The US Treasury market has long served as the world’s financial anchor – deep, liquid and reliably stable. That reputation for placidity is becoming harder to sustain. America is borrowing at a pace that would have seemed extraordinary a generation ago, and the buyers who once absorbed that paper without blinking are quietly stepping away.

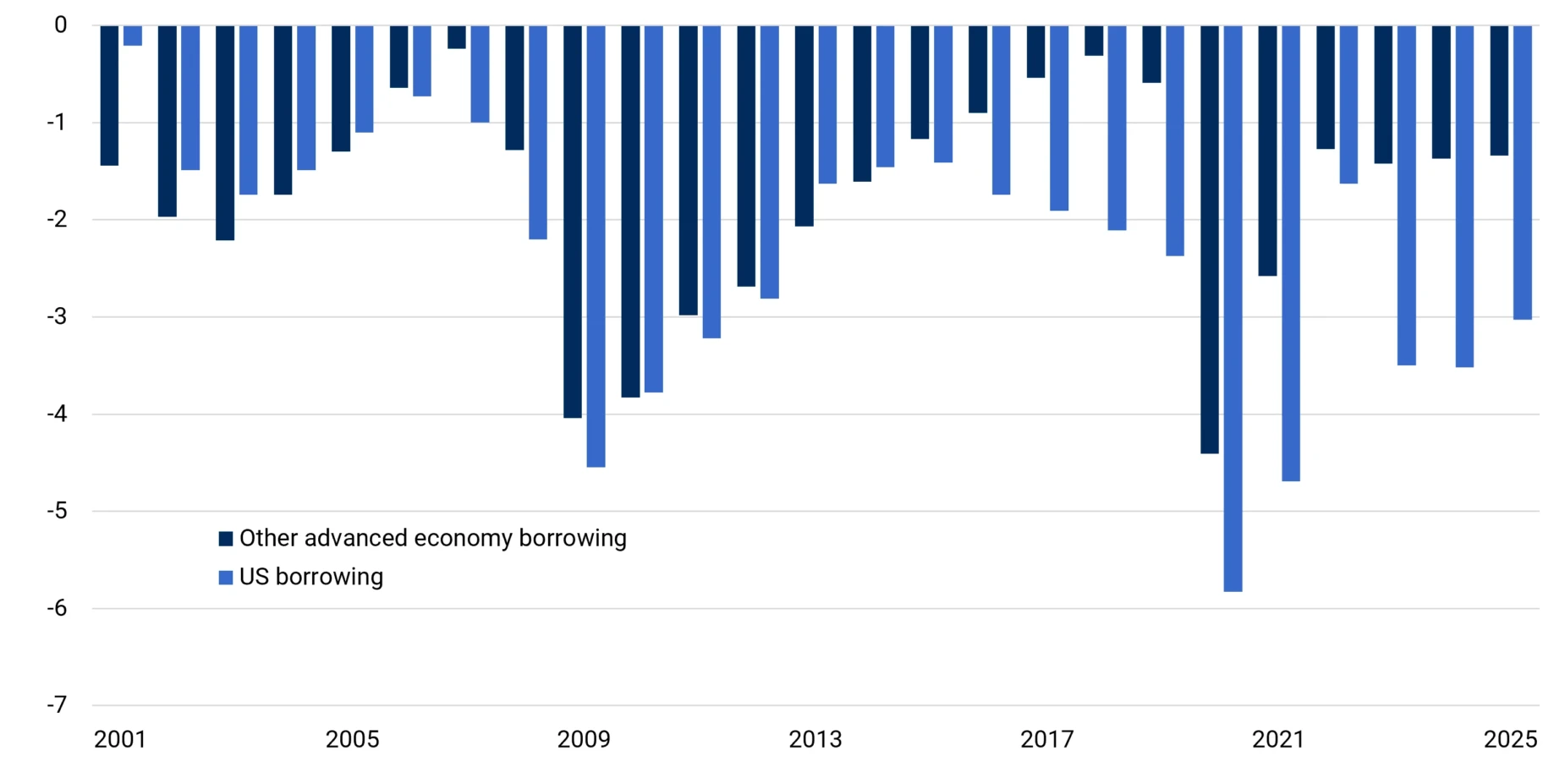

The scale of the fiscal expansion is astonishing. Publicly held US debt has risen more than fourfold since the 2008 financial crisis and now tops 100% of gross domestic product – a threshold last breached in the aftermath of the second world war. America borrows more than every other advanced economy combined (Figure 1).

