Autumn 2022

Rethinking the euro area’s economic model

The economic model that served the euro area in the decade before the pandemic is no longer fit for purpose, writes Katharine Neiss, chief European economist at PGIM Fixed Income.

An export-led economic model is no longer fit for purpose

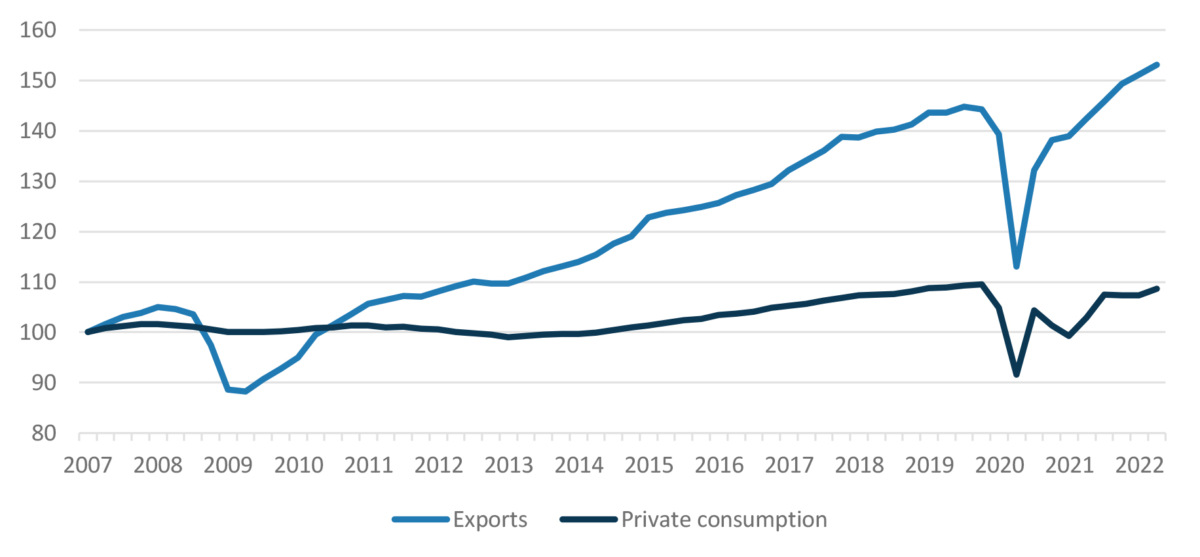

Weak growth in the euro area characterised the decade after the 2008 financial crisis and Europe’s sovereign debt crisis. But the region muddled through, largely via supercharged exports to the rest of world on the back of cheap energy imports (Figure 1).

As a result, the euro area’s trade surplus ballooned, making it the world’s most open large economic region. Manufactured exports from Germany, the Netherlands and Italy were key drivers, and deepened supply chain interconnections with central and eastern European countries that joined the European Union in 2004.

Figure 1: Components of euro area gross domestic product

Source: Macrobond

Yet, in the years leading up to the pandemic, this export-led model showed signs of strain. The euro area began to decouple from its third-largest trading partner after the 2016 UK referendum on EU membership. The Trump trade wars exposed the political limits of unfettered globalisation. Globally, trade stopped increasing as a share of gross domestic product and EU exports were flagging. Germany, the euro area’s export powerhouse, flirted with recession in the run-up to the pandemic, as exports and industrial output weakened.

Russia’s invasion of Ukraine has been the final nail in the coffin of Europe’s export-led, cheap-energy growth model. Reliable and sizable energy imports from Russia are a thing of the past. Both Italy and Germany – Europe’s largest manufacturing economies reliant on Russian gas imports – plan to wean themselves off Russian energy by late 2024. Alternative energy supplies are set to be significantly more expensive, at least for the foreseeable future.

Globally, the economic outlook is weak. Moreover, Europe’s key export markets look challenged. China is its largest goods trading partner, but growth there is slowing as policy-makers step away from market-based reforms and grapple with an inflated real estate sector. Lockdowns are expected to remain a virus management tool in China, further depressing activity. But when China sneezes, Europe catches a cold.

Europe cannot rely on trade with the rest of the world, as it has done in the past, to carry it through the next decade. In former German Chancellor Angela Merkel’s words, ‘We Europeans need to take our fate into our own hands’. Europe risks falling into decline unless it drives growth domestically. This will require a two-pronged approach starting with energy investment and further EU integration.

