A ‘grey swan’ is an outlier scenario which – though unlikely – has the potential to shape markets in meaningful ways if it happens. Here are five grey swans for the year ahead and their potential investment implications.

1. Artificial intelligence fails to scale

While AI-related equity valuations are very high, the argument is that the technology is still early in its monetisation curve and has the potential for real future growth in earnings across a broad range of sectors and geographies.

But what if AI fails to scale in the manner expected?

AI’s hunger for computational power has thus far proved insatiable, and scaling large language models or advanced generative systems requires a steady supply of high-performance semiconductor chips. Because production of these is largely concentrated in a few regions and dominated by relatively few companies, supply disruption could have far-reaching effects.

Training and deploying advanced AI models consumes massive amounts of energy, running the risk of demand spiking above grid capacity. If the energy grid cannot keep pace with data centre demand, a knock-on effect of rising energy prices and environmental concerns could trigger more localised public and political resistance. Higher energy prices would also erode tech margins while a halt to data centre construction could severely restrict AI progression.

As new AI use cases emerge, there is potential for a regulatory clampdown in response to unexpected negative effects. Efforts to relax regulations could unravel due to content moderation failures. An outcry over AI models that generate explicit content has already raised the spectre of a backlash that results in more rules and oversight.

2. China goes shopping

In a world beset by inter-country rivalry and heightened tensions, what if the largest exporting country abruptly became the world’s most voracious shopper – not just to fuel growth, but to cool global tempers? In this scenario, China jolts markets and policy-makers by unleashing a bold, demand-driven pivot: letting the renminbi rocket and, most crucially, turning decisively inward to revive domestic consumption.

This is more than economic engineering; it’s a calculated move to de-escalate mounting trade rifts with Europe and emerging markets after China’s trade surplus blew past $1tn in 2025. The imbalance is no longer about runaway exports – export growth barely outpaced gross domestic product – but about chronically weak household demand. In a remarkable pivot, Beijing acknowledges that the path to sustainable growth, and to restoring international goodwill, lies in empowering Chinese consumers and rebalancing towards internal demand.

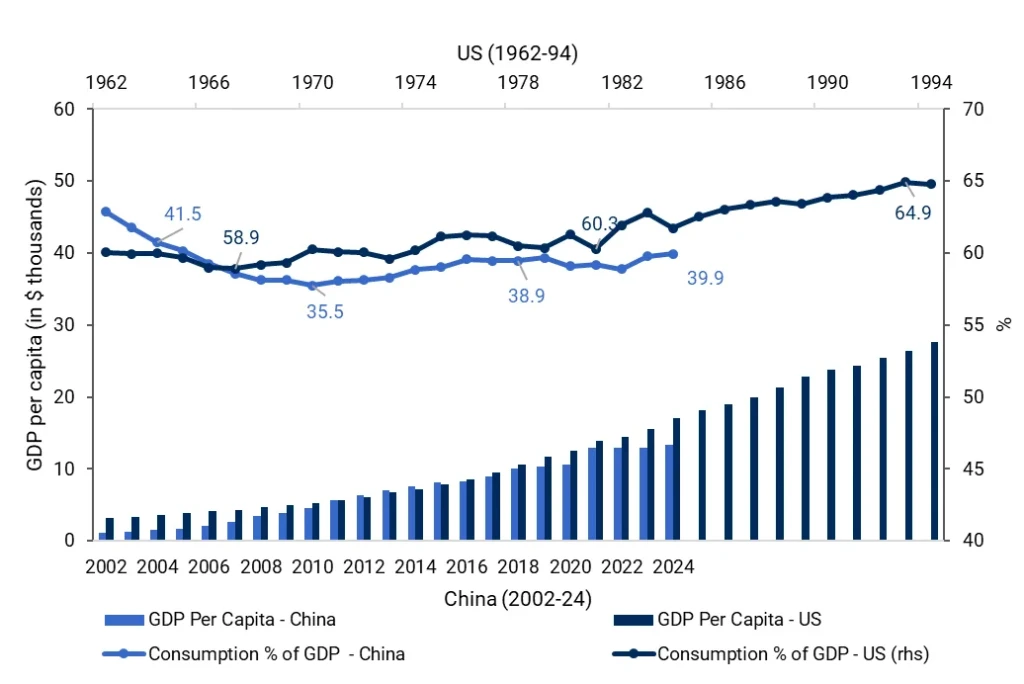

Using the US as a comparison, rising per capita GDP led to increased consumption as a share of GDP. As Figure 1 shows, China’s consumption remains low at 35%-40%. If China follows the US trajectory, rising incomes should drive a steady increase in consumption – unless it falls into the ‘middle income trap’. This inflection point strengthens the case for a consumption-led growth pivot.

