Given the scale of funding that Ukraine requires, the activation of frozen Russian reserves has effectively become the only viable option to sustain funding as Russia’s war is set to drag into its fifth year.

At the European Council’s meeting in October, the European Union refrained from committing to a proposed plan for ‘reparations’ loans for Ukraine using seized Russian reserves, largely due to objections from Belgium. Now, reworking the proposal or agreeing around an alternative financing vehicle for Ukraine is top of the agenda at a high-stakes EU summit in December.

The reality is that the West does not have the resources to bankroll an indefinite war. Instead, fatigue has risen – notably in the US – for continuing to finance Ukraine. There is less capacity to deliver on loans and grants when many western governments face mounting political and budgetary pressures themselves.

Ukraine’s creditors originally assumed the war would be over by this stage. The International Monetary Fund funding programme for Ukraine originally imagined the conflict would have wound down by the end of 2024. Remember too that €321bn of funds have already been allocated to Ukraine by global governments since 2022.

Additional foreign financing needed

With instead no clear end to the war in sight, the IMF estimates additional foreign financing of $65bn will be needed by the end of 2027. On top of this, another $60bn is required for military assistance. Still, Ukraine is likely to be running budget deficits of nearly 20% of gross domestic product a year for longer.

All told, Ukraine must secure around $50bn a year from its allies. One estimate points to more than $200bn being needed to sustain defence and financial requirements by the end of this decade.

However, many of Ukraine’s key backers – such as Germany, France, Poland, the UK and the US – all face increasing government debt, particularly those governments increasing defence spending to 3.5% of GDP by 2035 to meet their Nato commitments.

Ukraine can no longer rely on the US to deliver any sustained financing. This places a growing burden on the EU – already Ukraine’s single largest financier – to assume a greater share of the costs. However, there’s a risk of voter backlash within the EU if Ukraine’s military funding comes at the expense of domestic expenditure.

Belgium holds up EU agreement on Russian assets

If the only realistic resource at this stage is Russian assets, the challenge lies in mobilising them without exposing the EU or individual member states to undue financial risks – a primary concern for Belgium.

Belgium has insisted that it alone will not be held liable for the risks associated with the proposed lending programme, given that around €180bn of the money is held in Belgium. The country seeks the ‘full mutualisation of the risk’ if Moscow should make claims on the assets; legally binding guarantees that EU member states would contribute if the money must be repaid; and for all EU member states holding frozen assets to jointly act. Beyond Brussels, another €25bn of the assets are frozen across several other EU capitals.

For now, the European Commission and Belgium are working on reconciling each other’s positions. If it becomes possible to eliminate the sources of Belgium’s concerns, the Commission would officially propose a bill within a few weeks. Slovak Prime Minister Robert Fico, an advocate of Russia-friendly foreign policy, has stated his opposition to the plan. Separately, Norway is considering guaranteeing a part of the programme via the sovereign fund.

Ukraine’s funding situation will only become more challenging from around the end of the first quarter next year. For the reparations loan programme to work, an agreement must be achieved near term. This would provide the necessary time to work out a mechanism releasing the money by the second quarter of next year. Securing further IMF financing supporting Ukraine also hinges around whether the EU can finalise its plans. An agreement is required soon.

Growing consensus on EU plan to use Russian assets

The proposal of using frozen Russian assets to fund Ukraine is controversial. There is a legitimate concern about the further activation of Russian reserves including questions around sovereign immunity, reserve currency statuses and the risk of Russian reprisal such as the seizure of foreign assets.

Against such a backdrop, the European Commission’s proposition is innovative. Rather than directly confiscating the frozen reserves, which could undermine confidence in the financial system and the euro, the Commission has designed a legally intricate mechanism channelling the funding through the proposed structure seeking to minimise reputational risks and avoid legal challenges.

Under the Commission’s plan, around €140bn of available cash generated by the frozen Russian assets would be repackaged as zero-interest credits. Such loans would be conditional on reforms and repayable only if Russia ceases the war and compensates Ukraine for the damages.

