Over the past three years, the market for sovereign and sub-sovereign, supranational and agency bonds has been changing. The end of ultra-low rates in the euro area in 2022, followed by the beginning of quantitative tightening, has increased volatility in rates markets. The removal of the European Central Bank as the marginal buyer has diminished secondary market liquidity. Deteriorating fiscal positions and global trade disputes have amplified market volatility, and recurrent geopolitical ructions have made matters worse. This volatility gives rise to unevenly distributed benefits and costs among SSA issuers.

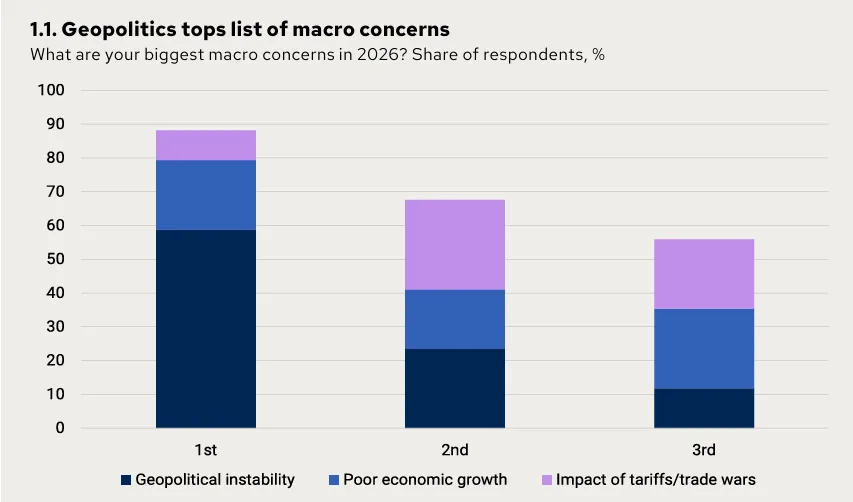

OMFIF’s 2026 Public Sector Debt Outlook Survey reveals issuers are most concerned about the least predictable form of volatility. Almost 95% of respondents ranked geopolitics in their top three macro concerns, while more than half identified it as the top concern (Figure 1). Importantly, respondents who place geopolitics first among their macro concerns are disproportionately more likely to place volatile markets in their top three funding concerns.

Figure 1. Geopolitics tops list of macro concerns

What are your biggest macro concerns in 2026? Share of respondents, %

Source: OMFIF Public Sector Debt Outlook Survey 2026

Primary market anxieties

Geopolitical risk disrupts the planning and implementation of funding strategies. Unpredictable market volatility induces issuers to offer concessions to investors in the primary market in the form of higher new issue premiums – spreads paid over the yield of comparably dated bonds of the same issuer trading on secondary markets.

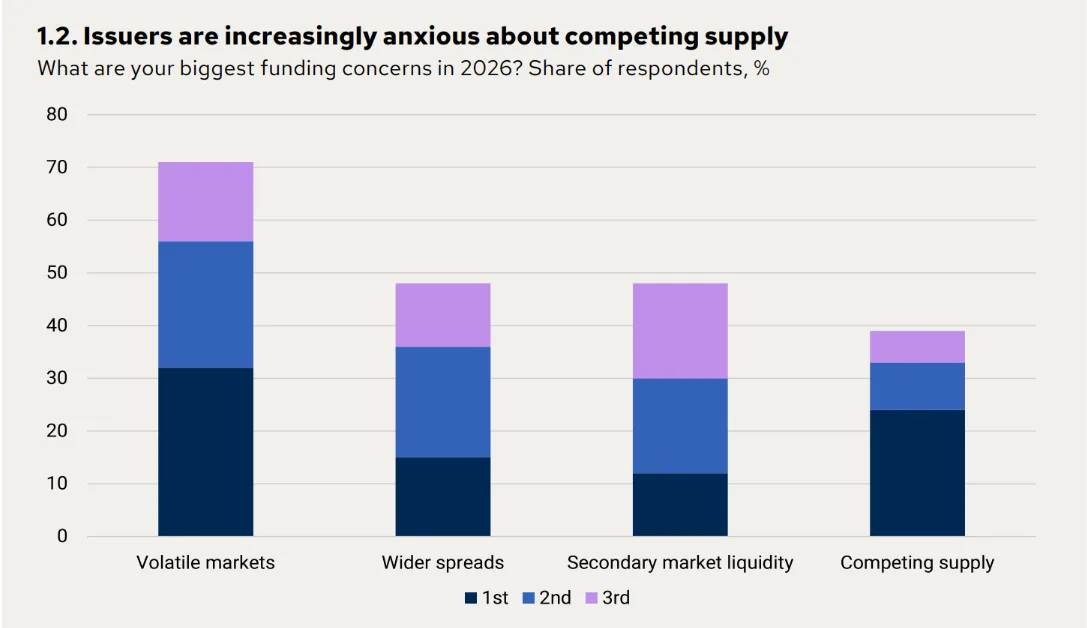

Expectations of its recurrence may also result in greater competition during issuance windows in predictably calm market conditions. Rarely are multiple benchmark deals offered on the same day in primary markets, and issuers attempt to avoid such conditions to diminish the possibility of investor fatigue, necessitating precisely the new issuance premiums they seek to avoid. However, our survey data show issuers are increasingly anxious about competing supply windows, with almost 40% of respondents ranking it in their top three funding concerns (Figure 2).

