After the September Federal Reserve rate cut, investors anticipate further rapid and decisive monetary easing. However, the data give reason to doubt whether a series of rate cuts is – or indeed should be – in the cards.

The latest meeting of the Federal Open Market Committee was one of the most consequential in recent times, with a wide diversity of views and shrouded in political intrigue, anathema to the Fed’s technical ethos. After the widely expected quarter-point rate cut, all eyes are now focused on the path ahead.

Investors expecting the Fed to quickly cut the federal funds rate to around 3% by mid-2026 (from the current 4% to 4.25%) are getting ahead of themselves. The median dot plot – ignoring the sadly droll projection by Stephen Miran, the Donald Trump-appointed chair of the Council of Economic Advisors and member of the Fed board of governors – points to barely two more cuts this year, limited reductions next year and a move to 3% only in the long run.

Moreover, deeper reflection on the data gives reason to doubt that a series of cuts is or should be in store for the coming nine months. Economic uncertainty is high, as reflected in the wide dispersion of views within the FOMC. But we suspect the Fed may be overestimating downside risks to the near-term growth outlook, while underappreciating upside risks.

We also suspect that its longer-term view might simply not add up. The Fed could ease policy more aggressively if it decided to bend to political pressure, but based on this latest FOMC meeting, we do not see this as likely. Miran was isolated in his dovish dissent, with Christopher Waller and Michelle Bowman – also Trump appointees to the Fed board of governors – siding with the majority.

Inflation leg of mandate

The FOMC pencilled in that personal consumption expenditures inflation will fall to 2% by 2027. Assuming reversion to target is standard operating procedure, but the inflation target has been overshot for five consecutive years. The dot plot projects PCE inflation this year of 3%, and marked up next year’s from 2.4% to 2.6%. Numerous short- and longer-term forces pose upside risks to inflation: tariffs – which might be more impactful than a one-time hit to the price level – dollar depreciation, decreased labour supply due to immigration policy, ageing demographics, geopolitical fragmentation and fiscal dominance, which could exert pressure for financial repression.

Notwithstanding the Fed underscoring the sanctity of the 2% target, is the US creeping towards a 3% inflation regime?

The maximum employment leg

The FOMC framed the rate cut as risk management to guard against a spike in unemployment.

To be sure, signs of labour market softness abound. The unemployment rate inched up from 4.2% to 4.3% and the dot plot projects 4.5% by end-2025; job openings and quittings are down; unemployment claims up. Broader measures capturing underemployment and marginal attachment to the work force are edging up. Recent job revisions data caused deep public concern, even if broadly in line with analyst expectations.

But even at 4.5%, unemployment would be considered broadly in line with the non-accelerating inflation rate of unemployment. And slower growth in the labour supply due to the administration’s crackdown on immigration implies a much lower monthly pace of job creation is needed to keep the labour market in equilibrium, perhaps as low as 50,000 rather than 150,000.

Moreover, the growth outlook has improved. Entering 2025, US growth forecasts were above 2%. They were quickly marked down after the 2 April Liberation Day, pointing to a second-half recession or flat growth. Now they have been raised again, and the dot plot marked up 2026 growth as well – though still shy of 2%. Fiscal policy remains supportive.

Is monetary policy restrictive?

The Fed argues that monetary policy is restrictive, largely because the FFR has been well above its longer-run neutral rate – 3% per the dot plot.

