Central bank reserve managers appear to be inching away from the dollar, but without enthusiasm. As the sun sets on investors’ increasingly loveless relationship with TINA – ‘there is no alternative’, the ascendant successor, TARA – ‘there are reluctant alternatives’ emerges as quite a low-burn affair for now. TIGA, a ‘good alternative’, is available, but is quite likely to stay on the shelf.

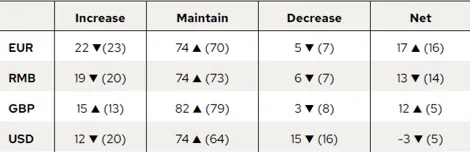

OMFIF’s 2026 Global Public Investor survey has for the first time revealed a marginal net intention of 3% to divest the US currency, which accounts for a still-dominant total of around 58% of reserves. Asked to pan out a 10-year horizon, respondents show a net decrease of 8%. This shows that reserve managers are spreading different dollar functions across a set of partial alternatives: the dollar remains the liquidity anchor, gold is the strategic hedge, the euro has the strongest potential if Europe can address the safe-asset gap and the renminbi is the trade-linked emerging-market alternative.

Figure 1. Net intentions to change currency holdings

Over the next 1-2 years versus the next 10 years, are you planning to increase, decrease or maintain your exposure to the following currencies? Share of respondents, %

Source: OMFIF GPI 2026 survey

Note: Brackets show results from 2025. Columns may not add up to 100% due to rounding.

Talk of ‘de-dollarisation’ may be overdone at this stage. The currency still has more than double the share of reserves relative to the US’s share of the global economy, at around 26%. Yet it remains one of the themes most likely to prompt sharp debate in OMFIF roundtables. Dollar defenders point to the unparalleled depth and liquidity of its safe asset market, broader dollar-denominated securities markets and the infrastructure to exchange, hedge, store and remit dollars.

The currency, unlike the euro, is also backed by a powerful unitary state and a defence budget of around $1tn a year. Non-defenders point instead to persistent US fiscal deficits, the risk of currency depreciation or inflation, and the use of US assets and financial infrastructure as a lever of foreign policy. These concerns predate President Donald Trump’s second term and were sharpened by the freezing of Russian central bank reserves after the full-scale invasion of Ukraine.

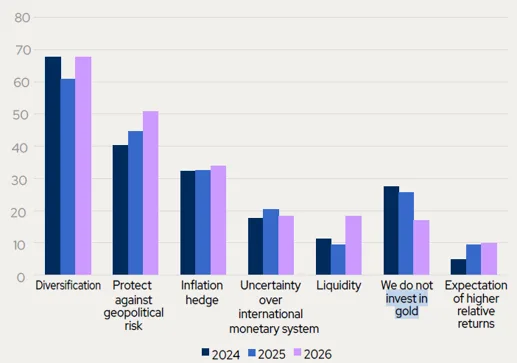

The main beneficiary is gold. Among the survey panel of 74 central banks, returns are only a marginal motivation: 10% cite higher relative returns as a reason for holding gold, up slightly from 9% last year. By contrast, 51% cite geopolitical risk, up from 45% in 2025, while 68% cite diversification, up from 61%. Physical gold holdings have also risen, with 82% of central banks now holding physical gold, compared with 71% last year.

Figure 2. Gold rises as a safe haven

Why do you invest in gold? Share of respondents, %

Source: OMFIF GPI 2025-26 surveys

The renminbi, which central banks expect to account for 5% of the average portfolio in 10 years, is likely to climb, with net 13% intending to increase holdings over the next 12-24 months – broadly unchanged from a net 14% last year. Given the size of the Chinese economy, now broadly equivalent to the US, this is arguably the reserves shoe that hasn’t dropped. The 10-year intention to increase renminbi holdings has also held steady at 32% of respondents. The net balance has edged up two percentage points from last year.

A similar story faces the euro. Net intentions to increase holdings in it, which were flat in the negative interest rate era of the early 2020s, have edged up a percentage point to 17% from last year. The 10-year net intention has palpably increased to 21% from 12%. It may be that reserve managers have hopes for – among other initiatives – Europe’s Savings and Investment Union drive.

Post-pandemic progress

An improbable change would deliver much more euro demand from reserve managers. Asked if the European Union were to become a ‘permanent, large-scale issuer’ of safe assets, 50% of respondents and 55% of those for whom the question applied, said they would increase their willingness to hold euro-denominated reserve assets. Despite the progress towards such an outcome after Covid-19 via the time-limited NextGenerationEU initiative, objections to fiscal union remain strong, especially in Germany. Adventurous discussions have started as part of the Markets in Crypto-Assets regulation 2.0 review at the European Commission to circumvent the impossibility of collectivised European sovereign borrowing in traditional bond markets via changes to the stablecoin framework.

As it stands, MiCA obliges 60% reserves for systemic stablecoin issuers to be placed in European bank deposits. A design which more closely resembled the US framework under the Genius Act would create a synthetic euro safe asset. Reserve managers in our survey, however, continue to show very little interest in digital assets, essentially unchanged from last year: long-term interest has risen only from 10% to 13%, while 92% still do not invest. Among other disincentives, a universal ban on stablecoin yield keeps potential central bank investors away. Commercial banks, alleging deposit flight risk, continue to lobby successfully against a change to this policy on both sides of the Atlantic, for now. An attempt to readdress it in the Clarity Act has helped slow the Bill down in the Senate, risking its safe passage before the summer recess and then mid-term campaigning.

The global competition not just between currencies but their electronic formats look set to run for some time. As our survey reveals a growing wariness of the dollar-denominated stablecoins continue to dominate that market, with $11tn in annual transaction volumes, and 99% market share. For official reserves, however, digital assets are still not the alternative reserve managers are looking for.

Regional nuances reinforce the TARA view

Our survey reveals striking regional nuances to reserve manager intentions. In the short-term, Europe for example, actually intends slightly to increase its dollar holdings [18%]. Europe’s currency, meanwhile, is the favoured alternative to the dollar in Africa and Latin America for the short term, [42%, and 21%], with material interest in the renminbi too [former 42%, latter 14%]. African reserve managers, many of whose economies are important clients of China, expect to very significantly increase renminbi holdings over the next 10 years [75%]. Similarly, over the longer term, Asia Pacific also stands out, with 57% intending to increase renminbi holdings.

It is important to note that Asia Pacific accounts for about $8.3tn of reserves and sub-Saharan Africa for $234bn. This suggests the renminbi story may be regional rather than universal, but still significant where China’s financial links are deeper. One global South deputy central bank governor at a recent OMFIF discussion said their institution was reallocating not only away from the dollar, but also away from US financial institutions, turning instead to Chinese banks in Hong Kong.

It’s clear the dollar remains king. However, as the global economy changes and the US currency starts to look a little less like a de facto global public good and more like a sovereign or operations risk, reluctant alternatives are expected by reserves managers potentially to become good ones medium-term.

John Orchard is Chairman of the Digital Monetary Institute and Yara Aziz is Senior Economist at OMFIF.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.