At the Bundesbank, we prioritise liquidity and safety when managing foreign exchange reserves. The choice of foreign currency and the type of investment is guided by the objective that the Bundesbank can meet foreign currency obligations fully and independently even in times of market stress. Return considerations are usually a secondary motive.

Against this background, we regularly review our reserves to assess their size, currency composition and risk structure. In recent years, the foreign exchange reserves of the Bundesbank have been diversified into additional currencies under strict criteria to improve the risk structure of the portfolio. Currently, our dollar reserves account for around 80% of our foreign exchange portfolio, reflecting the currency’s leading role in the global reserve system.

Regarding our gold holdings, liquidity and safety are likewise key principles within our framework. Although we are not actively trading our gold reserves, the increased gold purchases by other central banks over the last years highlight the growing role of gold as an asset class in portfolio management. Against this background, we support initiatives to create more liquid trading hubs for gold.

International role of the euro

The euro’s international role is growing steadily. In its 2026 study, the European Central Bank reported that the euro’s share across a broad set of indicators of international use rose to around 20%, making it the second-most important currency. In 2025, euro-denominated international debt reached record levels, and the euro became the leading currency in green and sustainable bonds. Foreign portfolio inflows in the euro area also hit near-record highs.

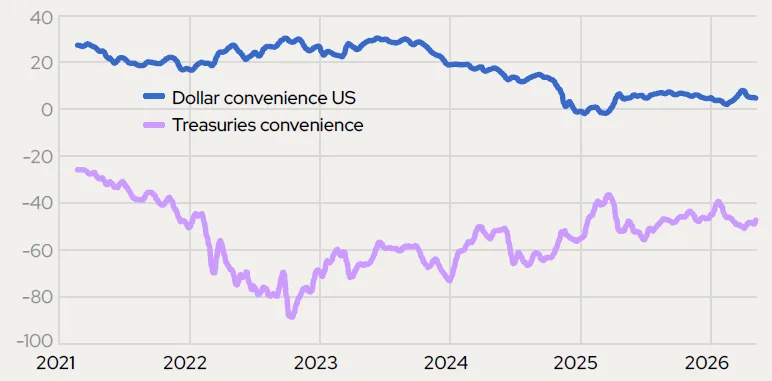

A currency’s appeal to investors can be measured by its ‘convenience yield’, which reflects non-monetary benefits like safety, regulatory advantages as well as collateral and liquidity features. A premium associated with these properties is typically higher the smaller the free float of the underlying government bonds. Empirical estimates indicate that the convenience yield of the dollar, i.e. the extra value investors place on holding dollar-denominated risk-free assets relative to euro risk-free assets, has been broadly positive over the last five years (Figure 1). However, it has fallen continuously since late 2023, suggesting that holding dollar assets no longer provides significant non-monetary benefits over euro assets.

Figure 1. Dollar convenience has fallen in recent years

Dollar and US Treasury convenience yield relative to euro and Bunds since 2021

Source: Deutsche Bundesbank

Note: The US Treasury convenience yield can be expressed as the dollar convenience yield plus the difference of the US and the Bund swap spreads.

At the same time, the convenience yield of US Treasuries relative to German Bunds has been largely negative. The measure peaked in 2022 in an environment in which German governments bonds were increasingly scarce amid the Eurosystem’s asset purchases. As the Eurosystem has reduced its balance sheet since then and fiscal authorities in Germany have stepped up government spending at large scale, Bunds have become more readily available, slightly lowering their specialness.

The euro’s potential in global markets

Europe has an opportunity to further strengthen the euro’s position in the shifting global order, provided that policy-makers create the necessary conditions to make the euro more attractive. The focus should be on fostering Europe’s economic foundations based on a strong legal and institutional integrity. Completing the single market, especially the Savings and Investment Union, is key to creating deeper and more liquid capital markets.

The Eurosystem is also committed to strengthening the euro’s appeal in global markets. Through the recently enhanced EUREP repurchase agreement facility, the Eurosystem provides backstop liquidity, encouraging reserve managers to invest and trade in euro sovereign and agency bonds. Moreover, the digital euro and wholesale central bank digital currency are important steps to strengthen the euro’s footprint in the digital and tokenised age and to reduce dependencies on non-European payment infrastructure providers. Above all, the Eurosystem’s independence and commitment to price stability ensure the euro remains a reliable global anchor of stability.

Karsten Stroborn is Director General of Markets at Deutsche Bundesbank.

This article featured in OMFIF’s Global Public Investor 2026.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.