Analysts and markets were in unison following Kevin Warsh’s first press conference as chair of the Federal Reserve – he’s a hawk, orthodox, not the president’s sock puppet. But the hawkish interpretation is premature and it may be wrong. Time will tell.

This was Warsh’s first Federal Open Market Committee meeting. Reputations are made up front and credibility is crucial for a Fed chair. Warsh commented on how the Fed has missed its inflation target for five years, inflation has just hit 4% and labour markets are perky. Of course, given this backdrop, he emphasised ‘price stability’.

Warsh may arguably be a hawk in his heart and have grounds to argue that Fed forward guidance overly spoon-feeds markets. But even if Donald Trump was restrained following the FOMC meeting and accepted that rate cuts were not on the table, the shadow of his jawboning and wish for lower rates still hangs over Warsh.

Accordingly, a press statement that did not feature forward guidance, Warsh’s failure to submit a dot to the dot plot and no comment on the future rate outlook arguably suited his interests. What would Trump have said if he learned that Warsh submitted a dot that didn’t call for a cut? Meanwhile, leaving other FOMC members to submit dots, with nine calling for a hike, to dominate the post-FOMC discussion caused an immediate jump in yields. Financial markets are doing the dirty work.

Plans for new reviews make sense

A new chair calling for a review of existing practices is perfectly reasonable. The creation of five task forces to review Fed communications, the inflation framework, the balance sheet, data and methodology, and productivity and jobs makes sense. Those on the inflation framework and productivity merit special attention and may hold keys to Warsh’s hawkishness or lack thereof.

Conducting such reviews in six months, as planned, crams a lot of work into a compressed period. Any bureaucrat worth their salt knows that how task force mandates are framed and who is on them are key. Will the mandates and composition be neutral or biased?

On the inflation framework, two key questions may shape the rate outlook: what is price stability and how do you measure it?

Warsh has seemingly suggested the 2% on the left side of the price stability target is correct, but the zero behind the decimal point may be emblematic of the fallacy of false precision. If true, that leaves open whether the definition of price stability may extend to 2.49%.

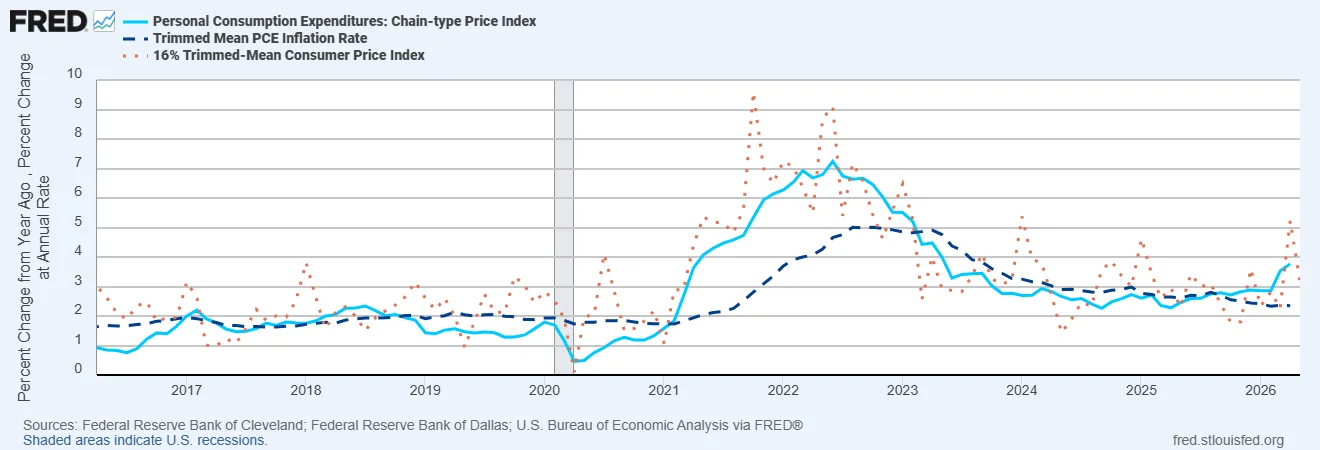

Then there is the debate over which inflation measure to use. Warsh has spoken about using trimmed mean measures. The Federal Reserve Bank of Dallas trimmed mean personal consumption expenditure measure now is under 2.5%, whereas PCE inflation is close to 4%. The Federal Reserve’s Bank of Cleveland’s trimmed consumer price index inflation is over 3%.

Figure 1. Which inflation measure should the Fed use?

Source: Federal Reserve Banks of Cleveland and Dallas, US Bureau of Economic Analysis

The relationship between trimmed mean and PCE inflation oscillates over time. Using trimmed mean PCE inflation now – in conjunction with a de facto slightly higher than 2.0% inflation target – could point to price stability being more readily achieved.

Regardless of whatever measure is used, changing horses in mid-stream before getting back, or at least on a clear path, to 2.0% PCE inflation might damage Fed credibility. And central banks still face the Herculean task of assessing the inflation outlook when trying to look to the medium term. But arguing that the Fed doesn’t hold much sway over supply shocks and downplaying possible second-round effects can support accommodation.

Productivity arguments are contested

Warsh has argued, with allusions to Alan Greenspan and the US’ 1990s experience, that artificial intelligence will boost productivity and growth without inflation, creating space for lower rates.

That view is contested. Greenspan refrained from raising them in view of productivity developments. In the short term, AI investments and activity are boosting demand more than supply, creating upward inflation pressure. Many economists argue higher productivity could boost the neutral rate. Technological improvements diffuse slowly into daily life.

In short, many are sceptical that an AI productivity revolution will have much near-term bearing on the inflation and rate outlook.

On balance, depending on how the task forces are staffed and their outcomes, inflation measures and productivity arguments could be used to suggest scope for lower rates, or not.

It is premature to conclude that Warsh is a hawk based on one press conference. He and the FOMC are navigating complex shoals between high inflation, supply shocks, geopolitics, fiscal messes, AI, changing economic dynamics and a president in search of lower yields. Time will tell if Warsh is a hawk, a chickenhawk or a dove.

Mark Sobel is US Chair of OMFIF.

Watch Mark’s June FOMC discussion with Claudia Sahm and Randy Quarles from 18 June.

Image credit: The White House

Interested in this topic? Subscribe to OMFIF’s newsletter for more.