The incoming Andy Burnham government in the UK will initially have sufficient authority to avoid the mistakes of its predecessor. It should avoid immediate fiscal pledges (such as measures to help low earners with the cost of living) and involve the Office for Budget Responsibility at an early stage with an assessment of all the fiscal pressures. It should not try to raise extra revenue quickly through changes to capital taxes: any such changes should be the result of carefully executed tax reform.

Although it is contrary to its instincts, the most sensible course would be to fix the public finances first and only then to increase funding for the government’s preferred causes. Failure to do so risks the remaining three years of this parliament being dominated by fiscal crises.

Such a disciplined approach to policy making will not be easy. The wishes and instincts of the Labour party are to spend more on public services, to increase public investment, not to curb benefit and pension expenditure (despite mounting evidence that current policies are unsustainable), and generally to increase the wellbeing of ‘working people’ through an early package of measures to reduce the cost of living. They would prefer to finance additional current and capital spending mainly by increased borrowing, but also by greater taxes on wealth and high incomes.

A Burnham government would add to these aims a push towards more devolution of powers, although the precise nature of this devolution and any fiscal consequences remain wholly unclear. The constraint on these aspirations is fear of a crisis in the bond markets. The way that the markets quickly upended the 2022 Liz Truss experiment of massive unfunded tax cuts is having its greatest effect on a government whose aspirations and instincts are to increase public spending.