Europe needs home-grown growth, starting with energy investment. Russia’s invasion of Ukraine has increased the urgency with which Europe needs to overhaul its energy strategy. It has done better than expected in finding replacements for Russian energy going into the winter. That said, rationing of at least 15% will be required for demand to match the reduction in supply. If a complete stop in Russian energy flows occurred alongside a colder-than-average winter, more significant rationing is likely to be required to meet the shortfall.

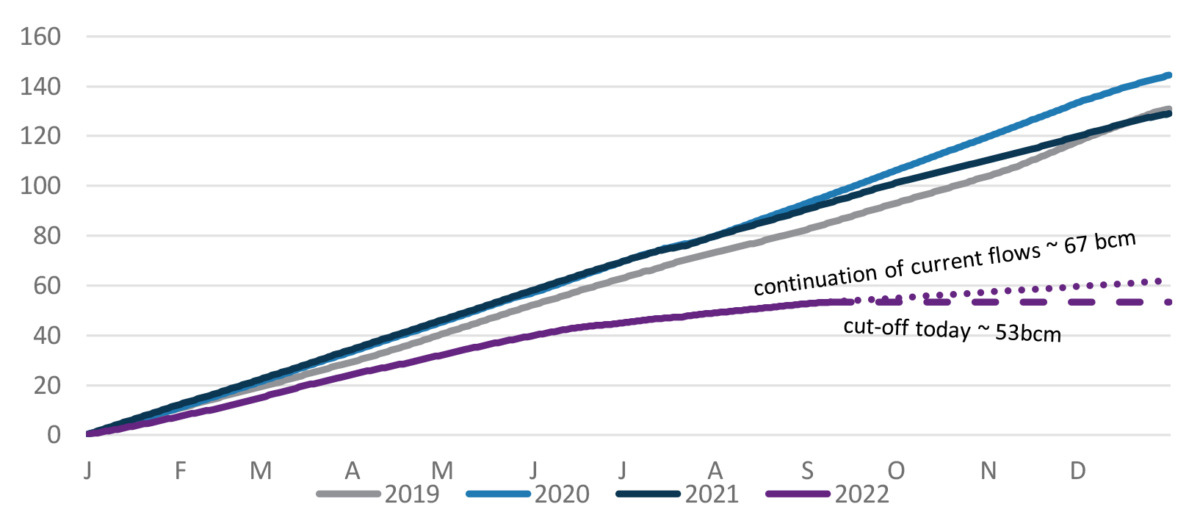

Imports of approximately 50bn cubic metres of Russian natural gas this year are about one-third what they were in previous years (Figure 2). However, the problem of replacing Russian gas extends beyond this winter. Subsequent winters may prove even more challenging.

Italy’s and Germany’s plans to wean themselves fully off Russian gas in an orderly tapering look optimistic. A good assumption is that imports in 2023 and beyond will be close to zero. Rustling up a further 15% of Europe’s gas needs in such a short space of time will be a tall order, since all other avenues, including pipeline flows and liquid natural gas imports, are already running at near-record highs.

Figure 2: Cumulative gas flows through major Russia-EU pipelines

Source: European Network of Transmission System Operators for Gas

Replacing Russian gas is not the only challenge. Alternative supplies need to reach where they are most needed. Broadly speaking, Europe’s existing infrastructure is based on moving gas from north to south and east to west. With Russian supplies under threat, that need has been turned on its head. Gas now needs to flow from south to north and west to east. For example, pipeline gas from Algeria and LNG from Spain need to flow to the rest of Europe.

Absent such infrastructure, regional pockets of vulnerability exist in industry-heavy, landlocked central and eastern Europe. These energy bottlenecks could turn out to be the mother of all supply chain disruptions. They risk amplifying across the EU in much the same way that regional pandemic lockdowns had knock-on effects globally.

Addressing these challenges requires a set of coordinated measures similar to the bold policy action taken by European policy-makers in 2020.

First, governments need to support households and firms through the energy crunch to prevent a downward spiral. Without targeted support, individually rational decisions to cut spending risk mass bankruptcy, unemployment and long-term economic scarring at the collective level.