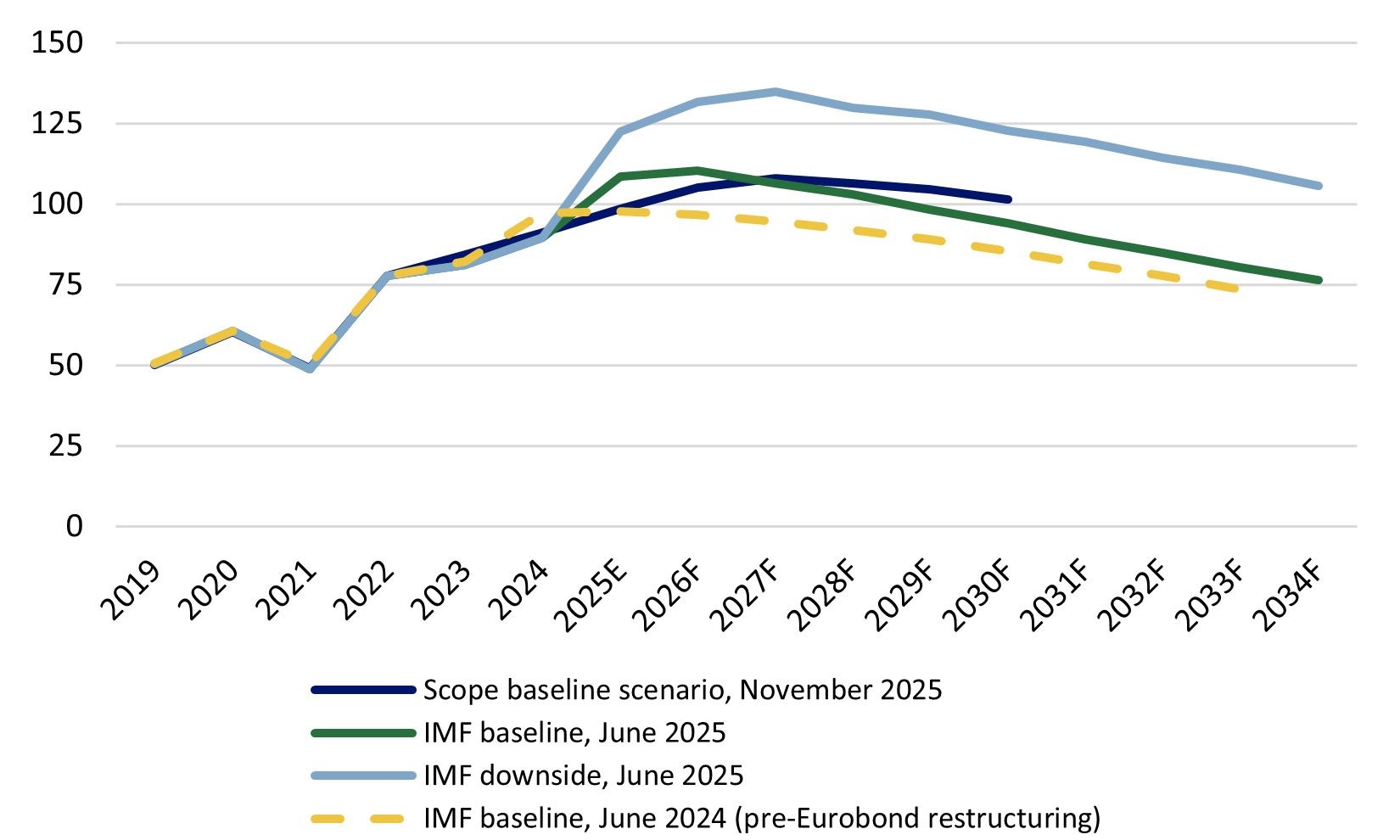

Given that Russia is highly unlikely to ever pay Ukraine for damages unless the former suffers a decisive defeat, the zero-coupon loans to Ukraine might serve effectively as grants – minimising adverse effects for Ukraine’s public finances (Figure 1).

Figure 1. Ukraine’s public and publicly guaranteed debt

% of GDP

Source: IMF, Scope Ratings

Note: Scope Ratings and IMF projections are for the public and publicly guaranteed debt stock of Ukraine including the Extraordinary Revenue Acceleration loans. June-2024 IMF projections were made before the August-2024 Eurobond debt restructuring.

Strain on stretched EU finances

A potential downside of the plan is that guarantees from willing governments would act as a contingent liability, lifting the implicit liabilities of the participating countries. Nevertheless, given the significant funds Ukraine requires from allies, if not by using the Russian assets, the EU would need to fund Ukraine through an alternative vehicle that would potentially place even more strain on already stretched national budgets.

An alternative such as joint EU debt or bilateral loans might require near-term debt-servicing costs, which the reparations loans would not; as well as a future repayment schedule, which a reparations loan programme probably also would not.

Dennis Shen is Chair of the Macro Economic Council and Lead Global Economist of Scope Group.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.