President Donald Trump declared his summit with Xi Jinping a ‘12’ on a scale of one to 10, while fawning over Xi as a great leader. Xi seemed far more reticent and stoic.

The summit presented a hefty set of welcome and pragmatic deliverables. They may helpfully turn down the temperature a tad for the time being in a frosty relationship. However, it is a limited deal, reminiscent of the unfulfilled Trump 1.0 Phase One deal.

More significant is what wasn’t addressed – fundamental economic structural flaws that impact the US-China relationship and will drive continued stresses for years to come, even apart from geopolitical tensions such as Taiwan, the South China Sea and Ukraine.

Structural imbalances and growth models

Only recently, China’s Fourth Plenum met, previewing the upcoming 2026-30 five-year plan. That preview was largely a ‘steady as she goes’ reaffirmation of the current broken growth model.

On the macroeconomic front, there is recognition of the need to boost consumption and domestic demand. But the general orientation of underlying policies appears aimed at gradualism, rather than a more immediate fundamental change. That is especially true on the fiscal front. The state will thus retain a heavy visible hand in driving investment-led growth. Housing woes, weak labour markets and high leverage should thus remain key features of the Chinese economy.

From an external standpoint, China’s weak domestic demand and robust production mean continued excess capacity and a flood of Chinese exports onto global markets, including manufacturing exports which now equal more than 10% of Chinese gross domestic product. With high US tariffs closing off many Chinese exports, Europe should be wary.

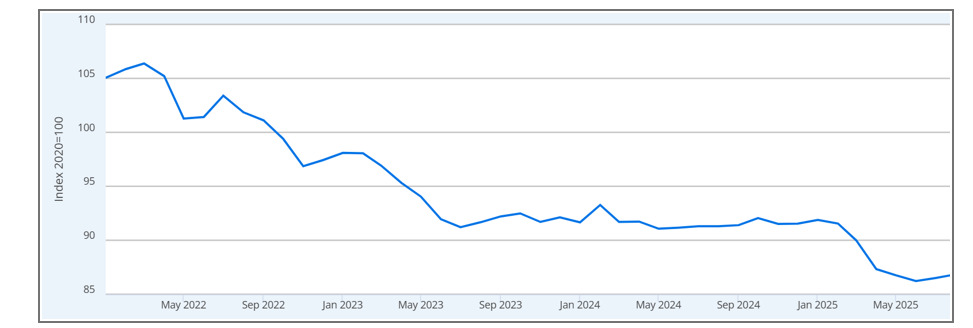

China’s massive external surpluses are being undergirded by an extremely weak and undervalued Chinese yuan. The real renminbi has fallen by over 15% since early 2022.

Figure 1. Weaker renminbi underpins China’s rising trade surpluses

Real broad effective exchange rate for China

Source: Bank for International Settlements via FRED

The International Monetary Fund now estimates that China will record more than 3% of GDP current account surplus in 2025 and the trade surplus should at least be 5%. However, using customs-based trade measures and making reasonable adjustments for perhaps faulty income data, the trade and current account surpluses are substantially higher. Even if exports to the US are sharply down, transshipments – especially via southeast Asia – have dramatically risen.

In part, China has become a less attractive source for capital inflows since the pandemic and the start of the Russia-Ukraine war. But apart from capital account developments, China has sought to keep the renminbi broadly stable against the dollar – on the down and upside – which means that it gained further competitiveness against other countries after the dollar fell in the wake of Liberation Day.

Of course, the main global counterpart to China’s huge external surpluses is the massive US current account deficit. That may in part be influenced by foreign excess savings and external practices. But first and foremost, it reflects America’s love of consumption, unsustainable gigantic fiscal deficits and associated low US national saving. The administration may tout that its policies will lower budget deficits from roughly 6% to 3% of GDP, but those prognostications must be taken with a huge grain of salt if not suspension of belief.

Technological competition and fragmentation

The summit’s deliberations on rare earths, chips and export controls underline that China and the US are in a sustained technological competition. The Plenum and Xi’s statements make clear that for China an immediate priority is a focus on artificial intelligence and technological advancement, while reducing possible dependence on the US. Americans are prone to disregard China’s technological dynamism, innovativeness and capacity for advancement.

In short, the Trump-Xi discussions and deal do not change the underlying dynamic in US-China relations. Decoupling, fragmentation and derisking of the global economic and trading systems is rising. Though the US and China need each other and global interdependencies run deep, more splintering is coming.

More dialogue needed

US Secretary of the Treasury Scott Bessent’s periodic meetings with Chinese interlocutors have been productive in limiting fallout, but neither a handyman fix-it approach nor a reliance on episodic Xi-Trump meetings are a sufficient answer. The Trump/Xi discussions highlight anew that the US and China – over 40% of the world’s GDP – need to better manage economic and financial stresses.

There are ample bilateral past formats, even amid frictions, to offer examples on improving understanding and discussion, such as the US-China Joint Economic Committee and Economic and Financial Working Groups, but these are hardly panaceas.

US-China discord is here to stay. Nonetheless, for their own self-interest, let alone the world’s, the US and China need to limit downside risks even when they disagree, avoid gratuitous tit-for-tat actions, find ways to speak to one another more comprehensively and technically and not just at senior political levels, and foster greater understanding of each other’s perspectives.

Mark Sobel is US Chair at OMFIF.

Join OMFIF on 9 December to examine The future of public money.

Image Source: The White House

Interested in this topic? Subscribe to OMFIF’s newsletter for more.