The macro and market impact of this pivot would be significant. Supportive global conditions – accommodative monetary policy, fiscal stimulus and a fresh start into the inventory cycles – boost traditional industries and new sectors such as AI and renewables, driving earnings and fundamental growth in 2026. Renminbi currency strength and policy clarity attract foreign inflows into equities and bonds, lift sentiment across Asia, support regional currencies and underpin commodity demand.

Figure 1. China ready for consumption pivot

Source: Bloomberg Finance, State Street Investment Management as of 31 December 2025

3. Fortress North America

Last year’s 2 April tariff announcement was the defining economic and policy event of 2025. In this scenario, we posit that 2026 brings about a powerful reinvigoration of the US’s relationships with Mexico and Canada, with the US taking a leadership role in building a strong multi-dimensional alliance.

The first joint review of the US-Mexico-Canada trade agreement is due in mid-2026. Given the approach initially taken by the US – the first tariffs announced were not on China, but on Canada and Mexico – speculation has run high that the entire arrangement could simply collapse, that the US may perhaps withdraw just as it did with the Paris agreement or other organisations that it no longer sees as ‘serving America’s interests’.

Yet, we could imagine a future where the opposite occurs: 2026 ushers in a reconstruction phase that redefines North American trade and security architecture. Renegotiations lead to a far more integrated trade and economic framework that binds both Canada and Mexico much more closely to the US economic, energy and defence ecosystem.

While Canada and Mexico might need some convincing about entering into a new arrangement that at face value seems built purely on the requirements of the US, the implications would be radical. ‘Friendshoring’ becomes more than just a buzzword – it becomes the lynchpin of US-led regional industrial renaissance. A USMCA of this type results in a fundamental shift in supply chains and casts North America as the pre-eminent manufacturing and energy location that is largely insulated from geopolitical shocks that occur elsewhere.

4. Yen carry trade unwinds

A gradual progression towards policy normalisation in Japan is generally anticipated, but what would happen if that consensus expectation was quickly overtaken by events and there was a sharp unwind of the yen carry trade in 2026?

The seed of this grey swan took root with the surprise election of Prime Minister Sanae Takaichi in October. If her policy agenda accelerates fiscal expansion, technological investment and advances JGB yield curve normalisation to the extent that it marks a meaningful departure from decades of ultra-loose policy and introduces potential volatility into global capital flows, the ramifications could be significant.

A sharp yen depreciation combined with rising JGB yields could catalyse an unwind of the longstanding carry trade. Key drivers could include: aggressive fiscal stimulus (prompting fiscal dominance concern) and wage growth fuelling domestic demand; the Bank of Japan tightening beyond expectations; and political resolve to pursue yield curve normalisation, addressing persistent market distortions and amplifying volatility risks.

Initially, a weaker yen supports exporters and reflation, but as JGB yields climb, leveraged carry positions face narrowing returns and heightened volatility. Given the scale of yen-funded trades, forced deleveraging could ripple across FX, equities and bonds, creating systemic stress.

5. Sovereign warnings trigger bond shock

Public indebtedness has risen across most developed economies in recent decades, with a noticeable increase in sovereign debt servicing costs as interest rates normalised after the Covid-19 pandemic. The notorious bond vigilantes have been relatively well behaved to date, and our base case does not anticipate a change in that behaviour. But, what if 2026 sees the first episode of serious stress in government debt markets?

