France and the UK are struggling with excessive national debt and political disaffection. But one is forced to make a virtue of necessity, while the other is tempted into inaction. Charles Dickens would have recognised the irony: the nation that praises freedom is shackled by its debts; the nation that suffers from market constraints could be renewed precisely because of them. The European Economic and Monetary Union protects France from the global financial market, while Britain stands alone. With this protection, the pressure to adapt is much less on France than on the UK, which is likely to prove a serious disadvantage for France.

Debt upon debt…

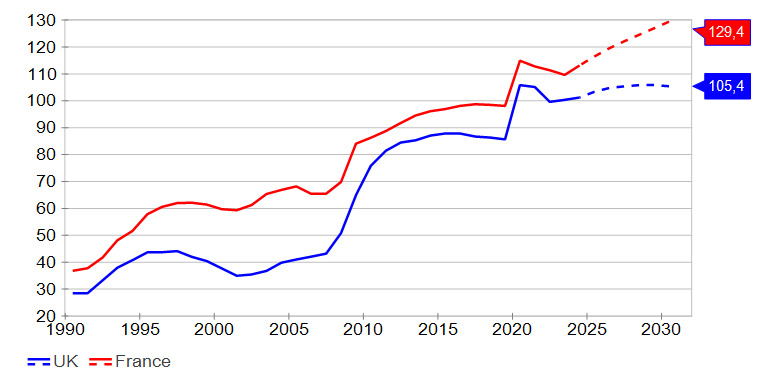

Both governments have run up high levels of debt, with France increasing its public debt ratio by 30% of gross domestic product since 2010 to an estimated 116.5% in 2025 and the UK increasing it by 27.5% of GDP to 103.4% (Figure 1). The International Monetary Fund expects debt in France to continue to rise sharply until 2030, while it will remain at a high level in the UK.

Figure 1. Public debt ratios rise sharply

Gross government debt in % of GDP

Source: Macrobond

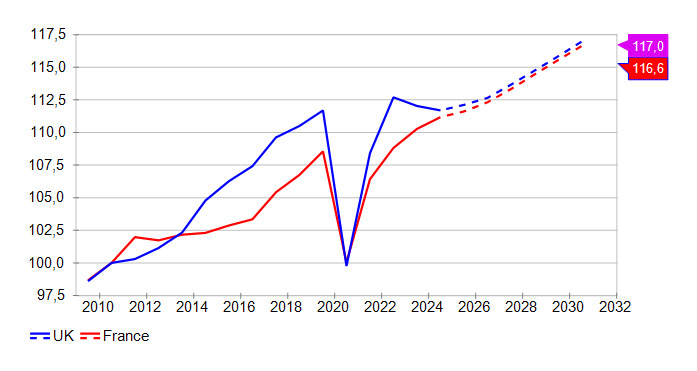

Average annual productivity growth measured as real GDP per capita was modest in both countries between 2010 and 2025 – 0.7% in France and (despite Brexit in 2016) 0.8% in the UK. The IMF expects GDP per capita in both countries to continue to develop almost in parallel (at a combined rate of 0.9%) until 2032 (Figure 2).

Figure 2. Stagnant productivity stays on a parallel path

Real GDP per capita (at purchasing power parity) 2010 = 100

Source: Macrobond, IMF

Thanks to population growth, real GDP in France rose by 1.1% per year between 2010 and 2025, and in the UK by as much as 1.5%. The IMF anticipates lower population growth over the next five years. In France, real GDP is expected to grow by 0.8% per year, barely exceeding GDP per capita growth. In contrast, the IMF forecast predicts higher growth of 1.2% per year for the UK.

Politics in transition

At first glance, the political situation in each country appears very different. Political deadlock in France is leading to instability and a loss of control over public finances. Prime Minister Sébastien Lecornu’s government lacks a stable majority in parliament and is struggling to remain in office after narrowly surviving a vote of no confidence by promising to water down pension reforms. The government is simultaneously struggling with budget consolidation, which is making little progress due to concessions to defenders of the country’s extremely generous social benefits.

On the other hand, UK Prime Minister Keir Starmer governs with a clear majority. However, his Labour party does not stand united behind him. Public finances are under pressure because the government is finding it difficult to curb social spending. Fearing that tax increases could completely stifle already weak growth, the government has resorted to more debt.

