Respondents to OMFIF’s 2026 Public Sector Debt Outlook Survey are markedly more confident about demand for euro-denominated paper than for dollar-denominated offers. More sovereign, sub-sovereign, supranational and agency issuers said they could not predict dollar subscription rates than expected them to rise; for the euro, most expect subscription ratios in line with 2025 levels, with a sizeable minority anticipating stronger demand.

Against this backdrop, there is unusual agreement among respondents of expected increased allocation to central banks and official institutions in Asia Pacific. In our relatively euro-centric sample of 35 issuers, this suggests expectations of currency diversification in emerging market reserve management.

The fading case for dollar issuance

Throughout the 2010s, SSA issuers, particularly supranationals like the European Investment Bank, funded large proportions of their borrowing needs in dollars. Three factors drove this decision.

The first was predictable excess demand for these issues from a global investor base, including the global reserve management community. The second was multi-currency issuance strategies being attractive from the perspective of demand-base diversification. Third, historically negative levels in the euro-dollar cross-currency basis – the discount applied on top of the standard interest rate differential when swapping cashflows between euros and dollars – allowed issuers to lower their funding costs by issuing in dollars and swapping back to euros with a cross-currency basis swap, thereby earning the basis.

The euro-dollar cross-currency basis is now closer to the zero level that conventional economic theory implies. Even so, one-third of respondents flagged changes in the basis and foreign exchange swap market conditions as a top three funding concern. Uncertainty over all-in dollar funding costs changing due to movements in cross-currency basis adds to the broader anxieties around the predictability of demand for dollar-denominated SSA paper.

While the benefits of investor base diversification will continue to support some level of dollar issuance, as US foreign policy belligerence reorders global defence alliances and causes reconsideration of economic dependencies, investors appear to be reconsidering their relationship with dollar-denominated SSA issuance.

Examining dollar SSA syndications between 2024 and 2025, bid-to-cover ratios fell slightly for dollar issuance – meaning that the level of excess demand for new bonds fell. Changes in initial price talk to reoffer spreads also fell – meaning that the issuers were able to extract less price improvement between initial guidance and final pricing – suggesting a softening in the market power of SSA issuers marketing dollar deals. The same metrics moved inversely for euro-denominated issuance, indicating strengthening demand.

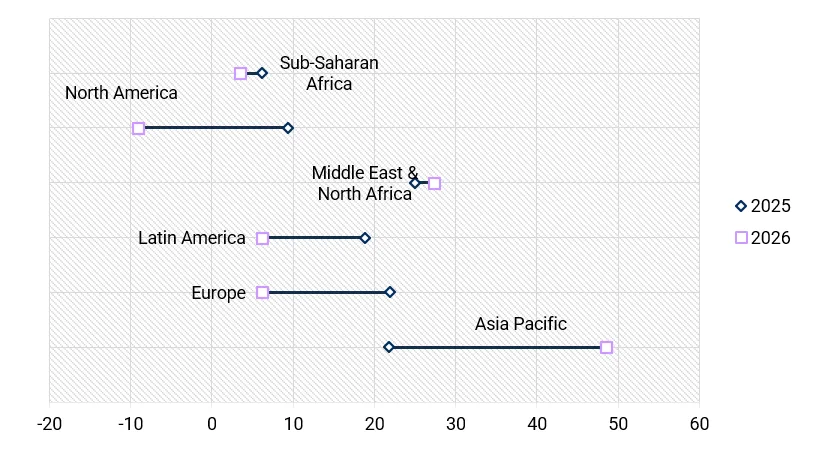

Issuers are taking note. A net 10% of issuers in our survey expect distribution to North America to fall. A year-on-year decline of 21 percentage points makes North America the only region where our survey respondents expect to decrease allocation relative to 2025 (Figure 1). While expected issuance to North America is not a perfect proxy for dollar-denominated demand, it is suggestive.

Figure 1. Issuers expect to decrease allocation in North America

How do you expect the distribution of your bondholders to change by geographical region in 2026?

Source: OMFIF Public Sector Debt Outlook Survey 2026

Conversely, issuers expect to lean far more heavily on investors in Asia Pacific. A net 48% of respondents expect to increase distribution to the region in 2026, which constitutes a year-on-year increase of 34pp.

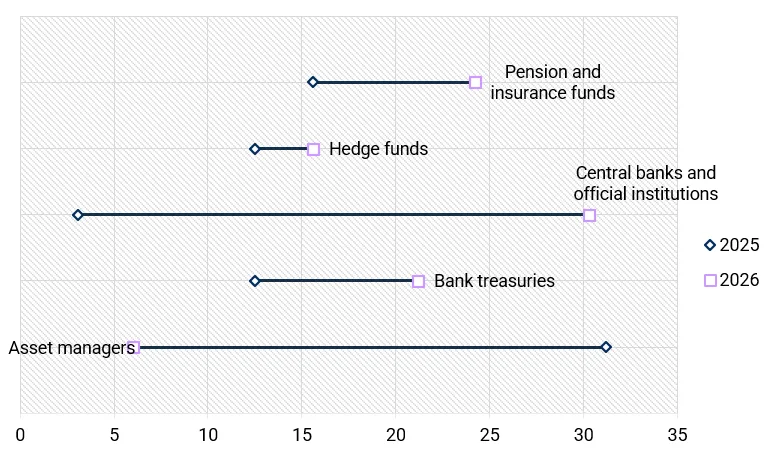

The figures for allocation by investor type add interesting context. A net 31% of survey participants expect to increase allocation to central banks and official institutions (Figure 2). Crucially, issuers expecting higher allocation to official institutions are also the most likely to expect to increase allocation to Asia Pacific.

Figure 2. Higher allocation to official institutions expected

How do you expect the composition of your bondholders to change in 2026?

Source: OMFIF PSDO Survey 2026

Signals beyond regional rebalancing

Among a set of largely European institutions, this correlation potentially indicates something larger than regional rebalancing. The SSAs in our sample appear to expect that, as emerging market central banks diversify away from dollar-denominated assets, the euro, as the second-largest reserve currency, stands to benefit.

Correspondingly, stronger expectations for euro subscription rates, and weaker expectations for dollar subscription rates go hand in glove with increased expectations of allocation to Asia Pacific central banks. As the US adopts a more inward-looking stance geopolitically and economically, structural demand for dollar-denominated assets weakens and SSAs appear to anticipate that this represents a structural tailwind for their euro issuance.

While the shift away from the dollar will not happen overnight, the case for diversification away from the dollar for emerging market reserve managers continues to strengthen. In such an environment, sovereigns and SSAs issuing in euros stand to benefit.

Conor Perry is an Economist at OMFIF.

Join OMFIF on 31 March to examine the renminbi in the international monetary system.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.