Every year, OMFIF’s Global Public Investor captures a moment in the evolution of official investment, with some years defined by a single shock and others by a turning point in markets. This year’s report is different because it points to something more durable: a world in which volatility is no longer a phase to get through, but a condition to be managed.

For central banks, sovereign funds and public pension funds, this demands a different kind of discipline. The challenge is not simply to respond to higher rates, geopolitical risk or changes in the monetary system, but to build portfolios and institutions that can continue to operate when all these forces are moving at once. The old assumption that public investors can wait for the environment to normalise looks increasingly unrealistic.

The title of this year’s report, ‘Riding the wave’, reflects that shift. Public investors are not standing still, but neither are they making reckless moves. Instead, they are adjusting cautiously, testing new tools, diversifying where possible and holding on to the principles that have always defined official investment on safety, liquidity and long-term value.

In total, GPI draws on insights from a survey of 90 central banks, public pension funds and sovereign funds with over $10tn in assets under management. The report provides an important view of how public investors at the heart of the global financial system are navigating a more fragmented, volatile and technologically complex world.

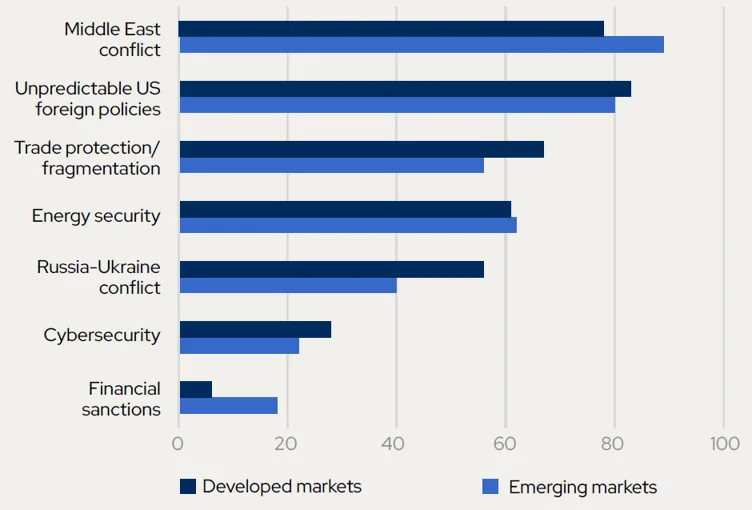

The shocks that have shaped reserve management strategies in recent years have not disappeared, but they have changed form. Policy rates remain the dominant near-term driver of investment decisions. Geopolitical risk has become broader and more persistent, moving beyond last year’s focus on trade protection. In 2026, reserve managers’ concerns centre on the Middle East conflict, unpredictable US foreign policy and energy security (Figure 1).

Figure 1. Middle East conflict tops risk concerns

Which geopolitical risks most concern you? Share of respondents, %

Source: Global Public Investor 2026 survey

Capital preservation remains the leading investment objective, while sovereign risk repricing is viewed as the biggest threat to global financial stability over the same period.

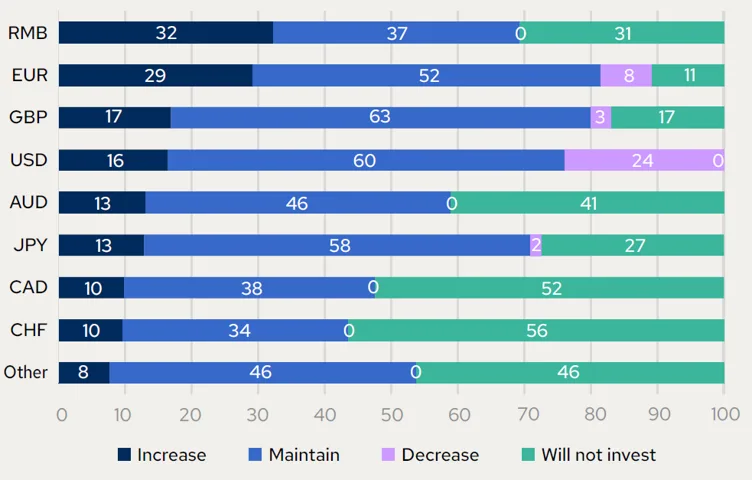

The dollar continues to dominate portfolios and is still viewed as unmatched for safety and liquidity. But central banks increasingly expect to reduce dollar allocations over both the short and long term, especially in emerging markets. For the first time since the GPI series began recording reserve managers’ long-term intentions in 2023, more central banks plan to decrease their dollar holdings than increase over the next 10 years (Figure 2). The euro and renminbi remain the main alternatives, while interest in smaller developed and emerging market currencies is rising. This year, 29% of respondents plan to increase euro holdings in the long term, up from 22% last year.

However, neither the euro nor the renminbi fully solves reserve managers’ problem: the former lacks a single, deep safe asset market, while the latter remains constrained by market structure and geopolitical concerns.

Figure 2. Dollar decrease over the long term

Over the next 10 years, do you anticipate increasing, decreasing or maintaining your exposure to the following currencies? Share of respondents, %

Source: Global Public Investor 2026 survey

Gold has become the clearest beneficiary of this uncertainty. It leads short-term buying intentions and has moved to the centre of reserve strategies as a hedge against geopolitical risk and concerns about the international monetary system. In 2026, 82% of central banks hold physical gold, up from 71% last year.

A net 30% plan to increase their gold allocation over the next one to two years, while 61% expect the price to settle between $5,000 and $6,000 per ounce by June 2027. Only 28% say the current price is discouraging further purchases. The motivation behind gold purchases is increasingly strategic rather than purely financial. Protection against geopolitical risk is cited by 51% of respondents, up 11% from 2024.

This year’s report also shows that adaptation is not only about asset allocation, as technology is becoming a more serious part of the reserve management conversation. Central banks are considering how best to integrate artificial intelligence and capitalise on the promise of greater efficiency, stronger analysis and better decision-making. Yet integration also introduces new questions around governance, model risk and cyber resilience.

Public pension and sovereign funds face a parallel challenge: they must meet long-term liabilities while navigating inflation, geopolitical uncertainty and shifting patterns of global growth. Their interest in real assets, emerging markets and AI-related opportunities reflects a willingness to look beyond immediate volatility while remaining selective about where and how they take risk.

Official institutions are not chasing every wave, but choosing carefully which ones to ride, and this is the central message of GPI this year. In a world of shifting tides, caution no longer means standing still but preserving optionality and being ready to move when the current changes.

Our thanks go to the central banks, sovereign funds and public pension funds that contributed to this year’s research. Their participation allows GPI to continue documenting how official institutions are adapting their portfolios, operations and long-term strategies as the financial system around them becomes more fragmented and complex.

Yara Aziz is Senior Economist at OMFIF.

Download Global Public Investor 2026.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.