Far from marking a retreat from climate action, recent gatherings of market stakeholders in major financial capitals have underscored just how increasingly material climate risk and transition planning are becoming to financial decision-making.

New York and London’s climate weeks both saw record attendance and the launch of major new initiatives, notably regarding transition finance and planning. The backdrop to these events has been the stark reality of rising emissions, while real-world impacts of extreme weather brought home the urgency of climate action.

This year, London and New York experienced their hottest and second-hottest summers on record, respectively, while Hong Kong was battered by the ‘super typhoon’ Ragasa in September, causing widespread damage and economic disruption. Economic losses related to extreme weather over the summer amounted to €43bn in Europe alone, according to reports.

No major retreat from climate commitments

Despite some jurisdictions reducing or streamlining certain green policies, we observe no significant retreat from climate commitments by financial market participants themselves. Firms are increasingly reporting their climate risk exposures, and their mitigation and adaptation commitments, providing much greater transparency for lenders, investors and regulators than existed just a few years ago.

To gauge the current state of climate commitments among issuers of corporate bonds, we curated a sample of some of the largest bond issuers globally, representing diverse corporate sectors and representing nearly $5tn in annual revenues. For each company, we compared the latest climate commitments communicated in official announcements with previous statements.

Our study found 57% of issuers are maintaining their climate commitments, while 30% are increasing them – by adding commitments, expanding the sectors targeted for financed emissions (in the case of financial institutions) or adopting more aggressive timeframes (Figure 1).

Those reducing their climate commitments were predominantly in the banking and oil and gas sectors. In a few cases, entities cited regulatory uncertainty or changes in market conditions as reasons for scaling back their earlier pledges.

Figure 1. Most financial institutions are maintaining or increasing commitments

Note: N = 40 large issuers.

Source: Sustainable Fitch

Focus shifts to credibility and implementation

The key shift we observe is entities moving away from making new high-level, attention-grabbing pledges. Instead, there is an evolution happening, with the focus turning to credibility, implementation and accountability with respect to climate-related commitments, with an intention to deliver decision-useful information. This is most evident in the rising numbers of companies disclosing climate transition plans, facilitated by new requirements and guidance announced by regulators and standard-setters over the past year.

There were several key developments at London Climate Action Week. The International Sustainability Standards Board released its transition plan-related disclosure guidance, the UK government launched a formal consultation on transition plan requirements and the Global Reporting Initiative (which issues standards used in impact reporting) announced its new climate standard, which now includes a transition plan requirement.

Disclosure of transition plans can help investors, lenders and other stakeholders to better assess companies’ exposure to, and management of, transition risk. They can also support entities in high-emitting and hard-to-abate sectors (such as fossil fuel energy and heavy industry) to access transition finance – capital that is deployed specifically to enable these companies to decarbonise.

Transition plan elements are core components of market frameworks for transition finance, such as the draft guidelines issued by the UK’s Transition Finance Council in August.

Transition assessments reveal decarbonisation hurdles

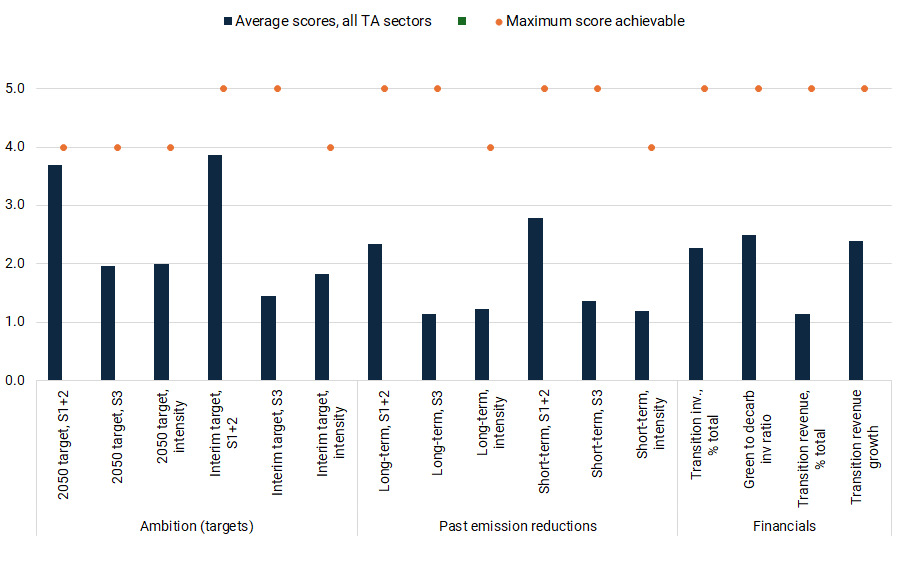

Our approach to evaluating the credibility, level of ambition and implementation of an entity’s transition plan is the Sustainable Fitch Transition Assessment.

We review the scale of emissions cuts pledged by the company and the progress it has already made on decarbonising its operations and value chains. In both cases, scoring thresholds are informed by credible decarbonisation pathways appropriate to the relevant high-emitting/hard-to-abate sector. Further adjustments are made to the final grading, reflecting factors such as high-impact decarbonisation levers, carbon lock-in and governance/transparency.

Based on the assessments we have conducted to date we observe that most assessed entities feature robust targets covering their direct emissions and emissions related to purchased energy (scope 1 and 2). However, value chain-related emissions targets (scope 3) remain a weak area, with several entities scoring zero out of five, indicating no target. This includes several oil and gas and mining companies, for whom scope 3 represents by far the largest component of their carbon footprints (typically over 85%).

Figure 2. Scope 1 and 2 targets far more common than scope 3

Transition assessment average scores

Note: Scores out of 4 or 5, where 0 = worst. N = 36 assessments (mix of solicited and unsolicited/desktop TAs). N = 36 assessments (mix of solicited and unsolicited/desktop TAs. Data as of September 2025

Source: Sustainable Fitch

The pattern is consistent across Sustainable Fitch’s wider universe of over 2,500 rated and scored entities. Of those with an emissions target, those relating to scope 1 and 2 are most common, while a minority have adopted scope 3 targets. A common issue we came across is the comparability of targets.

In addition to different baselines, organisational boundaries and GHGs covered by targets, we noted a wide variety of intensity metrics such as emissions per employee and emissions per square metre of floor space (common in real estate), complicating comparative analysis of borrowers and investee companies’ decarbonisation trajectories across different sectors.

Credible transition plans should also indicate how climate commitments align with the company’s broader business strategy. Our TA assesses the share of investment entities allocated to transition-related activities (such as low-carbon technologies and measures to improve carbon efficiency) and the share of, and growth in, revenues being generated from these activities. All the assessed entities allocate some investment to the transition projects – indeed, nearly a fifth of entities in the sample of completed TAs allocate over 50% of total investment (capital expenditure and operating expenditure) to transitioning.

However, revenue data indicate most entities are yet to transform their business models towards low-carbon activities, with most generating less than 1% of total revenue from such activities.

William Attwell is Director of Climate Research at Sustainable Fitch.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.