The promise of environmental, social and governance bond markets is to promote sustainable practices through market mechanisms. OMFIF’s 2026 Public Sector Debt Outlook Survey of sovereign, sub-sovereign, supranational and agency issuers finds that market momentum may be declining. Issuance in 2025, which stood at $1.5tn, was down year-on-year, and well below the 2021 peak of $1.9tn.

Almost 20 years after the European Investment Bank’s inaugural climate awareness bond in 2007, the premiums offered by investors for green securities are declining. Secondary market liquidity remains moribund and the absence of standardisation continues to constrain the expansion of the ESG bond market. An equilibrium of stasis prevails in the market.

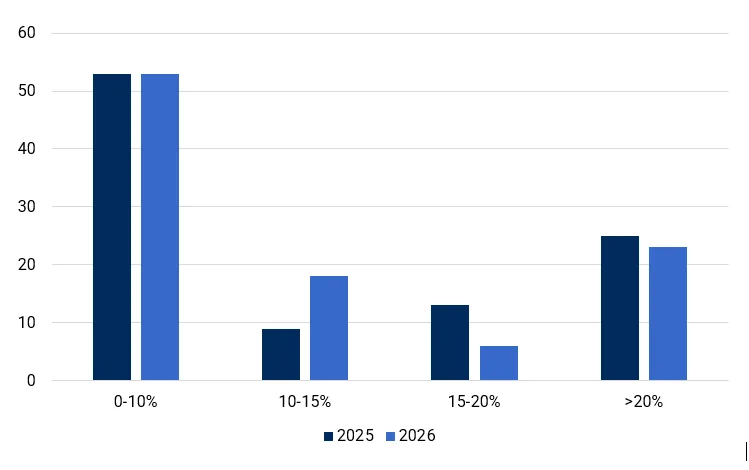

The European Union’s Green Bond Standard, launched in December 2024, was intended to catalyse the standardisation and fungibility that would increase secondary market liquidity and lift the market from stasis. However, the effects of this policy change have not come through in our survey. Between 2025 and 2026, issuers have not increased the share of funding they expect to allocate to ESG issuance (Figure 1).

Figure 1. Issuers are not increasing ESG issuance

What proportion of your issuance will be in ESG format in 2026? Share of respondents, %

Source: OMFIF Public Sector Debt Outlook Survey 2026

One purported incentive for ESG issuance is the existence of a ‘greenium’ – a spread concession that issuers earn from the willingness of certain market participants to forgo returns in exchange for owning ESG securities. However, confidence in such a concession is waning: just half our respondents believe that the greenium exists. Among these respondents, there was substantial disagreement over the size of the greenium, with some reporting below 3 basis points and others less than 1bp. If it does exist, it is shrinking.

Liquidity problems

Issuers continuing to operate in the ESG bond market almost universally reported opting to issue use-of-proceeds bonds rather than sustainability-linked issuance forms, with the dial moving little on this data point since last year’s survey. Use-of-proceeds bonds are defined by the destination of the funds raised. Sustainability-linked bonds, by contrast, make no restriction on how proceeds are used, but rather tie characteristics of the bond, such as the level of its coupon, to key performance indicators such as decarbonisation goals.

While both forms have their merits, one consideration is that use-of-proceeds bonds issued by sovereigns and SSAs channel capital towards green projects that would already be funded. SLBs offer more explicit incentives for sustainable practices by tying real-world outcomes to repayment profiles. However, these incentives often result in non-standardised issuance formats, with payoff profiles often difficult to model probabilistically with any degree of accuracy, posing serious challenges for their secondary market liquidity.

Non-standardised issuance formats hamper the development of a sustainable repurchase agreement market, which imposes a cost in the form of illiquidity for the holders of ESG securities. Expectations for the development of such a market were low in 2025 and in 2026 the picture is even bleaker. While around 30% of respondents saw some hope for its development last year, just 6% reported any expectation of expansion in 2026.

While a number of impediments to its development were cited, including its insufficient scale and the lack of any specialness for issues that may act as economic incentives to participate, the most commonly cited was weak underlying secondary market liquidity for ESG bonds. Like so many market infrastructure constraint problems, there is a chicken-and-egg problem here, where secondary market liquidity is constrained by the absence of an ESG repo market, but the development of such a market is constrained by the illiquidity of the securities.

Illiquidity, and the associated difficulties in pricing, managing and hedging positions, reduces dealers’ ability and willingness to intermediate ESG bond markets, compounding the problem further. No silver bullet exists, but the EuGBS may ease some of the pressure by driving standardisation across ESG bond features, increasing fungibility and, by extension, liquidity.

EuGBS as a catalyst for standardisation

The EuGBS is a voluntary standard for ESG bonds. The aim is to define uniform requirements for issuers, establish a registration and supervisory system for external review and provide templates for mandated disclosures and allocation reports. In principle, such standardisation should increase secondary market liquidity through increasing the fungibility of securities, thereby easing the development of a sustainable repo market.

The EuGBS joins the Climate Bonds Initiative’s Climate Bond Standard and the International Capital Market Association’s Green Bond Principles as market standards under which issuers may structure an ESG bond. To date, the ICMA GBP label, which is the most flexible in application, has seen the most uptake on the market. EuGBS tightens the standards for, and homogenises the meaning of, ESG bonds relative to the ICMA GBP.

However, compared with CBI standards, EuGBS are looser on some metrics. For example, in percentage limits on the allocation of funds, CBI standards require 95% of proceeds to be fully aligned with the eligibility criteria, while EuGBS requires an allocation of 85% of proceeds to be EU taxonomy-aligned. EuGBS is positioned as a middle-ground that both increases the verifiable impact of ESG bonds relative to ICMA standards and streamlines the process relative to the strict CBI standards.

As of February 2026, €22bn in EuGBS labelled bonds were outstanding with sovereign and SSA issuance constituting around half the market. Demand for issuance has been strong, as evidenced by consistently high oversubscription rates. However, structural constraints remain. EuGBS is, by design, a use-of-proceeds instrument, and its scope is limited to taxonomy-aligned activities – a subset of the broader ESG bond universe.

Equilibrium of stasis

While the EuGBS standard is a necessary step in the right direction, it is insufficient to meet the market’s standardisation needs. EuGBS is a supply-side intervention, which improves the verifiability of ESG credentials and the fungibility of ESG securities, but it does not directly address the demand-side infrastructure constraints that define the market’s equilibrium of stasis. In theory, standardisation should enhance secondary market liquidity, but the evidence is mixed and our survey participants do not have high hopes for the development of the sustainable repo market.

As it stands, EuGBS may increase the green credentials of the average ESG bond, but it will not on its own reshape the market. With the greenium compressing, issuers see diminishing incentives to enter; with liquidity stagnant, investors still face disincentives to hold. Unless EuGBS catalyses substantial further investor appetite, the ESG bond market will remain stuck in equilibrium.

Conor Perry is an Economist and Jordan Nann is an Account and Content Executive at OMFIF.

Join OMFIF on 17 April at the International Monetary Fund-World Bank spring meetings to explore nature-related risk.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.