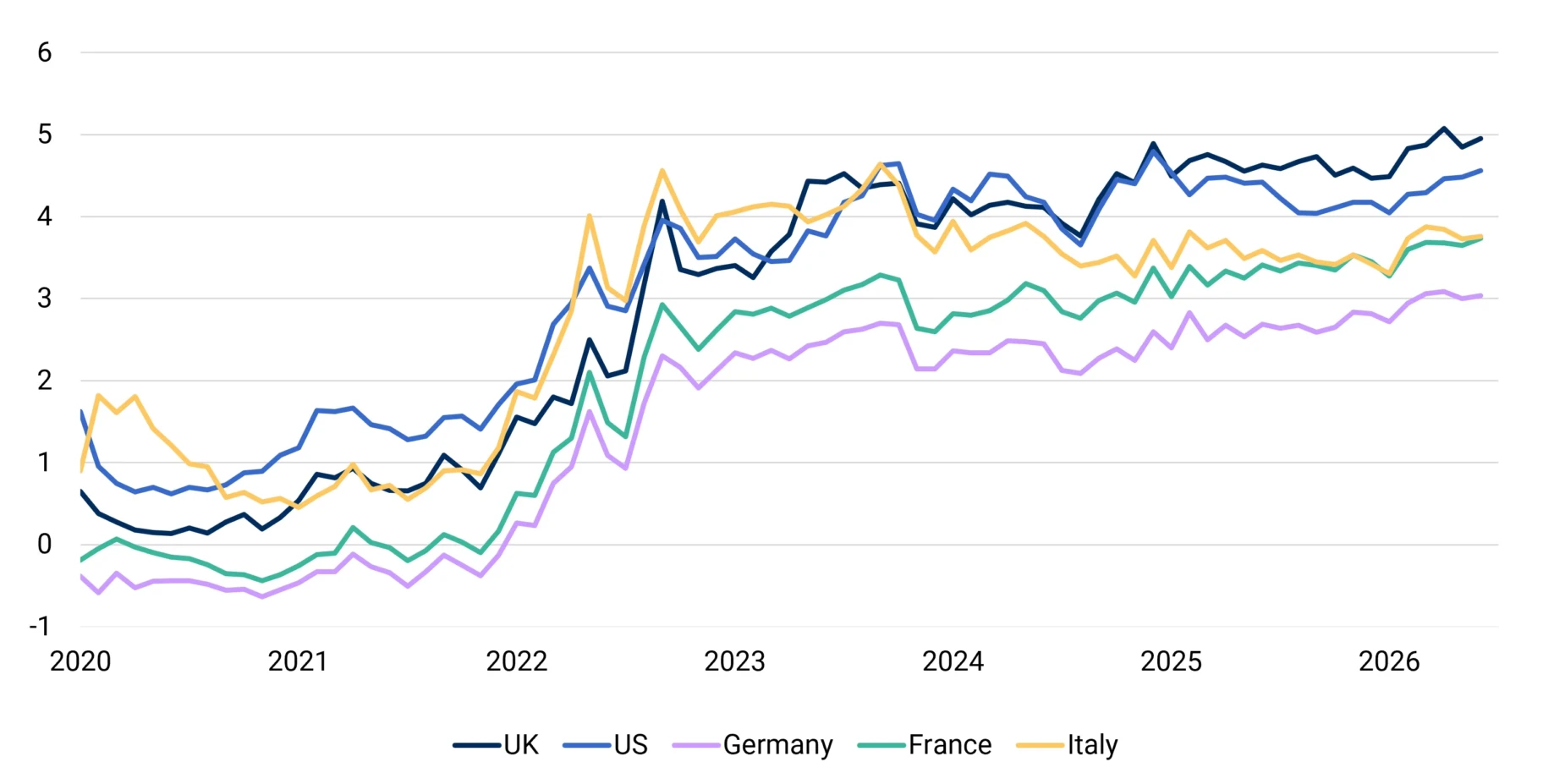

Higher bond yields than European peers

Having made an unwise pledge not to increase the main rates of income tax, value added tax or corporation tax, the Keir Starmer government financed its significant increases in public expenditure, especially on health, by two large tax rises – in employers’ national insurance contributions and, by freezing income tax allowances, in forecast income tax receipts. The fiscal rules have been obeyed to the letter, but not the spirit, by partly being achieved at the end of the forecast period largely by assuming unrealistically low growth in spending on public services in the final year.

The bond markets have broadly accepted this overall approach, but at a significant price: UK 10-year bond yields had been close to those of comparable European economies with broadly similar, or even more serious, fiscal problems. From late-2024 the UK 10-year bond yield has risen to be over one percentage point higher than in France or Italy (Figure 1). The UK government has to sell around £250bn gilts each year to cover its deficit and maturities at a time when the independent Bank of England is unnecessarily reducing its holdings of gilts by £70bn a year.

Figure 1. UK 10-year bond yields exceed European peers

10-year borrowing costs, %

Source: London Stock Exchange Group

This is a massive ask of the markets. Furthermore, around 30% of outstanding gilts are held by non-residents. This proportion is likely to rise as the Bank of England’s stock of gilts falls and with reduced demand from domestic defined benefit pension schemes. The need to satisfy foreign purchasers of gilts will be increasing.

Policy changes ahead of the next budget

The Burnham government will need to proceed carefully. It appears ready to maintain the pledge not to raise the main rates of income tax and VAT, and it cannot repeat the freeze of income tax allowances or realistically increase employers’ NICs again. In its assessment of the UK’s public finances the OBR should assess the consequences of the war in the Middle East and recent trends in the public finances, where borrowing has so far this financial year been above the OBR’s forecasts.

It is quite possible that this assessment will show that policy changes are needed to maintain fiscal headroom. Once this exercise is complete the government can devise an autumn budget that takes account of all existing commitments and any spending changes plus any need to rebuild headroom.

The autumn budget should take full account of the requirements for defence and any changes in spending – in whatever direction – following the second part of the Milburn report due in September. It would be counter-productive to have a budget that is perceived by commentators and markets as having not properly allowed for known commitments on spending, such as defence.

The OBR’s fiscal projections accompanying a budget cover four full financial years after the current one and, therefore, will cover developments beyond the later years of this parliament into the next. While the government sticks to its target of defence spending reaching 3.5% of gross domestic product by 2035, commentators and market participants concerned about the credibility of the public finances will be looking for progress towards that goal.

Options for Burnham

The government’s fiscal rules now target public sector net financial liabilities and there may be attempts to justify additional public investment – even in areas like defence – where there could be a liquid or illiquid financial asset to set off against the cost of the investment. This may give the Burnham government scope to increase investment, but it must expect the markets to subject the quality and value of the financial assets to intense scrutiny. There have been plenty of instances of UK public investments not having the value initially attributed to them.

Given its aspirations and the fiscal pressures it faces, the Burnham government may want to raise taxes. The least harmful way to do so would be an increase in the main rates of VAT (as proposed by the Organisation for Economic Co-operation and Development) or income tax. It should be wary about forecasting early increases in capital taxes – such as capital gains tax or property taxes – as alterations in behaviour can reduce yields markedly.

An autumn budget that took full account of fiscal prospects, including the pledges on defence, would be a difficult exercise for ministers and would, at least initially, disappoint many of their supporters. But even on the political level it would be far preferable to announcing policy changes early on only for a series of corrective measures to be necessary later.

Finally, there is potentially a significant bonus for the government in the form of lower debt interest payments, now running at over £100bn per year and rising, if it can reduce the yield on gilts at least to something closer to the rate paid by its European peers. One way to do this would be to stop the habit of concentrating compliance with the government’s fiscal rules to the final year of its fiscal plans. Earlier progress, particularly in moving more rapidly to balance on its current transactions, would help reduce misgivings in the markets and could reduce the expensive premium on UK gilt rates.

Peter Sedgwick was a senior Treasury official, a Vice President of the European Investment Bank 2000-06, Chair of 3i Infrastructure PLC 2007-15 and Chair of the Guernsey Financial Stability Committee 2016-19.

Join OMFIF on 22 July for The OBR on fiscal risks and sustainability in the UK.

Image credit: House of Commons

Interested in this topic? Subscribe to OMFIF’s newsletter for more.