Figure 2. Issuers are increasingly anxious about competing supply

What are your biggest funding concerns in 2026? Share of respondents, %

Source: OMFIF PSDO Survey 2026

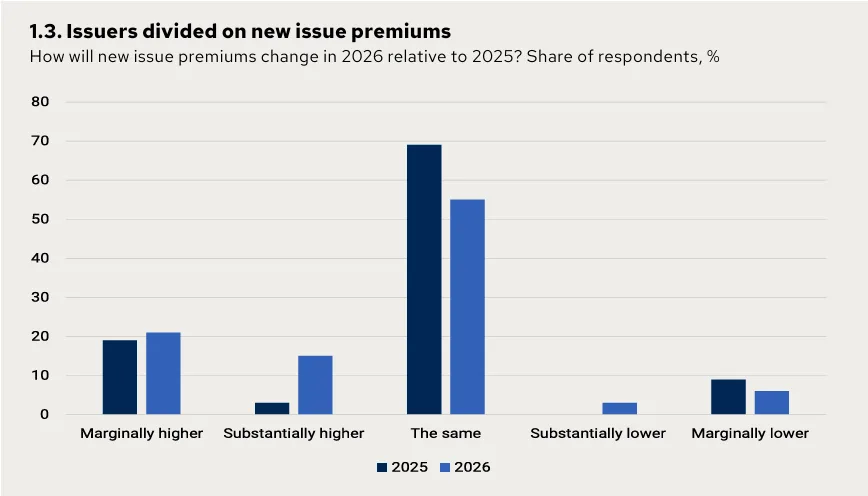

There is also a net expectation of higher new issue premiums in 2026 relative to 2025. However, just as interesting is the increased variance of opinion between the two years (Figure 3). In a changing market, the range of possible market outcomes feels wider, generating greater variety of opinion among issuers. This variety reflects a combination of increased uncertainty and differences in expectations around anticipated costs of market volatility between issuers.

Figure 3. Issuers divided on new issue premiums

How will new issue premiums change in 2026 relative to 2025? Share of respondents, %

Source: OMFIF PSDO Survey 2026

In the current climate of recurrent geopolitical risk events, NIP anxieties feed through into our data on the extent of front-loading. We found a 34-percentage point increase in the number of issuers who expect to complete less than half of their funding by the end of Q2, relative to our 2025 data. A Damoclean sword hangs above the head of SSA issuers in the current market environment, and many feel it better to postpone funding than risk the sword falling mid-deal, thereby forcing material spread concessions on their issuance.

Secondary market hopes

On secondary markets, the story is different. We found a net expectation of tightening in issuers’ benchmark 10-year asset swap spread of their main issuance currency. This contradicts the prevailing market wisdom that SSA swap spreads are set to widen slightly this year in the face of heightened supply from the European Union and Germany. There are three classes of explanation that contextualise this data point.

The first is that issuers think that, while peer institution spreads may widen, their spreads will remain nice and tight: call this hubris. The second is that the spread pick-up for moving from SSAs into riskier assets is at record lows, and this is potentially supportive of SSA spreads: call this the relative value effect. Third, and most analytically appealing, is the idea that spread tightening may be caused by volatility itself. Issuers anticipate that under the conditions of geopolitical risk events, tariff-driven disruption and sovereign downgrade in peer nations, they are best placed to benefit from a flight to quality. Call this the volatility dividend.

On this third explanation, the degree to which the sovereigns and SSAs in our survey are well placed to benefit will be variable, dictated by the strength of the sovereign credit rating, the liquidity of their debt stock and the stability of their financial condition.

Smaller SSAs, and those tied to weaker sovereigns like French agency issuers, will face no flight-to-quality effect under renewed market volatility; depending on the category of the risk event, they could see their spreads widen. By contrast, strong SSAs, like the German Laender, would most likely see modest secondary market spread compression – in times of uncertainty, investors buy safe assets.

Depending on the magnitude of the effects, higher NIPs could actually be offset by tighter secondary market spreads, meaning that, for some issuers, all-in funding costs may decrease, even if the Damoclean sword of geopolitical risk falls during a deal. While this outcome is not particularly high probability, its possibility exemplifies how volatile markets redistribute costs and benefits between stronger and weaker SSAs.

Arbitrary and non-arbitrary redistribution

Not all sources of volatility are equal in the market, nor do they all have equal impacts. The most feared kind of volatility, driven by geopolitical risk, causes primary markets to freeze. Excluding certain issuers with pre-committed issuance schedules, such as many sovereigns, those who can bide their time, do so. The threat of such events in this new regime for SSAs is reducing expectations for pre-funding, increasing expected NIPs and fanning fears of issuers competing for limited demand during the few predictably calm issuance windows.

However, other types of risk event discriminate more clearly between SSAs. Sovereign downgrades, trade policy uncertainty and economic growth concerns affect different SSAs differentially. Some earn the volatility dividend as spooked investors determine their paper to be sufficiently safe and liquid to hold and bid it up in an effort to flee more volatile assets. Others find their paper classed within the assets that investors dump.

Our survey suggests that issuers are near unanimous in their expectations of heightened volatility, but they differ on where they expect themselves to land in the fallout. Some see an impending volatility dividend, others expect a rough year in funding markets.

Conor Perry is an Economist at OMFIF.

Join OMFIF on 12 May for the Defence funding forum.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.