French President Emmanuel Macron: ‘Addressing global economic imbalances is our key priority… the objective of this G7 will be to build this framework of co-operation in order to fix the roots of these imbalances.’

US Treasury Secretary Scott Bessent: ‘We will execute on the President’s agenda for the G20 by prioritizing pro-growth economic policies though… strengthening our understanding of excessive global imbalances.’

Global imbalances emerged as a hot topic before and after the 2008 financial crisis when wide gaps between surplus and deficit economies were seen as an important macroeconomic backdrop to the crisis.

They persist today. As Macron observed at the World Economic Forum in Davos, these excessive imbalances arise from ‘American overconsumption, Chinese underconsumption and overinvestment, and European underinvestment and lack of competitiveness.’

Remarkably, Macron’s assessment, verbatim, would have been spot on 20 years ago.

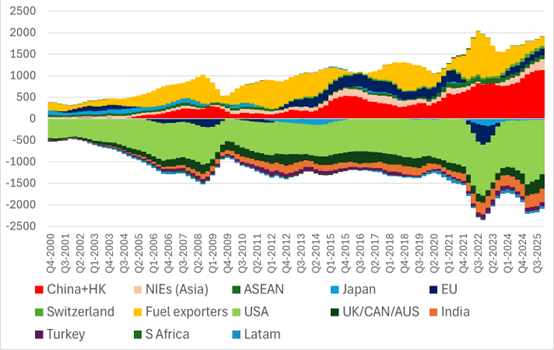

Figure 1. Global goods trade balance for select large economies

$bn, trailing 4q sums

Source: Brad Setser

Don’t confuse commotion for motion

The G7, G20 and International Monetary Fund have not ignored global imbalances over the last two decades. Early on, the G20 set up a Framework Working Group and a Mutual Assessment Process to root out imbalances. The IMF began producing an annual ‘External Sector Report’. Much ink and verbiage were spilled.

For the 2026 imbalances discussion, the French government has set up an independent academic expert group led by Hélène Rey and including other prominent outstanding economists. The US created a G20 study group, chaired by Australia and Korea.

In 2026, can Macron or Bessent succeed where others have flailed for two decades? That is highly unlikely. It is useful for leaders to discuss their economies, but the prospects for finding the political will for concrete G7 and G20 commitments and success in curbing global imbalances are dim.

The roots of the problem

Let’s return to Macron’s diagnosis of imbalances.

The US deficit: The flipside of US overconsumption is low national saving, significantly associated with longstanding massive fiscal deficits. Estimates now point to unsustainable average annual deficits of 6% of gross domestic product over the next decade. These deficits appear locked in. America’s political class lacks the guts to tackle them, blithely waiting for a financial crisis before finding the wherewithal to do something.

President Donald Trump’s Big (not so) Beautiful Bill aggravated America’s deficit problem, and forthcoming refunds on Trump’s misguided tariff policies could exacerbate the red ink. Meanwhile, the administration risibly and fantastically suggests surging growth and productivity will cut the deficit to a more sustainable 3% of GDP, countering global imbalances.

China’s surpluses are also locked in. The economy faces deflation or lowflation, a housing collapse, excess leverage, low confidence and depressed domestic demand, among other issues. Meanwhile, the government funnels finance to state-owned enterprises, which maintain production that cannot be absorbed domestically. That spawns manufacture exports, underpinning a massive current account surplus of some 3% to 5% of GDP, aided by a highly undervalued currency.

Chinese and other economists have urged the government to increase fiscal support for consumption, services and the social safety net in lieu of investment and to deploy more aggressive monetary policy accommodation. Yet, the leadership consciously has avoided doing so, fearing such policies could unleash other problems.

Europe’s surpluses have reflected in large part Germany’s strong saving. Germany’s decision to boost defence and infrastructure spending and reform the debt brake should help lower surpluses in the years ahead. But European exports may be swamped by China’s external prowess.

Moreover, is there any reason to think Europe may implement capital markets union, pursue significant joint Eurobond issuance and carry out the recommendations made in the 2024 report by Mario Draghi, former European Central Bank president? Is there any reason to think that France, facing severe fiscal constraints, will be able to implement growth-orientated reforms? Can Giorgia Meloni escape Italy’s fiscal and low productivity constraints?

Grounds for scepticism run deeper

Countries rarely ‘coordinate’ macroeconomic policies. Perhaps they can find the will in times of crisis. Other times, facing synchronic impulses, they may act in a common direction. But ultimately, countries respond to their own domestic political and cyclical circumstances.

President Xi Jinping faces numerous domestic constituencies. China needs its export might to meet excessively high growth targets and is unlikely to allow its currency to appreciate enough to upset strong external competitiveness.

No president of the US can make credible fiscal commitments, even if sensible, without Congressional support, and surely wouldn’t want to be seen as pursuing restraint in response to foreign-led exercises. The Federal Reserve will independently set its interest rates in line with its dual mandate. And few in the G7, let alone the G20, are willing to trust the Trump administration.

The US may see global imbalances as a vehicle to complain about Chinese surpluses while ignoring its own fiscal disorder, but Trump has shown little desire to upset the tense détente with China since the Busan Summit in October 2025.

Macron is nearing the end of his tenure. His domestic standing is weak. France is a ‘middle power’, unlikely to pin down the US and China, let alone Germany, on concrete commitments. Further, China isn’t even a G7 member.

In 2026, expect many academic papers, scenarios and rhetoric on global imbalances, highlighting what we already know. But the US and China, and many in Europe, are unlikely to budge on their policies that cause excessive global imbalances any more than they have over the last two decades.

Beyond the grandeur of lofty rhetoric, don’t expect much to happen. To use an American idiom, this is a ‘nothingburger’.

Mark Sobel is Vice Chair and Chief Economist at OMFIF.

Image Credit: Fiesp Ciesp Ses

Image Credit: Fiesp Ciesp Ses

Interested in this topic? Subscribe to OMFIF’s newsletter for more.