The Intergovernmental Panel on Climate Change uses shared socioeconomic pathways to project various climate scenarios for the remainder of the 21st century. These pathways represent different levels of global greenhouse gas emissions and ultimately different levels of temperature rise.

In recent years, there has been a growing integration of long-term scenarios into financial risk modelling and stress testing. This integration, while valuable for long-term planning, may limit the clarity with which present-day climate risks are interpreted. For instance, Figure 1 shows average annual temperature pathways in the US under different SSPs.

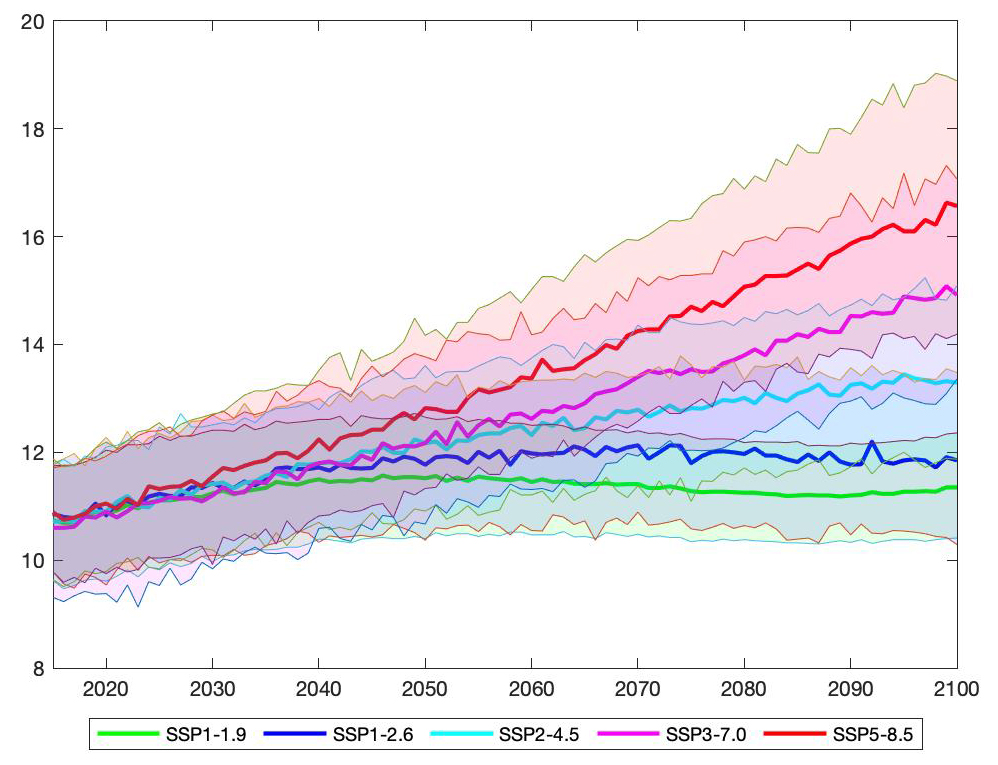

Figure 1. Long-term scenarios do not capture present-day climate uncertainty

US temperature pathways under different SSPs, on average (2020 – 2100)

Source: The World Bank: Climate Change Knowledge Portal 2025

Notes: Predicted mean surface temperature (in Celsius) for different SSPs in the US. Thick lines are the median projections of the ensemble across integrated assessment models used. The shaded area around the median depicts the range between the 90th and 10th percentile.

Two features of SSP-based projections highlight this challenge. First, while integrated assessment models provide long-term emission and warming pathways, they do not reflect near-term variability well. The shaded areas in Figure 1 (representing the 10th to 90th percentiles) show wide uncertainty bands that only begin to diverge meaningfully after 2050. Second, physical risk indicators – like tropical cyclone intensity or precipitation extremes – are projected to shift much later than we are already experiencing.