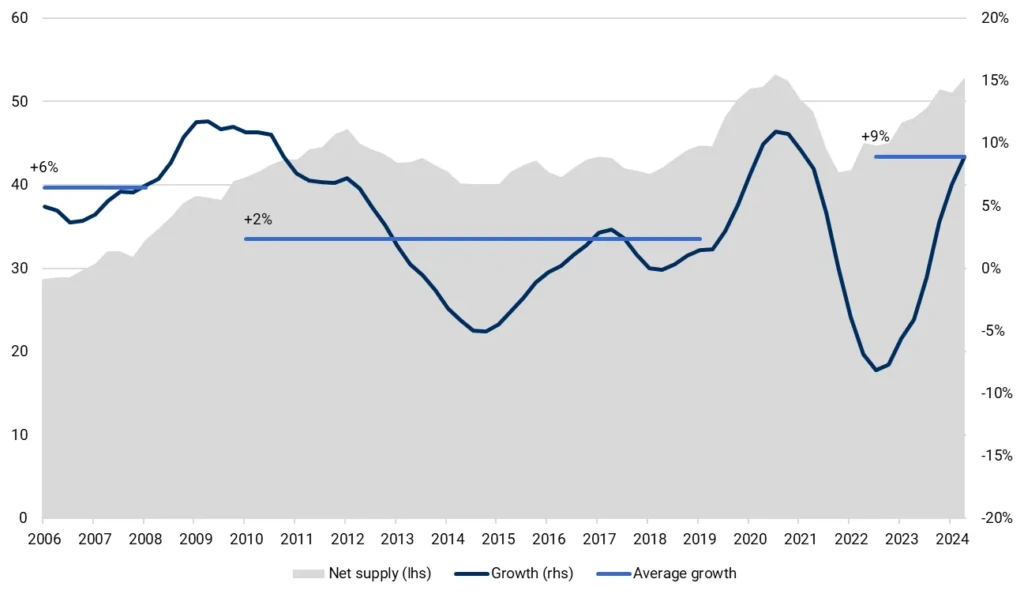

While there are material differences in sovereign debt sustainability among industrialised nations, the problem is global and systemic. Figure 2 shows our metric of the growth in the net supply of safe assets over the past two decades – i.e. the total bond issuance by highly rated governments minus the essential bond investment requirements of central bank reserve managers, global pension funds and commercial banks. This rapid growth is one of key reasons why long-term bond yields are rising for most developed economies.

Figure 2. Net global safe asset supply growth (2006-24)

$tn (lhs), year on year two-year m.a., % (rhs)

Source: Macrobond, SSIM Macro Policy as of 31 December 2025

In nominal terms, the majority of the growth is driven by consistently large deficits in the US, but this need not mean the first crisis will originate there. Global bond markets are facing increased supply in government debt, of which a growing share must be cleared at market rates. This opens up the possibility of sharp re-pricings at random auctions. Countries that are running comparable or larger primary deficits (budget deficit prior to interest payments) to the US, but have a much lower rate of nominal GDP growth, could be most vulnerable in the near term.

In this regard, yields on bonds at the very long end of non-US developed economies rose drastically in 2025, particularly in Japan, Germany, France and the UK. Of those, France appears the most likely candidate for a bond shock, as high deficits are not only mixed with low growth, but are complemented by a growing political crisis.

How might this scenario unfold? After the French government barely gets a budget through parliament in early 2026, the rest of the year then becomes characterised by increased political jockeying and gridlock. Before the year comes to a close, a rise in domestic tensions brings forward a divisive parliamentary and presidential election campaign. A fragmented electorate sees the market struggle to grasp what the future government composition might look like, bringing big swings in sentiment and an abrupt buyers’ strike for French government debt. The accompanying spike in French bond yields would be unlikely to remain a local story, rippling out to impact other European and developed sovereign bonds.

In Europe, this surprise rapid bear steepening of yield curves complicates monetary policy, leading to earlier rate cuts than expected, and stoking speculation that the European Central Bank may need to intervene directly and start buying bonds once again. The effects are also seen in currency markets, with a weakening euro driving other central banks to look seriously at easing as well.

Lori Heinel is Executive Vice President and Global Chief Investment Officer, State Street Investment Management.

This is an edited version of an article first published by SSIM.

With thanks to: Jennifer Bender, Global Chief Investment Strategist; Ninghui Liu, Head of Investment Strategy & Research, APAC; Simona Mocuta, Chief Economist; Aakash Doshi, Head of Gold Strategy; Masahiko Loo, Senior Fixed Income Strategist; Krishna Bhimavarapu, Economist; Elliot Hentov, Chief Macro Policy Strategist, SSIM.

Join OMFIF and SSIM on 14 May for Policy shifts and market risks: what public investors need to know.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.