Figure 1. US is the world’s biggest borrower, and it’s not even close

General government borrowing as % of advanced economy GDP, 2001-25

Source: International Monetary Fund

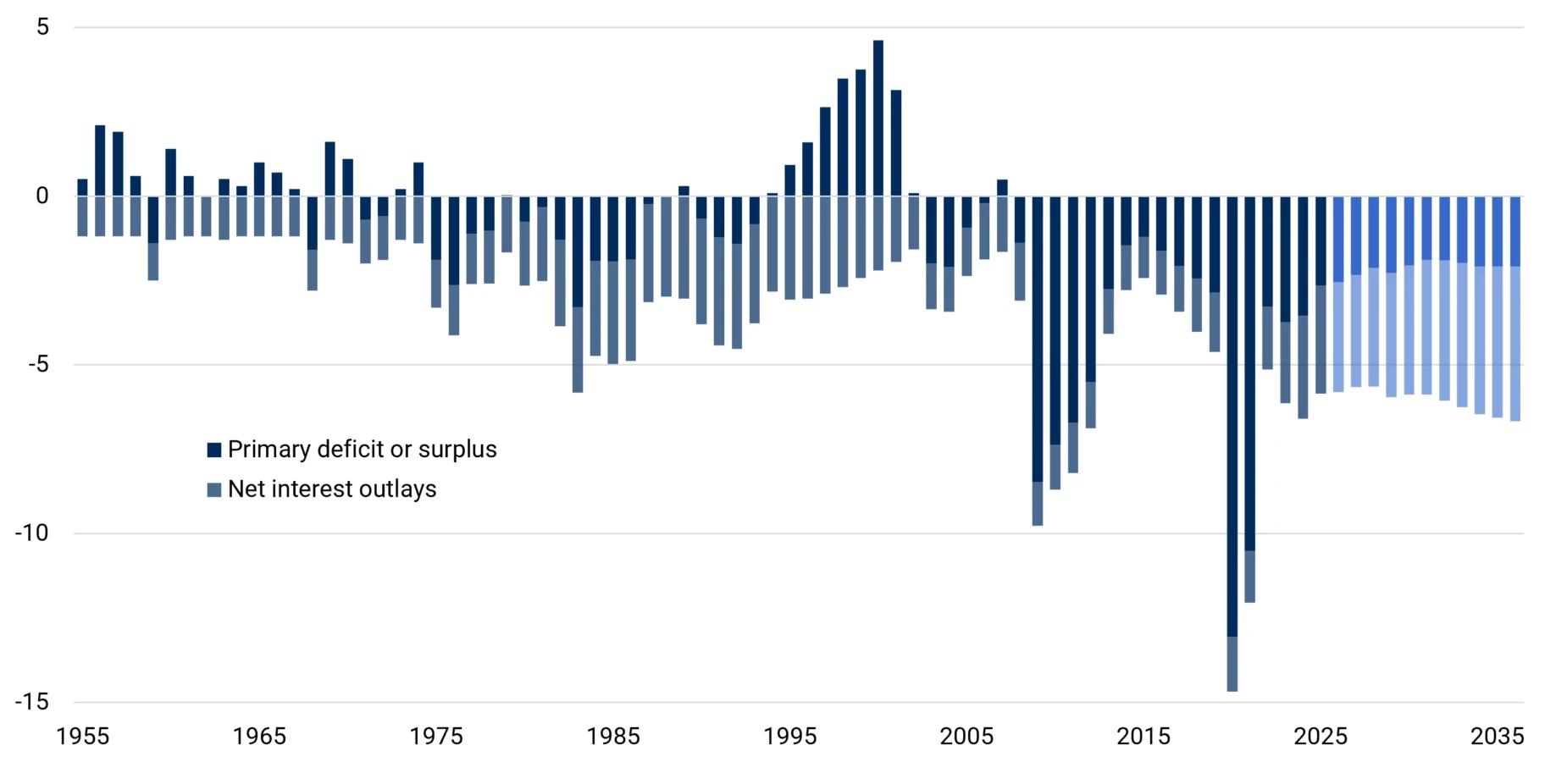

There is no let-up ahead (Figure 2). Where markets once imagined a Republican counterweight to Democratic spending, that illusion has been shattered. The latest update from the Congressional Budget Office shows President Donald Trump’s policies widening the federal deficit by $1.4tn over the coming decade, a 6% increase on the previous forecast from January last year – and that estimate predates the courts’ dismantling of his tariff agenda.

Figure 2. America’s fiscal trajectory is worsening

US total and primary deficit or surplus as a share of GDP, 1955-2036

Source: Congressional Budget Office, Office of Management and Budget

What makes the situation newly dangerous lies on the demand side. Foreign central banks, once voracious accumulators of dollar reserves, have slowed their purchases as the trauma of the late 1990s fades from memory. Increasingly strapped petrostates are drawing down their holdings. The Federal Reserve, having spent years as the buyer of last resort, is still shrinking its balance sheet. Pension funds and insurers, long-duration buyers with little interest in market timing, are playing a diminishing role – one that demographic shifts, as populations age and draw down savings, are only accelerating.