Second, Europe needs a massive public-private partnership to accelerate energy alternatives and achieve scale on a compressed timetable, in much the same way that Covid-19 vaccines were developed and distributed. All options should be on the table, including nuclear energy and fracking. Europe’s position on fracking, for example, is undermined if it simply buys fracked gas from elsewhere. Without vision and will, the region’s ambition to scale up renewables from 17% to 45% of energy provision by 2030 looks unachievable.

Finally, fiscal and monetary policy need to continue to work hand in hand, to facilitate much-needed public and private investment. For these goals to be remotely achievable, it must happen alongside closer integration.

Close remaining fault lines to enable risk-sharing

To bang an old drum: the EU needs to remove the fault lines that prevent it from achieving its potential. Much of the focus since the continent’s sovereign debt crisis has been on fiscal risk sharing. Next Generation EU funds agreed in 2020 go some way towards plugging this gap, but they are temporary. Top-ups and extensions of these funds from 2027-30 would offer a ready vehicle to drive an accelerated green transition.

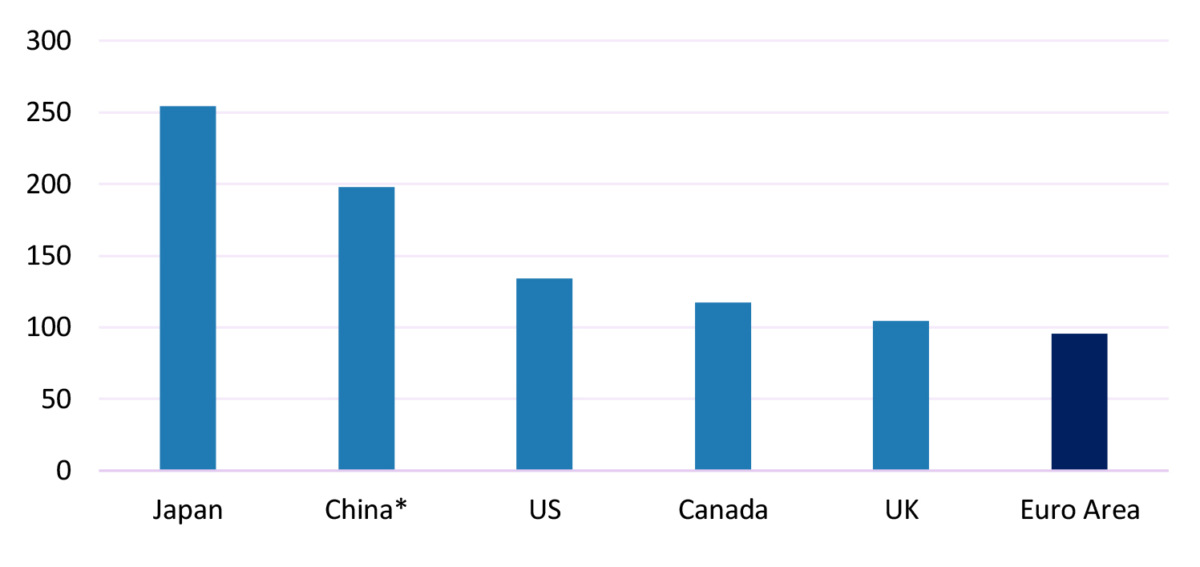

Contrary to many newspaper headlines, debt-to-GDP ratios remain low in Europe compared to other large economic areas (Figure 3). Scope exists for doing substantially more and future generations stand to inherit the investment enabled by increased debt. That said, in a world where investment needs to ramp up markedly, fiscal policy cannot deliver on its own. The size of the energy transition is too large.

Figure 3: Debt-to-GDP ratios

Source: Macrobond, PGIM Fixed Income

*PGIM estimate accounting for all debt of local government financing vehicles, all debt of local state-owned enterprises and 50% of the debt of central state-owned enterprises.

Looking beyond fiscal risk sharing, Europe needs a final push to deliver capital markets union. In principle, the EU has freedom of movement of persons, goods, services and capital. But the free movement of capital remains hampered by national rules, holding the region back.

Pockets of dynamism in Europe do exist. Skype, the world’s first major video conferencing platform, and BioNTech, makers of the first successful Covid-19 vaccine, are just two examples. Yet, like many other European firms, they were unable to scale up operations with purely domestic funding.

More generally, European firms remain overly reliant on bank funding. Capital market access remains limited and stifles otherwise high-growth firms. If scaling up investment is to be remotely achievable, Europe needs to integrate its national capital markets and create a genuine single capital market.