Anyone watching coverage of the 2026 Hungarian parliamentary election would be hard-pressed to believe that in 1989 Viktor Orbán launched himself into the centre of Hungarian politics with an anti-Russia, pro-liberal democracy speech. His gift for oration has remained even as his allegiances have reversed, helping him win four consecutive elections from 2010 to 2022.

However, political support for Orbán and his Fidesz party has dwindled in the last few years, and this year’s election saw the end of Orbán’s rule with challenger Péter Magyar and his Tisza party winning 138 out of 199 seats in parliament. This outcome has stark implications for Hungary’s economic trajectory and financial future, as Magyar seeks to dismantle an institutional apparatus that has been 16 years in the making.

The past: Orbánomics and illiberal democracy

The European Union’s longest serving head of state has written the playbook for populist leaders worldwide. He has been backed by US President Donald Trump, who sent his vice-president JD Vance to campaign for him in 2026, and Russia’s Vladimir Putin, to whom he has remained a key ally in the EU: blocking sanctions and aid to Ukraine. Orbán is a vocal proponent of ‘illiberal democracy’, which has manifested in a state-controlled media, limited judicial independence and crony capitalism. As a result, the EU blocked funds to the country in 2022.

The loss of EU funds accelerated the decline of the Hungarian economy that occurred after the Covid-19 pandemic and Russia’s invasion of Ukraine. Despite initially seeing gains in employment, economic growth and a reduction in the deficit, Orbán’s unorthodox economic strategy, dubbed ‘Orbánomics’, ultimately failed to lay the structural groundwork for a resilient economy, relying on state intervention in the market and privileging elite businessmen loyal to the regime, while neglecting investment in human capital and creating necessary conditions for competition and innovation.

Orbán’s dual industrial strategy aimed to reduce foreign dominance in key sectors while increasing foreign investment in manufacturing to promote exports. Subsidies favoured domestic firms in politically sensitive industries – such as media, banking and retail – while low corporate taxes attracted lucrative manufacturing deals with German automotive companies and Chinese electric vehicle and battery producers.

These low taxes were financed by increases in VAT and sector-specific windfall taxes on banks and foreign-owned companies, which have ultimately distorted market signals and harmed the investment environment. High election cycle spending and expansionary fiscal policy have increased budget deficits to a projected 5.6% of gross domestic product in 2026 and contributed to stubborn inflation. Persistent deficits have also made it difficult for Hungary to consolidate its debt. In December 2025, Fitch Ratings affirmed Hungary’s BBB rating but cut its outlook to ‘negative’, citing concerns over fiscal loosening in the wake of the 2026 election and the lack of a consolidation plan.

The future: Péter the Hungarian

Péter Magyar will have his work cut out for him restoring Hungary to a democratic, market-orientated state free of entrenched interests. Luckily for him, two things are working in his favour. The first is a supermajority in parliament that will allow him to alter the constitution and cement change at an institutional level. The second is his commitment to unlock €17bn in EU funding that will allow him to implement Tisza’s economic programme.

Tisza’s programme involves addressing the failures of Orbánomics and dismantling the institutional scaffolding that upheld it. His goal is for a ‘knowledge-based, competitive economy with strong domestic added value’ to bolster Hungary’s lacklustre economic growth and productivity. He plans to use EU funds for much-needed investment in education and healthcare. He plans to overhaul the public procurement system to eliminate corruption. Importantly, he plans to move away from the ‘giga-assembly’ model that has Hungarian workers working at low-value added segments and move up the value chain. He has surrounded himself with people that have global business and financial experience to make it all happen, such as István Kapitány, former global executive vice president of Shell.

While his plans sound sensible on paper and could put Hungary on a long-term path for a stronger economic growth rate and financial position, structural transformation will not take place overnight. Further, EU funds will not be unlocked immediately and are conditional on Hungary committing to rule-of-law reforms.

