Continued dollar strength and associated pressures on global finance may be the hallmark of 2025 foreign exchange markets, especially the first half of the year, notwithstanding the dollar’s large ‘overvaluation’ and massive current account deficit.

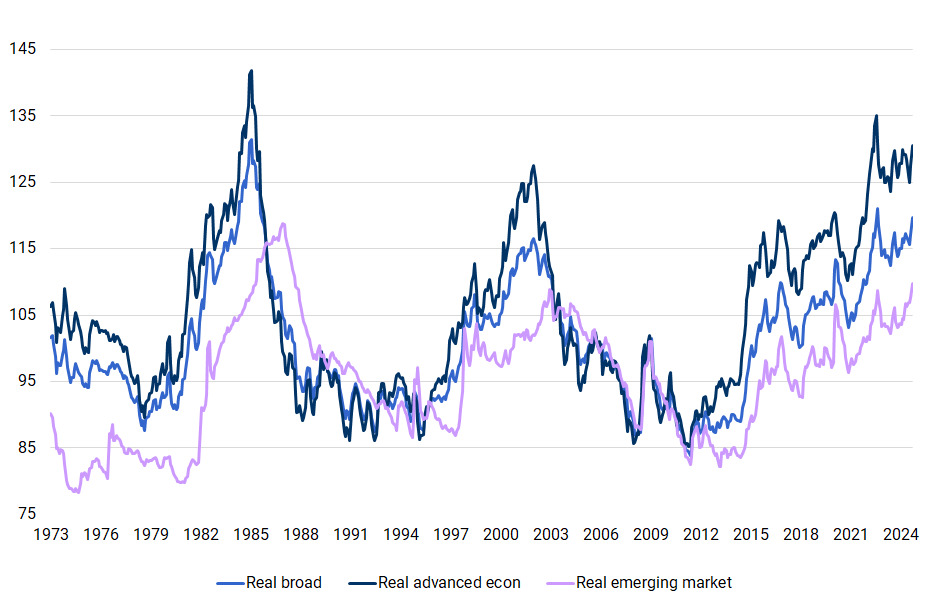

The real trade-weighted dollar is extremely strong and getting stronger, though still shy of Plaza Accord-era heights (Figure 1). Given dollar strength and strong relative demand, the US is heading in 2025 towards a huge current account deficit, perhaps pushing 4% of gross domestic product.

Figure 1. Real-trade weighted dollar extremely strong

Source: Derived from Federal Reserve data, through November 2024

Financing lofty dollar ‘overvaluation’ and a massive current account deficit might herald a major dollar reversal. But that is not in the cards as strong demand for dollar assets will underpin the buck. Don’t bet on a Mar-a-Lago Accord or dollar ‘devaluation’.

The Federal Reserve faces sticky services prices and a relatively robust economy, complicating efforts to cross the last mile in getting inflation back on target. With the Fed having already scaled back expected 2025 rate cuts from 100 to 50 basis points and financial conditions being arguably accommodative, some ask if any cuts can be expected.

Longer-term rates are rising. That is also due to expectations President Donald Trump will largely succeed in extending the 2017 tax cuts and promulgating others, swelling an irresponsible 7% of GDP budget deficit and associated financing pressures.

Additionally, tariff threats, even if partly implemented, will render exports to the US less competitive, dealing a blow to foreign currencies. Higher tariffs and deportations will prop up inflation. Trump’s bluster will heighten global uncertainties and the dollar tends to appreciate in a risk-off environment.

In short, all signs point to continued extreme dollar strength. But in currency markets, it takes two to tango.

Prospects for euro strengthening are dim. Good progress is being made in getting inflation back to target, while the euro area economy languishes. Markets expect that the European Central Bank will cut its deposit rate by at least 100bps if not more over the next year, in contrast with the Fed’s more restrained posture. France and Germany are in a weakened political state. Europe is unlikely to mount an effective response to Trump. Given a tepid global economy and cranked up Chinese export machine, a weak euro won’t translate much into increased exports. Parity between the dollar and euro is in sight.

The yen should firm modestly over the year but it won’t be smooth sailing. Many analysts project the official rate will be hiked from 0.25% to 1%, influenced by real wage gains, firmer activity and inflation sustained above 2%. They may prove right. But the Bank of Japan at times seems very cautious about lifting – higher rates will lift the government’s interest bill and a stronger yen will push inflation down; fewer hikes put downward pressure on the yen via the carry trade. The BoJ is instinctively a free floater, but the Finance Ministry will unhappily jawbone if the yen is weak and if the yen rises. Sometimes the authorities appear schizophrenic.

The renminbi will be a tale of two currencies – the trade-weighted renminbi and the dollar-renminbi exchange rate.

The authorities have long and unconvincingly suggested analysts should focus on the trade-weighted renminbi. The real renminbi is extremely competitive, down sharply over the last three years (Figure 2). The International Monetary Fund and others suggest China’s current account surplus is roughly 1.5% of GDP and the trade surplus some 3%. Those estimates are in all probability vastly understated given opacity in China’s balance of payments data. China’s manufacturing trade surplus is roughly 10% of GDP.

Figure 2. Real renminbi is extremely competitive

Source: Bank for International Settlements

The renminbi-dollar exchange rate is more relevant as a gauge for financial flows. Notwithstanding the enormous current account surplus, capital account pressures weigh heavily on the renminbi given major domestic economic headwinds and looming Trump tariffs. Authorities might be tempted to allow considerable renminbi depreciation in the face of any Trump tariffs. But given concerns about accelerated capital outflows and with the renminbi already hyper-competitive, they will most likely restrain depreciation through an array of opaque tools, without drawing lines in the sand.

A quarter of US trade is with Canada and Mexico. The Loonie is under pressure, having fallen some 7% since the summer following forceful Bank of Canada rate cuts amid a softening economy and weaker commodity prices. The central bank may not be finished. Trump’s trade threats are a wild card. Canadian politics is in turmoil.

The Mexican peso also has fallen since the summer. But with core inflation under 4% and Banco de México’s official rate at 10%, the authorities have substantial scope to react to market developments, while contending with Trump.

If Mexico and Canada can begin sorting out relations with Trump 2.0 over the year, their currencies may have scope to find renewed footing and firm. Otherwise, a rocky economic fallout could occur.

There is every reason the dollar will remain extremely strong for the first half of 2025. US slowing in the second half and greater clarity on Trump’s trade policies might pave the way for some modest easing. But projecting exchange rates is a fool’s errand!

Mark Sobel is US Chair of OMFIF.

Interested in this topic? Subscribe to OMFIF’s newsletter for more.