Traditional financial stress testing assumes macroeconomic shocks (such as inflation and supply disruption) stem from rare, exogenous events. By contrast, climate scenarios typically involve gradual transitions to new economic regimes over many years. If a bank were to calibrate models on these SSP trends, it would assume average gross domestic product growth and discounting through to 2040 or beyond – even in scenarios involving significant physical risk. This creates a misleading impression that acute climate risks are a distant concern.

The uncertainty of extreme outcomes

In reality, the effects of climate model uncertainty and intensifying climate extremes could be closer in time. The scientific community acknowledges that , natural variability and model limitations. For example, global climate models often oversimplify cloud behaviour and misplace key regions of tropical risk. In mid-latitudes, they underestimate the frequency of anticyclones – drivers of heatwaves, wildfires and drought. As a result, many extreme outcomes we currently observe cannot be explained by these models.

To fill this gap, climate scientists use weather event attribution to estimate how greenhouse gas emissions have changed the likelihood of specific events. Models are run simulating ‘possible weather’ under current climate conditions and ‘what might have been’ conditions without the atmospheric GHG concentration. However, as the 2021 study from Hossenfelder et al points out, the attribution outcome relies on climate models being able to simulate extreme events in the first place. If the models cannot reproduce observed extremes, they cannot estimate the probability ratio between the two conditions. This may inadvertently lead analysts to overlook extreme events, potentially skewing assessments towards less severe outcomes where probability ratios can be simulated more reliably.

Scientific disagreement further compounds near-term uncertainty. For instance, research from Knutson et al in 2020 found no consensus on whether carbon emissions have affected hurricane frequency or intensity in the North Atlantic. Some studies suggest fewer landfalls; others, more. Meanwhile, risks from tipping points – like ice sheet collapse or permafrost thaw – may manifest sooner than the slow trajectories depicted by long-term scenarios.

This uncertainty carries over into financial modelling.

Many climate risk vendors use coupled climate-catastrophe models to generate hazard scenarios, such as projections of hurricane activity. This method was applied in a study by Ranger and Niehoerster to generate risk scenarios for Florida in 2012. Users may be shown only a single ‘scientific view’ of the future, tied to a specific SSP. This could be, for example, sea surface temperatures in 2050, giving a false sense of precision while excluding a broader range of plausible outcomes. In the 2023 Federal Reserve Board climate scenario exercise, physical risk inputs were tied to SSP4.5 or SSP8.5 pathways, without considering the full distribution of uncertainty behind those choices.

Improving risk management

The Network for Greening the Financial System is aware of immediate climate risks and has recently published short-term scenarios to address them. To further enhance integration of short-term climate risk into financial stress testing, financial institutions and regulators could consider several enhancements.

We should distinguish observable risk from latent risk. Observable risk, like hurricanes and floods, have a known historical distribution and can already be quantified. Latent risk arises from model divergence and scientific uncertainty. While long-term SSPs offer valuable insights, financial institutions could benefit from also considering near-term climate uncertainties in their stress testing frameworks.

It may be helpful to draw on catastrophe modelling techniques, which integrate physical narratives and tail risk distributions to explore a spectrum of plausible scenarios – rather than presenting them as precise forecasts. This approach can help broaden the understanding of extreme outcomes. Additionally, reviewing near-term assumptions and hazard modelling is important as part of model governance, alongside validating long-term scenario selection.

Transparency is also critical. Financial institutions should have visibility into how vendors construct climate scenarios – not just which SSP is selected, but how physical risks are parameterised and constrained. Without this, model outputs may be misinterpreted as forecasts, rather than conditional ‘what if’ views of the future.

Finally, lightweight modelling tools or ‘nowcasting’ stress layers should be developed to complement long-term climate scenarios. These tools can help decision-makers understand the risks we face today – not just those we might face in 2050.

Disclaimer: The views expressed in this article are solely those of the authors and not those of Citigroup.