Figure 1. Forint rallies, reaching highest point since February 2022

Forint to euro exchange rate, as of 13 April 2026

Source: XE

Magyar can free up funding in other ways by getting rid of the subsidies for Orbán-era business elites. His pledge for a simple, more predictable tax system with fewer windfall taxes will contribute to a more attractive investment environment. Magyar has also pledged adoption of the euro. This is another plan that is likely to take longer than a four-year electoral term, but it will set Hungary on a policy path that will improve its financial standing in an attempt to meet the Maastricht criteria, including such measures as: reducing the budget deficit to below 3%, reducing the public debt-to-GDP ratio (debt was 74.6% of GDP in 2025), reducing inflation and interest rates, and ensuring exchange rate stability.

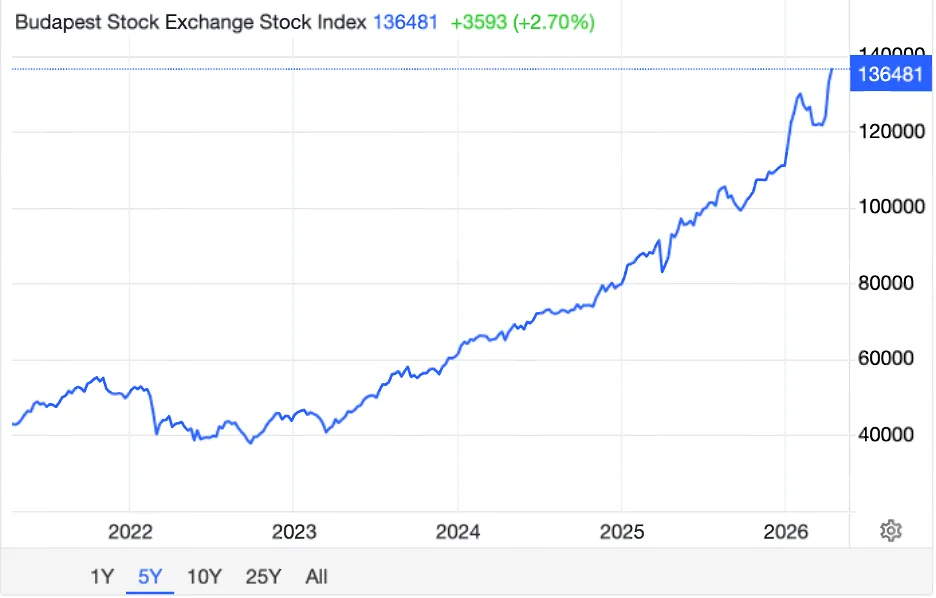

Financial markets have reacted with optimistic anticipation for Magyar’s reforms. Hungarian bonds, stocks and currency ‘pushed to the brink of multi-year highs’ days before the election took place (Figure 1). Meanwhile, the Budapest stock index (BUX) reached a record high of more than 136,000 points the day after the election, demonstrating a reduction of Hungary’s policy risk premium (Figure 2).

Figure 2. BUX reaches record highs day after election

Budapest Stock Exchange Index as of 13 April 2026

Source: Trading Economics

Despite the strong pro-European stance that inspired investor confidence and cemented his victory, Magyar’s election cannot be seen as a hard-Western ideological pivot for Hungary. He has been careful not to present himself as a liberal, focusing on the economy and deteriorating public services in his campaign, a pragmatic move that has helped him win over past Orbán voters. His conservative-Right party are maintaining the pro-family position of the Orbán government, pledging family allowances and maternity benefits.

Magyar, which literally means ‘Hungarian’, also espouses nationalist stances that are clear from his economic and foreign policy programme, such as prohibiting the mass employment of guest workers and rejecting immigration quotas. Ever the pragmatist, he plans to keep using Russian oil, at least until Hungary can reduce its dependence.

However, he is expected to unblock a €90bn euro EU loan to Ukraine, which Orbán had previously prevented. In this way, Magyar has carefully played the game both at home and abroad: making it clear that Hungary wants to orientate itself towards Europe and away from Russia, but not sacrificing domestic interests for his relationship with Brussels. Nevertheless, after 16 years of Orbán’s loud belittlement of Europe and liberal principles, Magyar is a breath of fresh air and evidently a propitious bet for global investors.

Mariam Khan is an Economist at OMFIF.

Join OMFIF on 20 April to examine how to unlock Europe’s capital potential.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.