The political deadlock in France and the timidity of the UK government are grist to the mill for protest parties. According to an Opinium poll conducted in October, Reform UK, the right-wing populist party of Nigel Farage, stands at 32%, Labour at 22% and the Conservative party at 18%. The Liberal Democrats (11%) and the Green party (10%) have little support. Under the first-past-the-post voting system, Reform currently has a good chance of forming the next government. Whether this would lead to more solid public finances is questionable as Reform wants major tax cuts for citizens and businesses, but it remains unclear how these measures would be financed.

In France, an October 2025 poll by the Ifop institute found that around 35% of voters would vote for the Rassemblement National. This makes Marine Le Pen’s party the strongest political force today. Like Reform UK, the RN is promising extensive tax cuts, but remains vague about how they will be financed. Its opposition to the austerity plans of Emmanuel Macron’s Renaissance party minority government does not bode well for public finances should the RN actually come to power.

Populist parties benefit from grievances. The longer the solution to the problems is delayed, the stronger they become. Once in power, they worsen the situation instead of improving it. As a study by economists Manuel Funke, Moritz Schularick and Christoph Trebesch shows, real GDP per capita falls by 15% compared to a reference path over 15 years when left-wing populists are in power, and by 10% when right-wing populists have gained power.

Where are the ‘bond vigilantes’?

Interest rates in the UK are significantly higher than in France, at around 4.4% for 10-year government bonds compared to just 3.4%. The exchange rate of sterling against the euro has fallen by almost 6% in the course of this year, resulting in inflation rising to 3.8% in September.

Although the UK has a slightly weaker external current account balance than France, this is unlikely to be enough to explain the interest rate differential and the depreciation of the pound. It is more likely that France can hide behind the EMU, while the UK has to fear pressure from the financial markets through the ‘bond vigilantes’. More solid public finances in other euro area countries are keeping interest rates low and the euro stable for France.

However, the ‘bond vigilantes’ often ensure a return to sound fiscal policy. Former British Prime Minister Liz Truss experienced this in October 2022, when her deficit-increasing tax cut plans triggered a financial crisis that forced her to resign after only 49 days in office. The socialist experiment of French President François Mitterrand in the early 1980s also failed due to resistance from the financial markets, which forced an economic policy U-turn with currency crises and interest rate hikes of up to 17%. This experience of political powerlessness in the face of the ‘bond vigilantes’ might have motivated Mitterrand years later to wrest monetary union from Germany.

At present, it seems that France wants to take its time in reining in its out-of-control fiscal policy, while the government in London is struggling to find solutions – hence the expectation that the primary balance of the UK’s national budget will turn from the current deficit into a surplus by 2030, while in France it will remain alarmingly high, according to the IMF’s forecast.

Déjà vu?

Before the EMU, no monetary union of sovereign states had ever survived in history. They either failed or were absorbed into national currencies. The history of the Latin Monetary Union is likely to be of particular interest to the EMU. Founded on France’s initiative in 1865, the participating states failed to muster the necessary fiscal discipline to protect the currency from the monetary financing of individual states’ budget deficits. Prominent offenders were Italy and Greece. Ultimately, the LMU failed due to the financing of the first world war, which many states were only able to cope with by creating large amounts of unbacked paper money.

Today, financial support for Ukraine – coupled with the need to significantly increase countries’ own defence budgets, and the unwillingness to cut back on the bloated welfare state – is leading to similar financial stress. For now, the alliance with Germany in the monetary union is still protecting the highly indebted states from the ‘bond vigilantes’.

However, with the German government under Chancellor Friedrich Merz set to take on enormous new debt, this protection is likely to be lost. Like France, Germany is failing to adapt public spending to the radically changed requirements of our time and is resorting to excessive borrowing. As a result, the euro will lose the fiscal anchor that Germany has provided up to now.

At first glance, the present day does not seem to have much in common with the Britain and France that Dickens knew. But on closer inspection, a similarity can be seen: France is in political deadlock and facing national bankruptcy. The structures are so entrenched and the pressure to adapt from the financial markets is not great enough thanks to monetary union that an orderly solution to the problems is possible. Ultimately, a disorderly, chaotic resolution of the problems is likely, which could cause considerable collateral damage not only to monetary union but also to the European Union as a whole.

Although the UK also faces major challenges, politicians still have room for manoeuvre. The financial markets are generating the necessary pressure to act. As a result, the outlook for the UK is much more favourable than that for France.

Thomas Mayer is Founding Director of the Institute and former Chief Economist of the Deutsche Bank Group and Head of Deutsche Bank Research.

This is an edited version of an article previously published by the Flossbach von Storch Research Institute.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.