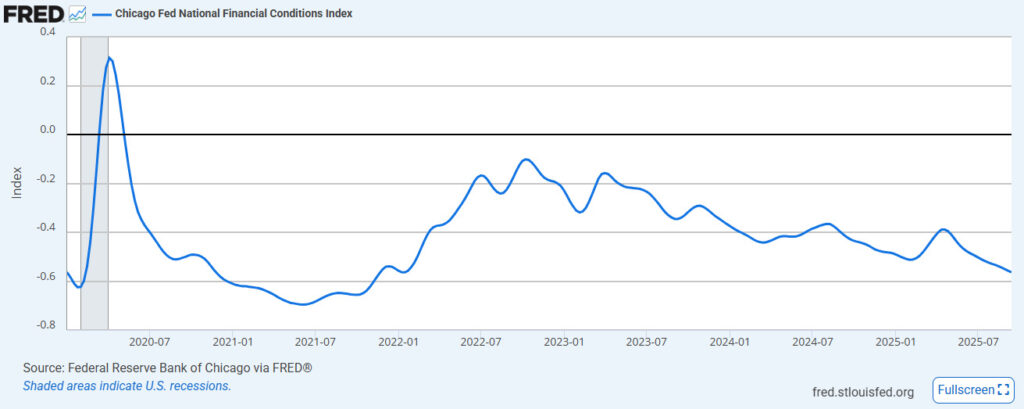

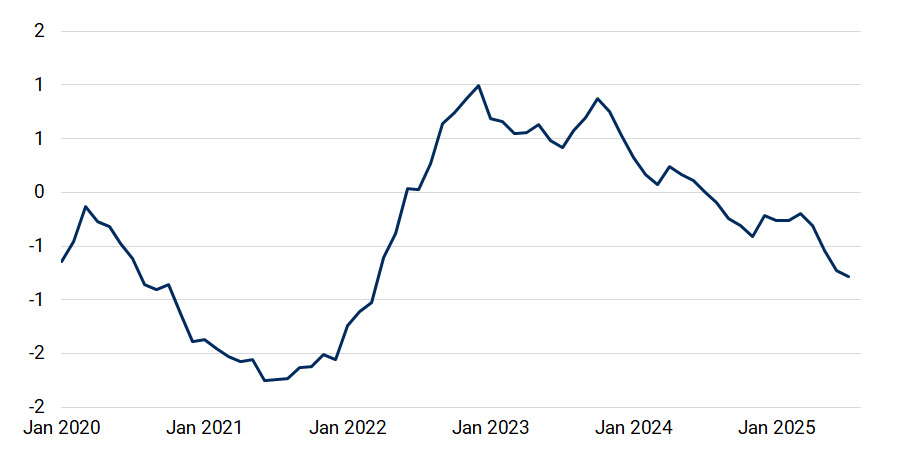

But is it restrictive? Monetary policy works through the impact of financial conditions on the economy. Stock markets are widely viewed as frothy. While financial conditions indices are hardly ironclad, they suggest conditions are accommodative (Figure 1 and 2).

Figure 1. Financial conditions are accommodative

Figure 2. Federal Reserve Board Financial Conditions Index

Source: Fed Notes, 30 June 2023, A New Index to Measure US Financial Conditions

Even the Fed acknowledged this: at the July FOMC meeting Fed Chair Jerome Powell noted that the economy did not seem to be held back by restrictive policy.

Looking ahead

The FOMC was more than able to frame a coherent narrative in support of the latest rate cut. One 25 basis point reduction in the FFR in and of itself will hardly shape the economic outlook. What matters is the path ahead.

Investors cheered the prospect of more rate cuts, pricing in a much faster path to a 3% FFR than the Fed has signalled. They should beware that the Fed’s own outlook might not add up. Two more rate cuts this year would bring the policy rate to 3.5% to 3.75%. With a push from tariffs, inflation might well rise above it. We would then have a negative policy rate in a resilient economy goosed from a fresh wave of tax cuts. It would be awkward and ill-advised for the Fed to cut further.

The foregoing begs a discussion of whether the mystical, mysterious, metaphysical and immeasurable nominal neutral rate is 3%, as the Fed’s dot plot suggests, or perhaps closer to 4%. Work by the Federal Reserve Bank of Cleveland estimates a nominal neutral rate of 3.7% – and that estimate is based on an inflation rate close to 2%.

Prior to the 2008 financial crisis, the long-term average of the real policy interest rate was about 2%. With the economy growing at the Fed’s estimate of potential at near 2%, this still sounds about right. Add a 2% inflation target, and the nominal neutral rate should be around 4% – even higher if inflation instead settles at 3%.

Moreover, longer-term rates, critical for investment decisions, don’t necessarily follow cuts in shorter-term rates, and there is ample evidence that if the FOMC gets ahead of itself, longer rates could back up. Indeed, the 10-year Treasury yield has risen since the September FOMC meeting. If inflation stays closer to 3% rather than 2% and if the nominal neutral rate is closer to 4% than 3%, severe market repricing could emerge and bond vigilantes will have their say.

Marco Annunziata is Co-Founder of Annunziata + Desai Advisors and former Chief Economist at General Electric and UniCredit. He writes the Just Think blog on Substack. Mark Sobel is US Chair of OMFIF.

Join OMFIF on 16 October to examine the outlook for US fiscal policy roundtable.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.