‘There is no substitute to the dollar… not the renminbi, not the euro’, said a prominent former central banker at an OMFIF gathering in London to mark the launch of Can Europe Survive?, a new book by David Marsh.

But the real question is not whether the dollar will disappear from its dominant position; rather it is how central banks and sovereign investors are managing the risks of relying so heavily on it at a time when politics, technology and markets are pulling in new and contradictory directions.

Geopolitics has always influenced financial flows, but it now shapes reserve management decisions. Tariffs, sanctions and the weaponisation of payments systems can no longer be ignored. They are the filter through which allocation decisions are made.

One speaker at the book launch described how many countries feel ‘caught in a dollar spider web’ – bound into a system they distrust but unable to leave. The US use of sanctions and extraterritorial law has encouraged more states to experiment with alternative payments systems and digital currencies, but the underlying infrastructure of global finance, from invoicing and settlement to debt markets and foreign exchange turnover, remains firmly dollar-centric.

Why alternatives fall short

Most central banks still hold the majority of their assets in dollars and for many this remains unavoidable. Dollar assets offer liquidity, depth and a benchmark for safety that no rival currency can currently match.

The euro, despite being a major invoicing currency, cannot claim global status. Without a unified capital market and a truly pan-European safe asset, its role remains regional. As one participant said, ‘The euro cannot aspire to be a truly global currency without sufficient safe bonds and a deep, liquid pan-European market – and that will not happen’.

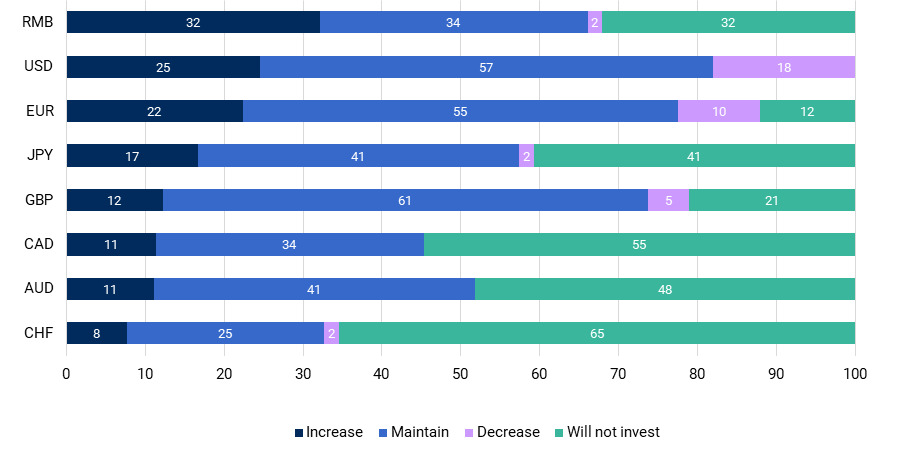

The renminbi is viewed as a potential long-term player (Figure 1) but is constrained by limited openness, capital controls and weak institutional credibility. Other currencies are simply too small. Even where diversification away from dollar happens, it is at the margins.

Figure 1. Central banks plan to increase their exposure to the renminbi

Over the next 10 years, are you planning to increase, decrease or maintain your exposure to the following currencies?

Source: OMFIF Global Public Investor 2025 survey

The gold comeback

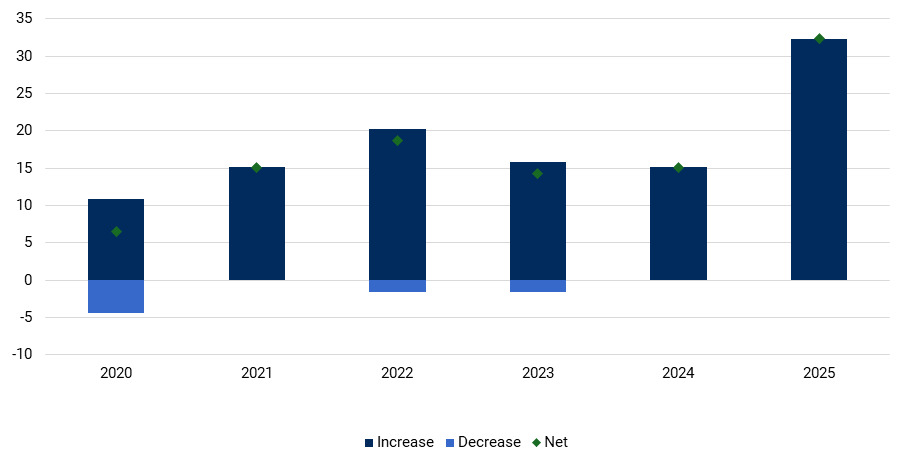

With currencies constrained, gold has re-emerged as a serious part of the debate. Some central banks have added record amounts to their reserves in the past two years, citing its neutrality, sanction-proof qualities and role as a hedge against shocks (Figure 2).

At the book launch, speakers observed that ‘the beauty of gold is the intrinsic value of the metal’. In addition to its sentimental and emotional factors, gold has an agreed value across all nations, ‘which is quite impressive’. As such, several speakers declared ‘the gold rush is just beginning’.

Figure 2. Gold has come to the fore

Over the next 12-24 months, do you expect to increase, decrease or maintain your allocations to gold? Share of respondents, %

Source: OMFIF Global Public Investor 2020-25 survey

Others remain cautious, stressing gold’s lack of yield and limited liquidity, signalling risks of large transactions. For many institutions, the challenge is how to balance its value as insurance against its drawbacks as an investment.

Looking ahead, tokenised gold was flagged as a potential innovation by participants at the launch, though for now its role remains largely conceptual. One speaker observed that gold is clunky and difficult to move, but ‘putting it on a digital rail makes it tradeable 24/7’.

Technology and AI

Technology adds a layer of uncertainty and potential for transformation to the landscape of reserve management. New payments systems and digital settlement tools could accelerate shifts in currency use, even if they do not by themselves create trust or safe assets. As one participant noted, ‘Technology won’t replace the fundamentals of trust and safe assets, but it will make shifts happen faster once they begin’.

Artificial intelligence is already being used in more subtle ways. Central banks are using it for scenario modelling, risk diagnostics and operational resilience. For now, it is a tool rather than a disruptor. But expectations are high, and markets are already priced for the productivity gains that may or may not materialise. In recent conversations OMFIF has had with central banks, several highlighted the need to build in-house expertise, both to capture potential benefits and to manage the rising risks of cyberattacks and overreliance on external providers.

Reserve management in a fractured world

Reserve managers are caught between two truths. They cannot abandon the dollar, but they cannot ignore the risks either. Diversification into gold, experiments with alternative payments systems and more attention to political risk are all signs of adjusting to a more multipolar world. But none changes the fact that the dollar remains at the core of the system.

OMFIF – in partnership with BNY, Bridgewater and Capital Group – has been holding a series of confidential conversations with reserve managers from Europe, Latin America, Africa and Asia. These discussions build on the findings of our flagship Global Public Investor 2025 report and offer a closer look at how central banks are navigating a rapidly shifting economic and geopolitical landscape.

The insights will be discussed further at an OMFIF roundtable during the International Monetary Fund-World Bank annual meetings in Washington DC on 16 October, where we will bring together leading voices from the Bank of Korea, Bank of Finland and Bank of Lithuania. A Global Public Investor Working Group 2025 report, distilling the findings of our conversations, will be launched virtually on 20 November 2025.

Yara Aziz is Senior Economist at OMFIF.

Join OMFIF on 16 October to examine reserve management in a volatile world.