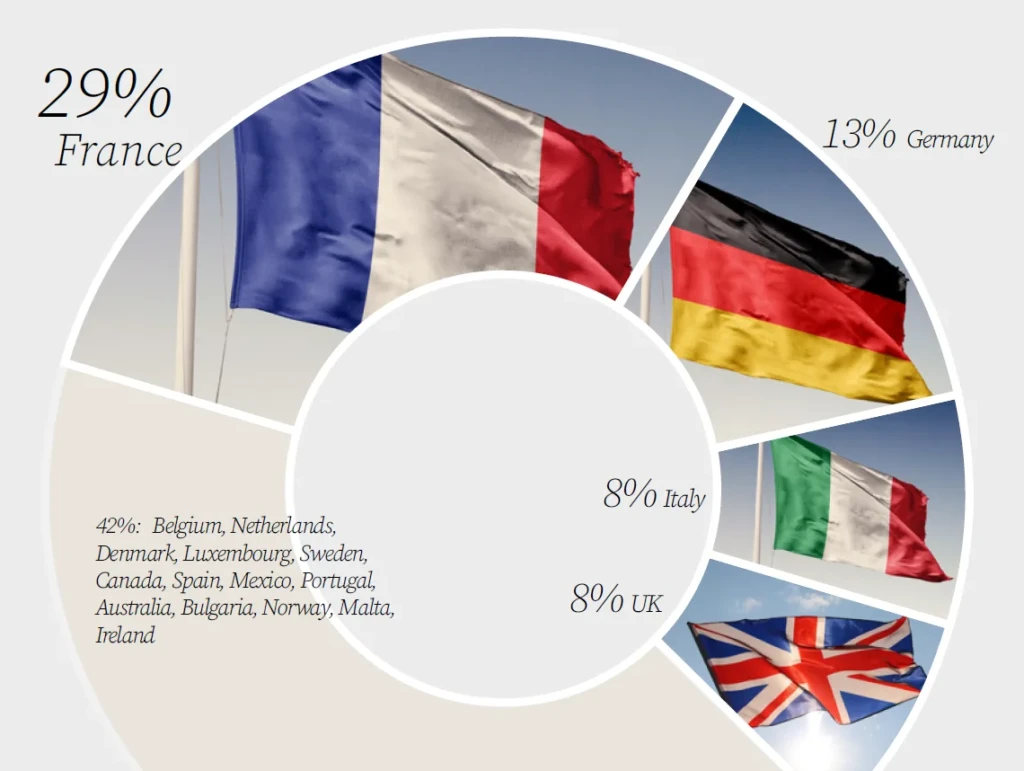

If a German duality were to ensue in Brussels and Frankfurt, that would not be extraordinary in Europe’s institutional history – and would help overcome a German lag in filling Europe’s top jobs. Germany has held the top positions in the 10 institutions surveyed for a cumulative total of 73 years, less than half France’s recorded score of 183 years (Figure 2).

Figure 2. France has historically dominated top positions in Europe

Percentage of top roles held by European countries, 1963-2026

Note: Institutions include Bank for International Settlements, International Monetary Fund, Organisation for Economic Co-operation & Development, Nato, European Commission, European Investment Bank, European Parliament, European Council, European Bank for Reconstruction & Development and European Central Bank. See full details here.

Source: OMFIF analysis

Duality of presidencies has been a French speciality in the post-war period. Statistical analysis shows that France has occupied simultaneously two more presidencies in every year since 1963, the sole exception being a seven-year period in 2012-19. The discrepancy is even larger when the totals are adjusted for the economic size of individual countries.

Europe is entering a Hobbesian multipolar world accompanied by its own historic policy errors rendering it vulnerable on energy and defence. Lagarde had been rumoured to be stepping down earlier than the October 2027 end date of her term. Almost certainly, an energy-price-driven economic challenge will require Lagarde’s attention before she goes, to conclude a tenure that has already spanned negative interest rates, the Covid-19 pandemic and an inflation shock.

Her successor will require all the abilities of a career central banker – as well as extra capacity to navigate the ever more arduous repercussions of fluctuating geopolitics.

John Orchard is Chairman of OMFIF’s Digital Monetary Institution and David Marsh is Chairman of OMFIF. With thanks to Conor Perry and Simon Hadley.

This article is the third instalment of a series on the ECB presidency. Read parts one and two.

Join OMFIF on 22 April to examine the economic outlook for France: policy choices in an election cycle.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.