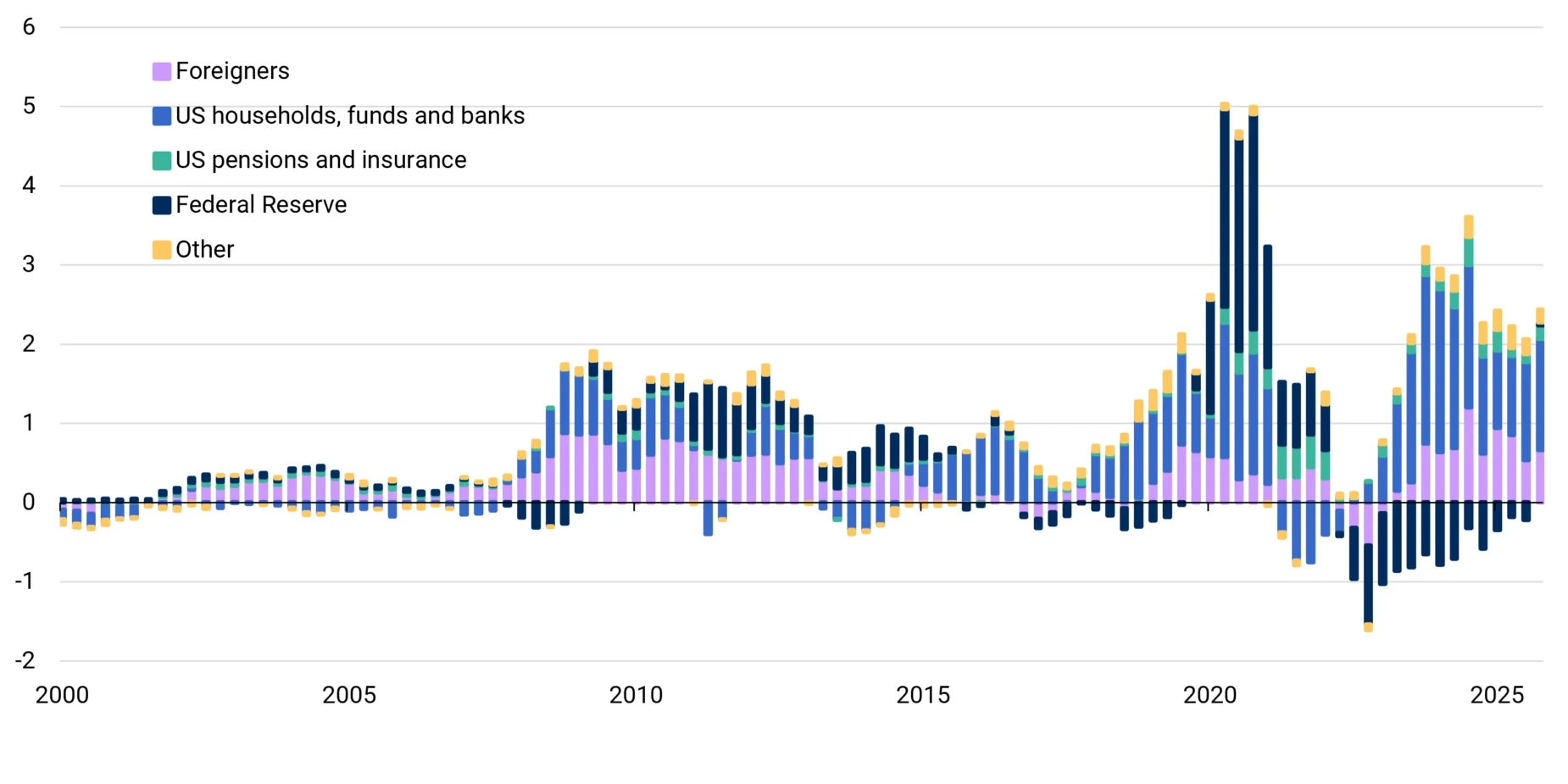

The gap is being filled by investors of a very different temperament. Foreign commercial buyers, hedge funds, private asset managers and intermediary banks have stepped up – but they are, by nature, price-sensitive (Figure 3). They buy when yields (or basis spreads) are attractive and sell when conditions turn: a coalition united by the fact that none of them regard Treasuries as a permanent, unconditional holding. That is a fragile foundation beneath the world’s supposedly safest asset.

Figure 3. ‘Price-sensitive’ investors now take bulk of Treasury issuance

Net Treasury purchases, four-quarter rolling sums, $tn, 2000 Q1-2025 Q4

Source: Federal Reserve, US Treasury, Bloomberg

The picture is complicated by structural shifts in the global economy. Governments elsewhere are loosening their purse strings, particularly on defence. Firms at the centre of the artificial-intelligence buildout, the energy transition and the commodities boom are driving a wave of capital expenditure not seen since the industrial era, and corporate borrowing is undergoing a step change. The result is a global scramble for long-term capital in which America’s Treasury and Silicon Valley’s hyperscalers are competing not only with each other, but with governments in Berlin, Tokyo and beyond.

None of this implies the greenback is doomed to decline – in fact, the opposite could prove true. The US is unlikely to default on its debt: the bulk of it is denominated in a currency Washington can always create more of, meaning any real default would be a political choice – a failure to raise the debt ceiling, say – rather than an inability to pay.

But if interest rates at the core of the global financial system settle at a structurally higher floor, punctuated by spasmodic bouts of volatility, countries without the privilege of issuing the world’s dominant reserve currency could find themselves severely crowded out. To update John Connally’s infamous warning about the dollar: it may be our Treasury market, but it’s your problem.

What does this mean for currency markets? Once the dust settles in the Middle East, many participants expect trading to revert to fundamentals: relative shifts in growth, employment and inflation. They may find themselves wrong-footed instead by continued bond-market lurches that have little to do with any of these. Foreign exchange traders and corporate hedgers have spent a decade waiting for interest rates to return to normal. The unsettling possibility is that they already have.

Karl Schamotta is Chief Market Strategist at Corpay Cross-Border.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.