With the latest episode in the destructive US debt ceiling farce now over – once again underscoring the country’s lack of fiscal policy and extreme Congressional dysfunction – the financial commentariat can turn to its other favourite pastime: hyperventilating about Federal Open Market Committee actions.

As the 13-14 June FOMC meeting approaches, the Federal Reserve is facing a dilemma. Two teams are advocating for opposing outcomes. One team believes another federal funds rate hike should be skipped this month. This team importantly appears to include Jerome Powell, Federal Reserve chair, Philip Jefferson, vice chair designate, and Patrick Harker, president of the Federal Reserve Bank of Philadelphia.

The other team is arguing that at least another 25-basis points rate hike is in order. Both teams seem to agree that, once the FFR peaks, it should stay there for quite a while and markets are now falling in line. In any case, market rates are likely to remain propped up for a while as the Treasury replenishes its cash balances.

Team skip has tabled a range of arguments, as set out by Harker during an OMFIF conference held at the Philadelphia Fed headquarters. The Fed has already raised rates by some 500bp. Interest rate hikes act with lags and the FOMC should gauge the impact of past hikes before possibly moving forward again. Even if inflation is persistent, it is coming down and the process will take time. Patience is in order.

Some new data point to economic softening, especially in manufacturing. The unemployment rate rose in May and average hours worked declined slightly. Inflation expectations remain well anchored. Supply chain conditions are improving. Credit growth is slowing. The Fed should not crush the economy. The FOMC can always raise rates at its July meeting if warranted. A skip is not a pause.

But Powell has also stressed in recent months that the FOMC is ‘data dependent’.

Most data are backward looking or coincidental, not forward looking. And the data do not readily lend themselves to supporting a skip, according to proponents of a June hike. Even if headline inflation has declined, underlying price data, including for services, suggest core inflation is sticky, stubborn and persistent in the 4% to 5% range, well above the FOMC’s 2% inflation target.

The US labour market remains robust – payrolls have surprised to the upside for well over a year and did so again in May. Good labour market performance should support disposable income and consumption, the key US economic driver. Inflation cannot be brought down towards the 2% target without significant labour market slowing.

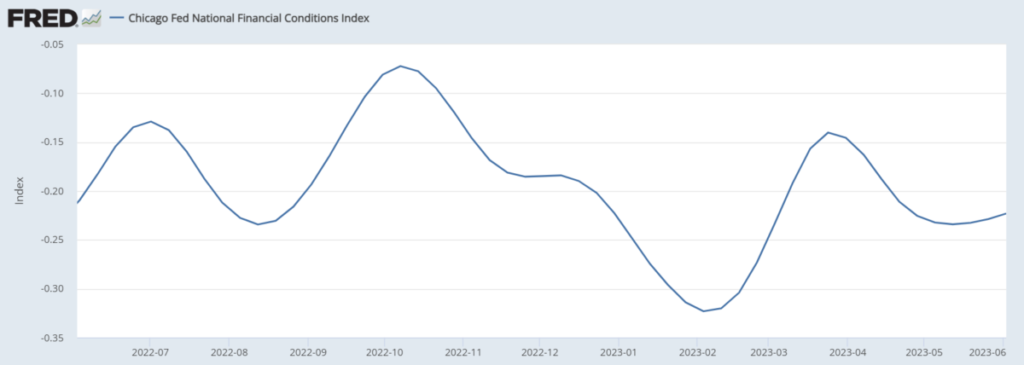

The latest banking wobbles appear behind us, at least for now. With the FFR at 5% and 10-year Treasuries around 3.75%, real rates are not restrictive. Corporate credit spreads are not rising. Financial conditions have eased in recent months (Figure 1).

Figure 1. Financial conditions have eased since April

Source: Federal Reserve Bank of Chicago

Source: Federal Reserve Bank of Chicago

As a result, data dependence may be hoisting team skip – rightly or wrongly – by its own petard. For the time being, given that the FOMC’s leadership is on team skip, the FFR is likely to remain unchanged at the June meeting, as is now strongly suggested by market expectations (although they could swing if the consumer price index data surprise markets sharply to the upside).

Team skip’s arguments might prove to be correct. The forthcoming decision may be finely balanced. Yet, if the FOMC decides to skip, it will need to acknowledge that risks may well warrant further rate hikes and that it stands ready to act – in other words, a ‘hawkish skip’.

Accordingly, the June FOMC meeting could pose communicational challenges, including for Powell’s press conference. These may be intensified by the dot plot’s release, which could see markups in growth and inflation and markdowns in the expected unemployment rate. If the Fed believes in data dependence, do the data on balance now support a hike? What fundamental change in new data could the FOMC expect over the next month? The possibility also exists that there could be dissents at the meeting – if so, how will Powell explain that?

There will be much on the line at the FOMC meeting and the financial commentariat will have another bite at the apple in late July. Perhaps ChatGPT could simply tell us the proper action to be taken on the FFR. But that would render the FOMC obsolete and deprive the world of the entertainment of heated, navel-gazing debates on whether 25bp moves in the FFR are the alpha and omega of the US economy.

Mark Sobel is US Chair of OMFIF.

Vincent Reinhart, chief economist and macro strategist at BNY Mellon and former director of the US Federal Reserve’s monetary division, is joining Mark Sobel to discuss the outcome of the June FOMC meeting. Register to attend here.